Global| Dec 08 2008

Global| Dec 08 2008German Industrial Output Trends is Weaker Than Expectedly

Summary

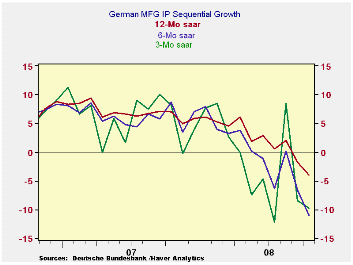

German industrial output fell by 2.1% in October and its sequential growth rates show a steady drumbeat of negativism more than an acceleration of weakness. This is in stark contrast to the unraveling in orders. But order weakness [...]

German industrial output fell by 2.1% in October and its

sequential growth rates show a steady drumbeat of negativism more than

an acceleration of weakness. This is in stark contrast to the

unraveling in orders. But order weakness always takes several months to

become embedded in the behavior of output so the steadier path of

output is not much in which to take solace. Finally it is the consumer

sector that it showing some resiliency. But capital goods and

intermediate goods industry output each show persisting deep if not

accelerating declines in output. With the economic crisis spreading

this resiliency by consumers will not be long lived. MFG IP shows

relatively more weakness. And orders are pointing the way much lower.

| Total German IP | |||||||

|---|---|---|---|---|---|---|---|

| Saar except m/m | Oct-08 | Sep-08 | Aug-08 | 3-mo | 6-mo | 12-mo | Quarter-to-Date |

| IP total | -2.1% | -3.3% | 3.2% | -8.7% | -10.5% | -3.9% | -17.8% |

| Consumer Goods | -0.4% | -2.3% | 3.5% | 2.8% | -1.6% | -3.4% | -4.8% |

| Capital Goods | -3.1% | -3.1% | 3.7% | -10.1% | -14.6% | -4.6% | -21.4% |

| Intermediate Goods | -2.2% | -4.6% | 2.9% | -15.3% | -11.6% | -3.4% | -23.5% |

| Memo | |||||||

| Construction | -3.0% | -3.0% | 6.4% | 0.5% | -5.1% | -4.3% | -16.5% |

| MFG IP | -2.2% | -3.6% | 3.3% | -9.8% | -11.0% | -3.9% | -19.2% |

| MFG Orders | -6.1% | -8.3% | 3.5% | -36.8% | -28.3% | -17.3% | -48.2% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief