Global| Sep 07 2017

Global| Sep 07 2017German IP Comes Up Flat One Month After Falling; German Output Trend Cools

Summary

Germany's industrial production was flat in July after a 1.1% decline in June. These results followed a series of five months during which German output expanded strongly at a 12% annual rate. With the slowing in the past several [...]

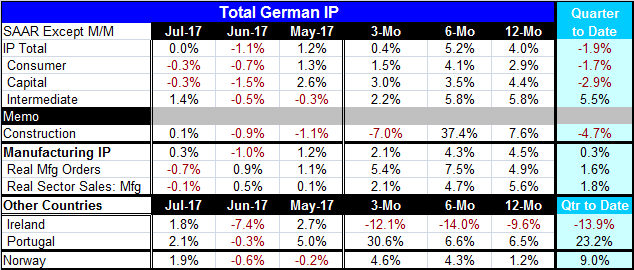

Germany's industrial production was flat in July after a 1.1% decline in June. These results followed a series of five months during which German output expanded strongly at a 12% annual rate. With the slowing in the past several months, the 12-month growth rate is now down to 4%. It accelerates to 5.2% over six months because of that hot growth span then eases back to a 0.4% annual rate over the most recent three months. Manufacturing shows a steadier pace of slowing with 12-month growth at 4.5%, the six-month pace at 4.3% and the three-month pace at 2.1%. Even so, manufacturing shows growth in the nascent third quarter at just a 0.3% annual rate.

Germany's industrial production was flat in July after a 1.1% decline in June. These results followed a series of five months during which German output expanded strongly at a 12% annual rate. With the slowing in the past several months, the 12-month growth rate is now down to 4%. It accelerates to 5.2% over six months because of that hot growth span then eases back to a 0.4% annual rate over the most recent three months. Manufacturing shows a steadier pace of slowing with 12-month growth at 4.5%, the six-month pace at 4.3% and the three-month pace at 2.1%. Even so, manufacturing shows growth in the nascent third quarter at just a 0.3% annual rate.

The detailed sector trends show us that construction is holding back overall IP as it has fallen in two of the last three months and gained in the current month by only 0.1%. Its three-month growth rate is -7% and its quarter-to-date pace is -4.7%. The manufacturing components of consumer goods, capital goods and intermediate goods show declines in July and in June except for intermediate goods that post an increase in output in July. Capital goods output is showing sequential deceleration as output slows from a 4.4% pace over 12 months to 3.5% over six months to 3% over three months. Consumer goods trends show a speed up from 12-month to six-month then a slowdown to a three-month pace below the 12-month pace. Intermediate goods shows a strong 5.8% 12-month growth rate that is steady over six months then slows sharply over three months. All sectors show a slowdown from 12-month to three-month. But in the quarter-to-date consumer goods and capital goods output is contracting while intermediate goods output is still expanding.

After a strong hard run, German manufacturing is in a slowing mode. That is not surprising - nor is it inconsistent with its past strong pace that was too fast to be sustained. Based on other survey data, it appears to be a slowing and nothing more. The European Central Bank's decision today to hold rates and its declaration that it could still do more economic stimulus, should help to stabilize the euro which had been moving up sharply and persistently on expectations that the ECB was on the verge of a shift to less accommodative policies. That shift still lies ahead but is perhaps farther in the future than markets had expected.

The main German economic barometers for manufacturing are presented in Chart 2: real orders, the manufacturing PMI and manufacturing IP. They show that conditions have cooled. They also show how the manufacturing PMI leads and overshoots. In this chart, (unlike the first chart), we plot the PMI in percentage change terms the same as for real orders and IP itself. In this format, the PMI is on the same schedule as the other indicators and it is already in a cooling mode. Real orders have steadied at around the 5% growth mark and IP itself rarely runs hotter than orders. IP's year-on-year growth is stabilizing, and as we see in the table, its sequential growth rates are slowing.

The main German economic barometers for manufacturing are presented in Chart 2: real orders, the manufacturing PMI and manufacturing IP. They show that conditions have cooled. They also show how the manufacturing PMI leads and overshoots. In this chart, (unlike the first chart), we plot the PMI in percentage change terms the same as for real orders and IP itself. In this format, the PMI is on the same schedule as the other indicators and it is already in a cooling mode. Real orders have steadied at around the 5% growth mark and IP itself rarely runs hotter than orders. IP's year-on-year growth is stabilizing, and as we see in the table, its sequential growth rates are slowing.

There has been some excitement about the strong manufacturing PMI growth rates, but the PMI itself is cooling in momentum terms even as its static reading remains strong. One issue to ponder is that the manufacturing PMI has not been cranking up the services sector along with it in Germany. That is another aspect of the recovery story to bear in mind. Globally, there are a lot more manufacturing PMIs to peruse and while they are 'doing better' Asia as a group is still lethargic. And services sectors have been less buoyant than manufacturing. But jobs generally come out of the services sector and service sector growth in Germany in particular has been stunted. For all of the EMU, services sector performance is still solid; however, for Germany, it has lagged badly. The U.S. service/nonmanufacturing sector also is sluggish in PMI terms on the ISM gauge. Thus, a broader global picture still finds flaws in the accelerationist hypothesis and finds the step back in German manufacturing a more consistent result.

On balance, I find the slowing in Germany most consistent with the other German indicators we have. While it is sometimes useful to see the services and manufacturing sectors separately, it is also good to put them together to see how they are feeding off one another and how balanced growth is. It looks as though manufacturing sort of got out of the gate too fast and is being pulled back to a more sustainable pace, either by its own dynamics or by a services sector that simply has not gone along for the fast ride. The German economy is still doing fine. It is just not as pedal-to-the-metal as the PMI data were saying just a few months ago. The PMI readings are still strong, but they are what they are which are indicators of breadth not of strength, and their tendency is to oversell each and every trend- Chart 2 shows that plain as day.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief