Global| Jan 08 2021

Global| Jan 08 2021German IP Rises...So Does the Sun, But That Does Not Mean It Isn't Going to Rain

Summary

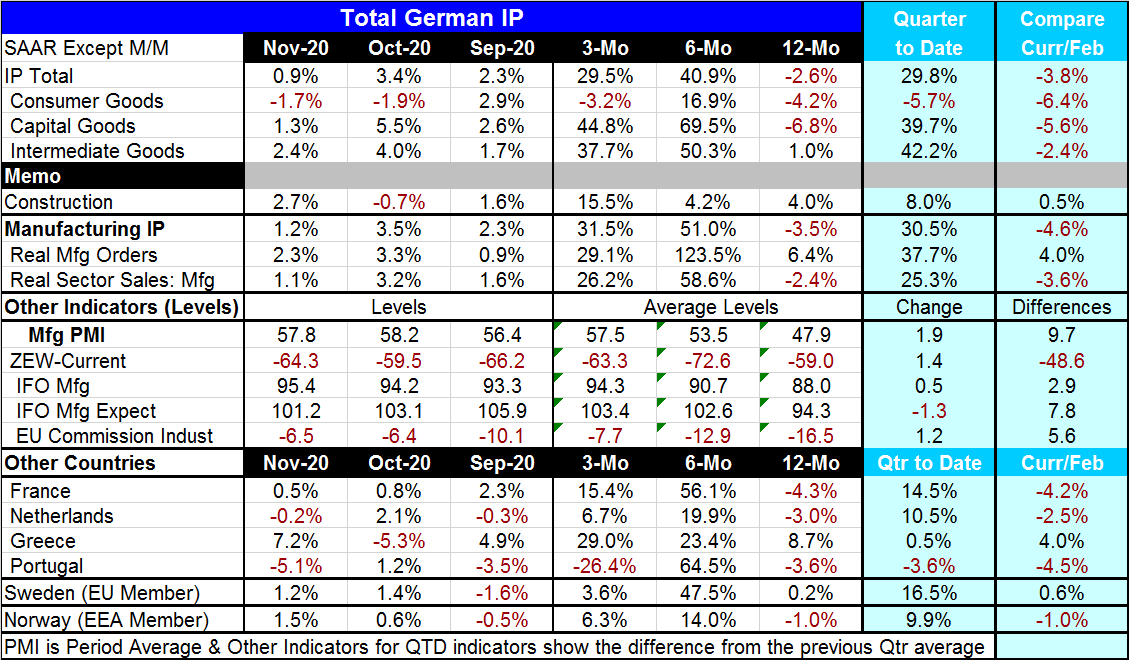

German manufacturing has all the trappings of being on the mend. Output rose by a solid 0.9% in November and is still riding a string of increases. Although output is up at a 29.5% annual rate over three months and at a 40.9% pace [...]

German manufacturing has all the trappings of being on the mend. Output rose by a solid 0.9% in November and is still riding a string of increases. Although output is up at a 29.5% annual rate over three months and at a 40.9% pace over six months; over 12 months it is lower by 2.6% and compared to its level in February German IP is still lower by 3.8%. Despite this recent hot-streak in output manufacturing still lags behind its pre-covid-19 level of performance.

German manufacturing has all the trappings of being on the mend. Output rose by a solid 0.9% in November and is still riding a string of increases. Although output is up at a 29.5% annual rate over three months and at a 40.9% pace over six months; over 12 months it is lower by 2.6% and compared to its level in February German IP is still lower by 3.8%. Despite this recent hot-streak in output manufacturing still lags behind its pre-covid-19 level of performance.

This is significant since there is a new explosion of Covid-19 circulating and a new more communicable variant in the United Kingdom. The U.K. is swimming against the current trying to use the new vaccines to create a herd immunity buffer to stop the spread. In addition, it has adopted much stronger social distancing rules and economic restrictions to slow the spread as the rest of Europe is facing similar spreads but not yet widespread contamination by the new U.K. virus strain. But that risk still lurks.

European manufacturing data are still looking relatively solid as this report demonstrates, but service sector data are showing a more potential hit. This report is only through November but the PMI data are through December and still solid for manufacturing but the December services data show the ongoing wear and tear of the virus and the lockdowns as well as a new negative impact of the virus’ new spread. It is the January period that will hit everything much harder. So bear the timing in mind while looking at the details in this report. This report may come from a cusp of activity that is about as good as it will get before the next wave of virus strikes again.

Despite the clear strength in this report through November, the German data still show irregularities. The consumer sector is not firing on all cylinders as it shows output declines in both October and November. Capital goods and intermediate output both show strong gains over recent months. Construction, despite a decline in output in October, is the only sector to show output in November in excess of its level of activity in February 2020 before the virus struck. Manufacturing output is down by 4.6% compared to February, but real manufacturing orders, an antecedent of output itself, show a 4% rise compared to the level of real orders in February 2020. Still, real sector manufacturing sales trail their February level by 3.6%. But both real sales and real orders show strong gains month-by–month recently as well as strong sequential gains from 12-months to six-months and again form six-months to three-months.

The diffusion data for November show better than the actual accounting data. The IFO manufacturing and expectations gauges for manufacturing as well as the EU Commission industrial index all show gains compared to February 2020. The ZEW current conditions survey, however, is quite contrary. The current gauge reveals a decided sharp deterioration. ZEW’s financial expert assessments of current conditions are quite negative.

Other European nations also are reporting IP data and report out a mixed bag of results that tilts more to ongoing expansion. France, Greece, Sweden and Norway show IP rising in November while the Netherlands and Portugal show output declines. Still, only Greece and Sweden reveal output levels in November above the levels they reported in February 2020. The data do tilt toward showing ongoing expansion based on the sequential growth rates from six-months and 12-months, but the recent monthly data have turned more spotty. Then, of course, because a bird in the hand is worth two in the bush- and it is already January 2021 in real time- the trends in these data do not yet know what we do about what economic realities will be in the months ahead. So it is a good idea to temper your enthusiasm and to discount these trends.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief