Global| Jun 08 2018

Global| Jun 08 2018German IP Follows Orders Lower...Much of Europe Joins Trend

Summary

German trends but more broadly European trends are pointing lower. Germany's IP drop is formally listed as ‘unexpected.' But after four months in a row of orders declining one has to wonder why would a drop in output be unexpected [...]

German trends but more broadly European trends are pointing lower. Germany's IP drop is formally listed as ‘unexpected.' But after four months in a row of orders declining one has to wonder why would a drop in output be unexpected with that legacy? Clearly there has been some denial in the mx so beware of that. It is probably a phenomenon that is broader than just denial about weakness in German industrial output.

German trends but more broadly European trends are pointing lower. Germany's IP drop is formally listed as ‘unexpected.' But after four months in a row of orders declining one has to wonder why would a drop in output be unexpected with that legacy? Clearly there has been some denial in the mx so beware of that. It is probably a phenomenon that is broader than just denial about weakness in German industrial output.

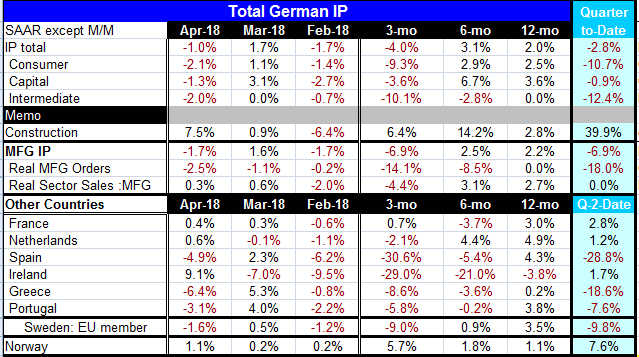

German IP fell across the board in April falling by 1% overall by 2.1% for consumer goods output, by 1.3% for capital goods, and by 2% for intermediate goods. The sequential growth rates from 12-months to 6-months to 3-months generally show a moderate 12-month expansion, a slightly greater 6-month pace then a collapse into decisive decline across the board over three-months. Intermediate goods pose a slight exception to these output trends; they show monotonically declining rates of growth across these horizons.

The construction sector in Germany is a true exception to those trends. Construction shows positive rates of growth on all horizons. Trends in that sector tilt slightly upward. The strongest growth rate is for six months; the three-month growth rate is faster than 12-month growth. Still the year-on-year growth rate in construction is 2.8% not that much stronger than for IP overall that is at 2%.

In the quarter to date all German sector growth rates are negative but again construction is an exception and it is knocking down an amazing 40% annual rate expansion early in Q2. In its public sector Germany is prioritizing the running of a budget surplus and it is planning to cut back on infrastructure spending this year. That could slow down spending in this sector.

Across Europe IP is weak over the last three-months. With eight other European nations reporting IP at this time, we find declines in half of them in April. But it is the broader trend that is disturbing. Over 3-months six of eight show declines in IP; only one, The Netherlands, logs a ‘slow' pace of decline at -2.1%. Spain and Ireland show declines at annual rates of around -30 percent. Moreover, over six months there are declines in five of eight reporters. And the pace of decline is generally large.

Only the Netherlands logs a growth rate over six months that is "strong" at a pace of 4.4%. Norway shows a +1.8% pace and Sweden registers a 0.9% positive pace. After that the rest are all declines. As we also saw for Germany, the 12-month growth rate shows smooth sailing.

Only Ireland has a decline in IP over 12-months (and a relatively severe decline at that). Spain and The Netherlands show growth of over 4% over 12-months, Portugal is at 3.8%, Sweden at 3.5% and France at 3%. The annual figures look just fine. That simply underscores the switch that we have seen in a short period of time to go from growth rates that average (unweighted) 2.1% over 12-months to annualized rates that average -9.8% over three-months.

Both Germany and the rest of Europe are seeing a step-down in growth. Whether it is the fear of trade sanctions and trade warfare or something else is hard to tell. There has been acceleration in place from 2016 through 2017 but at the turn of 2018 there was really something else that happened and redirected growth. The PMI gauges have captured the turnaround. But the ECB is still set to ponder a full exit from its batch of stimulus programs.

The global economy does have a lot up in the air. The US threat of tariffs is more than just a threat. The US has long been the butt of international trade abuse and Donald Trump has vowed to put a stop to it – it was part of the platform on which he ran for office. The rest of Europe is not in the right as much as they think. They just like the way things have been and like the exceptions they have been allowed...and want it to continue. With US wages stagnant and too many low wage jobs being created in the US Donald Trump is no longer willing to have the US milked for its income to shore up other economies. He wants something more like what FREE TRADE is supposed to produce: equal opportunities. Every G7 member runs a long bilateral trade surplus Vs the US except the UK. Germany has the highest current account surplus as a ratio to its GDP of any industrialized economy. And with that Germany is running a budget surplus and does not plan on paying its share into NATO defenses this year.

Yes, the US is "isolated" but it is hardly in the wilderness. I think Europeans need some perspective before they decide to gang up on the US. They may outnumber the US, and in GDP they maybe an equal, but in terms of intransigence THEY are the violators much more than the US a country that is only seeking redress from advantages Europe has had through much of the Post-War period.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief