Global| Feb 07 2018

Global| Feb 07 2018German IP Backs Down But Still Logs a Solid Growth Profile

Summary

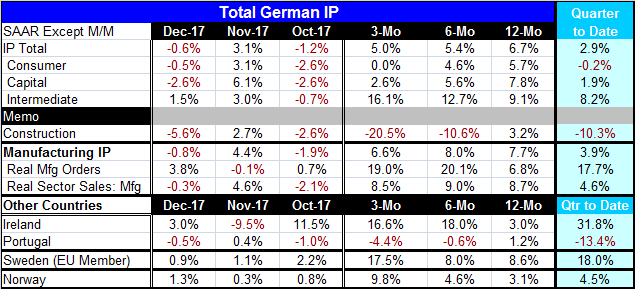

Despite falling in two of the last three months, Germany's industrial production is still advancing at 5% annual rate over those same three months. That growth rate indicates a very slight slowing trend for German IP which is up by [...]

Despite falling in two of the last three months, Germany's industrial production is still advancing at 5% annual rate over those same three months. That growth rate indicates a very slight slowing trend for German IP which is up by 6.7% over 12 months and up at a 5.4% annualized rate over six months. Output also fell for consumer goods and capital goods in December. And for both of these sectors, growth has showed outright contraction in two of the last three months. Both also show decelerating output trends. For German IP, the output of consumer goods and of capital goods shows clear decelerations that cut to weak growth rates. The acceleration in German output is all in intermediate goods and that is a red flag of sorts. Intermediate goods feed the other sectors; they are not a trend leader. But during an expansion phase, it is normal for intermediate goods output to be fastest but only when there is output acceleration. That may be drawing to a close.

Despite falling in two of the last three months, Germany's industrial production is still advancing at 5% annual rate over those same three months. That growth rate indicates a very slight slowing trend for German IP which is up by 6.7% over 12 months and up at a 5.4% annualized rate over six months. Output also fell for consumer goods and capital goods in December. And for both of these sectors, growth has showed outright contraction in two of the last three months. Both also show decelerating output trends. For German IP, the output of consumer goods and of capital goods shows clear decelerations that cut to weak growth rates. The acceleration in German output is all in intermediate goods and that is a red flag of sorts. Intermediate goods feed the other sectors; they are not a trend leader. But during an expansion phase, it is normal for intermediate goods output to be fastest but only when there is output acceleration. That may be drawing to a close.

Real manufacturing orders and real sales still show stability and strength in their respective growth rates and paths. They continue to have a pace that exceeds the pace for output itself.

There are four other early reporting European countries of industrial output data. Three of four show strong to accelerating trends in output with Portugal being the exception. Ireland, Sweden and Norway show expansion or outright acceleration.

Separately, the PMI data continue to point higher for Germany and the EMU. The global expansion is in place and the outlook for continued gains in output is good. The EU Commission just today notched its growth expectation for the EMU up by two tenths of one percentage point for 2018 to 2.3%.

Historically, when German output is ramping up, intermediate goods output will for a time grow faster than other sectors. That is followed by a peaking in other sector growth rates followed by a slowdown. However, it is not negative signal about the future as much as it is statement about how the cyclical sector growth rates play out. For the time being, this underscores that Germany is seeing a real acceleration in output. Intermediate goods output can grow faster than the average output of capital goods and consumers goods for an extended period of time. About half the time, intermediate goods grows faster than the average of the other two sectors in an expansion phase. For now this is pro-growth signal. But the sharp slowing in the other two sectors over the last three months is a sign for caution. Once there is a slowing in consumer goods and capital goods output, the output of intermediate goods is not going to continue to lead the parade. Instead, it will head for a pullback. With the recent volatility in the data, it is hard to know how abrupt the pullback will be, but there are output declines in two of the most recent three months and then there is that nagging weakness in the Baltic dry goods index to think about.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief