Global| Jun 08 2017

Global| Jun 08 2017German IP Springs Back to Life

Summary

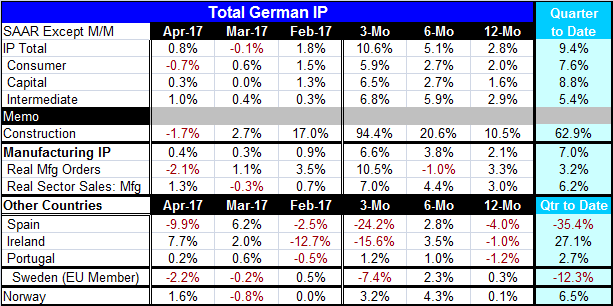

Germany's industrial production gained 0.8% in April after dropping by a thin 0.1% in March. Production is now accelerating sequentially as the 2.8% 12-month pace rises to 5.1% over six months and to 10.6% over three months. All [...]

Germany's industrial production gained 0.8% in April after dropping by a thin 0.1% in March. Production is now accelerating sequentially as the 2.8% 12-month pace rises to 5.1% over six months and to 10.6% over three months.

Germany's industrial production gained 0.8% in April after dropping by a thin 0.1% in March. Production is now accelerating sequentially as the 2.8% 12-month pace rises to 5.1% over six months and to 10.6% over three months.

All sectors show gathering momentum

Despite a drop in consumer goods output in April, all three German sectors consumer goods, capital goods and intermediate goods show the same sequential acceleration in output displayed by the headline. Manufacturing output also accelerates on that timeline as does construction output.

Consistent or widespread strength in Germany

In short, just about any way you cut or divide up German output, the trends show strength and acceleration. Interestingly, the strength is all near-term as year-on-year IP growth is just at 2.8% and for manufacturing it is at 2.1%. Over three months, the weakest sector growth rate is for consumer goods at 5.9%. And since IP growth rates are on inflation adjusted data, these all represent quite strong results.

Strong growth in early Q2

With near-term strength accumulating, it is not surprising that the quarter-to-date calculations (April's growth compounded over the Q1 average) for growth early in Q2 are quite strong. For overall growth the pace is at 9.4% and for manufacturing alone it is at 7%. Construction output is rising at a 62.9% annual rate in Q2. But factory output is growing much faster than real sector sales and real orders, the latter that tend to foreshadow where German output trends are headed. Real sector sales for manufacturing are up in Q2 at a 6.2% pace, just behind the 7% pace for output itself. All the German trends are reinforcing on growth, but the current speed of output does not look to be in line with what orders or real sector sales suggest might be sustainable.

Beyond Germany

Beyond Germany, other early IP reporters in Europe feature EMU members Spain, Ireland and Portugal as well as Sweden and Norway. The strength in output outside Germany is considerably diminished. Spain, Ireland, and Sweden all report double digit annualized drops in output over three months. Portugal features three-month growth at an annualized pace of just 1.2%. Only Norway reports solid-looking IP growth at a 3.2% annual rate over three months. Over six months all these countries show growth in IP at rates ranging from 1% in Portugal to 4.3% in Norway. Over 12 months growth is on a razor's edge as Spain, Ireland and Portugal each report output declines ranging from -4% in Spain to -1% in Ireland. The 12-month change in output in Norway is only 0.1% while in Sweden it's just 0.3%.

Uneven growth in Europe

Germany has been touting some very solid economic numbers. But it has also come under some fire for its relentless and large current account surplus. The data in hand today are but a small and varied sample from the rest of Europe. But these trends make the point that German growth does not travel well. A lot of German output strength is derived from its export prowess which cannibalizes growth in the rest of Europe leaving less behind for fuel and for other EMU and EU countries to mop up. There is a world of difference in the table above between the German data in the top panel and the data from other Europe in the lower panels. Germany is going great guns, but the jury is out on the rest of Europe.

The ECB begins to take the most preliminary steps to shift policy

How growth is spread around is important. Today the ECB met and dropped its reference to future rate cuts as Mario Draghi shifted his tone to speak of risks as roughly balanced. The ECB is beginning to make the first of the noises it will have to make if it is to begin to withdraw its accommodation. Certainly in the EMU, conditions have improved: growth is more consistent and deflation is no longer knocking on the door. But as we see in the IP data, some of the growth is really concentrated and not as readily spread across the region. That could become a problem for policy. On the inflation front, the ECB is not meeting its inflation objective and core inflation, the gauge least impacted by OPEC and oil prices, is showing a still lethargic inflation result. Draghi may be taking the first steps we will need to take to withdraw accommodation, but there still is a lot he will need to see before he actually begins to reverse the ECB's stimulus. Just yesterday Banco Santander absorbed one of its large rivals that was thought to have been on the brink of collapse. Today in a move with some real consequences for Europe, we are waiting on the results of the British elections. They will either strengthen or undermine Theresa May's hand in Brexit negotiations. There is still a lot afoot in Europe and Europe is much more than just what is happening in Germany.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief