Global| Apr 06 2018

Global| Apr 06 2018German IP Drops Sharply- What Does It Mean?

Summary

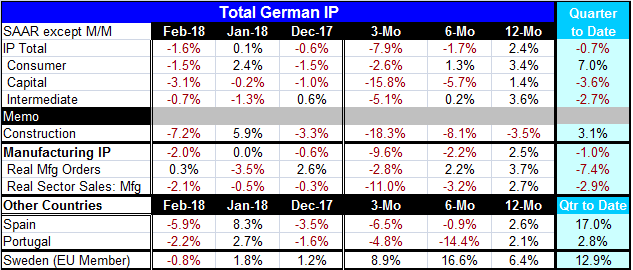

Germany’s industrial production fell by 1.6% in February as bad weather may have taken a toll on output. Construction output fell by 7.2% in February. The March construction PMI for Germany fell for the first time since 2015. [...]

Germany’s industrial production fell by 1.6% in February as bad weather may have taken a toll on output. Construction output fell by 7.2% in February. The March construction PMI for Germany fell for the first time since 2015. Apparently, there are some weather disturbances in play, but it will take time to try to disentangle them from any true weakening that may be in train. The Baltic Dry goods index has been signaling for trade weakness and other indicators –and not just from Europe- also have ‘turned up lame’ recently.

Germany’s industrial production fell by 1.6% in February as bad weather may have taken a toll on output. Construction output fell by 7.2% in February. The March construction PMI for Germany fell for the first time since 2015. Apparently, there are some weather disturbances in play, but it will take time to try to disentangle them from any true weakening that may be in train. The Baltic Dry goods index has been signaling for trade weakness and other indicators –and not just from Europe- also have ‘turned up lame’ recently.

As shown in the table below, German output, orders and real sector sales are weak in recent months and all are falling on balance over three months.

IP in manufacturing, for construction and real sector sales all are lower on balance over six months. However, over 12 months, IP in manufacturing is up by 2.5%, real sector sales are up by 2.7%, real manufacturing orders are up by 3.7%. But over 12 months, construction output is down by 3.5%.

The quarter-to-date calculations show a drop in overall output, a decline in manufacturing IP, a drop in real orders and a decline in real sector sales. But the construction sector, as consistently weak as it has been, manages a pretty good gain for the quarter-to-date (so far).

The early results from Spain and Portugal show substantial recent declines in ongoing output trends. But when the chips fall as they may for the quarter-to-date calculation, both countries are showing a gain in output as well.

The German results are not reassuring even though there seems to be a weather effect embedded there somewhere. The German construction sector is off in February and then the construction sector PMI is falling for the first time in more than three years in March due to colder-than-usual weather. Is weather the culprit for both the March and February declines? Or is there something else going on?

There is at the same a weakening in the Global PMIs from Markit. For Europe, PMI indexes are falling from very high readings to more moderate scores. For much of Asia, there is weakness relative to what has been ongoing disappointing performance. In the U.S., the ISM gauges are off peak but still very high-valued. What have started to look weak in the U.S. are retail sales, with three monthly overall sales declines in a row. Recall that consumer spending is about 70% of U.S. GDP.

There has been a great focus on central banks in recent months as the attention in Europe is on a policy turn coming from the ECB. Japan has even started to talk of an end game for its easy approach. The BOE started rates higher, then, much as the Fed did, put its rate hiking ambitions on hold. In the U.S. with a new Fed chairman in place, there is speculation about policy and clear assumptions that some string of rate hikes is coming. But all of this discussion has simply focused on central bankers’ actions as growth continues to come on line. What if the assumption of growth coming on line or of growth accelerating turns out to be not true? There were such high hopes for Europe early in the year and all of a sudden euro-trends are not looking so good. Europe’s taking advantage of the U.K. as they negotiate Brexit looks to be very short sighted especially as Russia acts in a more reckless, bolder fashion.

In short, there are many assumptions made in late-December and early-January about how the world would look that are not looking quite so prescient at the moment. It’s a good time to be open-minded and to not dismiss things that are unexpected as false.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief