Global| Jun 25 2018

Global| Jun 25 2018German IFO Slips in June

Summary

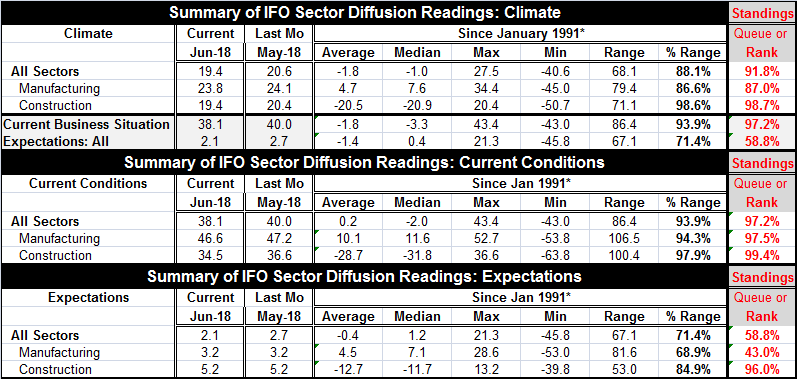

All of the early-release IFO climate and aggregate metrics in the top portion of the table declined in June. All-sector climate fell, manufacturing climate fell, and construction climate fell. The current business situation index [...]

All of the early-release IFO climate and aggregate metrics in the top portion of the table declined in June. All-sector climate fell, manufacturing climate fell, and construction climate fell. The current business situation index dropped by nearly two points and overall expectations dropped.

All of the early-release IFO climate and aggregate metrics in the top portion of the table declined in June. All-sector climate fell, manufacturing climate fell, and construction climate fell. The current business situation index dropped by nearly two points and overall expectations dropped.

Of these five metrics, three of them still reside in the top 10% of their respective historic queues of values. Construction is in its top 2%, the current business situation is in its top 3%. The all-sector climate index stands in its top 9 percentile of its historic queue of values. While not quite as strong as those indicators, the manufacturing index stands in its 87th percentile, a top 13 percentile standing- still quite impressively strong. The weak reading of the bunch is for expectations with a 58 percentile reading, a metric that is still firm and above the neutral ‘normal’ reading of 50. In diffusion terms, all the indicators show expansion.

The current conditions detail shows declines in June for both manufacturing and construction in addition to the all sector index being lower. Still, the standings for the diffusion indexes show manufacturing in its top four percentile and construction’s current reading in its top one percentile.

Expectations are a different story. As we saw above, all-sector expectations have a more moderate 58th percentile standing. But manufacturing, despite its strong climate reading, has an expectation standing only in its 43rd percentile below its median reading (which occurs at a value of 50 and that signals ‘normalcy’) despite the fact that manufacturing still shows expansion and despite the fact that expectations over all are still positive. The positive reading is still below what is normal for the sector. Construction, on the other hand, shows a strong climate reading and a strong expectations reading to accompany it.

The chart clearly depicts the situation with the current index flying up and away relative to the other metrics although it has been roughly flat with a couple of spike highs that did not last over the past year or so. Climate and expectations have lost upward momentum and have declined relatively persistently and significantly in 2018.

However, the whole of the European area itself is feeling pressure. Angela Merkel, while still the head of government in Germany, is not in the same control as she once was. The touch-stone issue for Germany as it is in many places is migrants. People who have lived under terrible conditions or in places that have become intolerable are leaving and flocking to more developed countries without taking the time to go through formal immigration channels. In Europe, there are migrants from war torn Syria and elsewhere that are filling boats and crossing the Mediterranean. Greece and Italy have borne the brunt of this immigration, but the new Italian government is standing up in defiance of letting more in. It is trying to deflect them to Malta or Spain or elsewhere. Germany is essentially land-locked by other EU members who have closed their borders. Germany gains some protection from that. But it has been admitting migrants at its own pace and there is opposition even to this. Merkel has noted that Greece and Italy have borne the brunt of these migrants, but the EU passed rules disallowing passage of migrants from their entry ports until they were accepted elsewhere. This has caused a piled-up of migrants in Italy and Greece as acceptance of migrants in other EU members has been too slow to handle the flow. The EU has done nothing to relieve this burden on Greece and Italy. So migration is literally an exploding issue in the EMU as Italy has shut its ports to ships with rescued migrants. Interestingly, the U.S., a broad ocean away, has the same set of problems and suffers domestic political division over migrants sweeping over it. The U.S. southern border with Mexico is breached regularly by Mexicans and other Central Americans who have flocked to the U.S. as a safe haven. Of course, the migrant issue already was responsible for blowing the U.K. out of the EU in Europe. Migration issues may seem noneconomic, but they are huge political and socio-economic influences. The issues are not just those of migration but of its scope. Once a migration starts, it seems very hard to stop and for the flow to diminish.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief