Global| Jul 25 2017

Global| Jul 25 2017German IFO Is Stunning, But Is It Right? What Does It Mean?

Summary

Positioned in its various arrays of data since 1991, the German IFO index and its principle components show the all-sector reading at its historic high (since 1991), manufacturing at its historic high and construction at its historic [...]

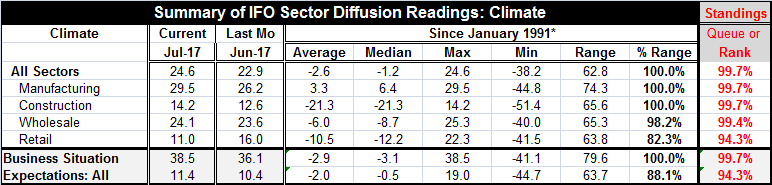

Positioned in its various arrays of data since 1991, the German IFO index and its principle components show the all-sector reading at its historic high (since 1991), manufacturing at its historic high and construction at its historic high. Wholesaling is lagging as it is less than two percentage points off its high value and has been this strong or stronger only 0.6% of the time (that rounds to 'almost never'). All humor aside the retailing index is less ebullient as it stands in the 82nd percentile of its historic high-low range and also at the 94th percentile of its historic queue. The retail index has been about 18% higher than its current value at its best, and has been higher than its current value less than 6% of the time. Most EMU members would 'kill' to have readings as strong as the IFO's weakest sector. And, yes, despite all this strength, retailing did actually slip in July, falling by a relatively sharp 5 points from its June value.

Positioned in its various arrays of data since 1991, the German IFO index and its principle components show the all-sector reading at its historic high (since 1991), manufacturing at its historic high and construction at its historic high. Wholesaling is lagging as it is less than two percentage points off its high value and has been this strong or stronger only 0.6% of the time (that rounds to 'almost never'). All humor aside the retailing index is less ebullient as it stands in the 82nd percentile of its historic high-low range and also at the 94th percentile of its historic queue. The retail index has been about 18% higher than its current value at its best, and has been higher than its current value less than 6% of the time. Most EMU members would 'kill' to have readings as strong as the IFO's weakest sector. And, yes, despite all this strength, retailing did actually slip in July, falling by a relatively sharp 5 points from its June value.

What's impressive

The business situation index is at its all-time (since 1991) high at a reading of 38.5. Expectations have been this high or higher about 6% of the time. The IFO report is stunning for its 'strength' and for its breadth.

What's not...

However, here I should also offer the disclaimer. The IFO is a diffusion index to start. So the various indexes are formally never about strength but only about breadth. In other words, the IFO tells us that there is a record proportion of firms with output expanding in all sectors, in manufacturing and in construction. It does not actually spell out how strong those gains are, just that they are gains. When I say that the report is impressive or strong, this is using the usual vernacular for describing these sorts of indexes. However, from time to time we also have to remind ourselves what we really have. It would be more correct to say that the IFO survey is impressive for its breadth by sector and for the spread of sectors that also show such a breadth of gains- and never to use the word 'strength.'

Perspective...get some!

We should not confuse this with a report about surging industrial production (IP) or anything like that. As of May German manufacturing IP is up by 4.5% over 12 months and German IP overall is up by 3.8%. These are solid and even strong gains but not historically strong for the German economy: current annual German IP gains are on in the top 20 to 25% of its historic results. The EMU and Germany clearly are not growing anywhere near 'historically strong' rates of growth. So what are these huge historic diffusion rankings telling us anyway?

Consistencies/inconsistencies

This month the IFO diffusion indexes are at a place where diffusion indexes can get you in trouble if you are not careful to remember what they are and what they are not. We tend to infer strength from breadth but strength and breadth are two different things. Nonetheless, this is an impressive report. As the chart shows not only are the levels of the diffusion readings high, but there has been sharp gain as well. There is not just great breadth but a recent substantial improvement in breadth and in momentum. Interestingly, the Markit indexes of July (flash) did not seem to be tipping off the same sort of thing. Markit, which also uses diffusion indexes, showed some backing off in Germany and in the Markit PMI framework the services sector, which is well represented in the IFO survey, is at historically weak readings. There is a chasm of difference between the IFO on services and Markit on services in Germany.

I love diffusion surveys...I hate diffusion surveys...

This is why I have a love-hate relationship with diffusion indexes. I like the reports and they are useful surveys and easy to administer. They tend to be highly sensitive to changes in the economy. But we are also seeing a large gap in what the surveys are telling us about services in Germany from two different sources. Similarly there has been a huge gap between what the Markit PMI gauges have been telling us about services and manufacturing in the U.S. and what the U.S. ISM surveys for manufacturing and nonmanufacturing have been saying. It is reasonable to conclude from this that these diffusion surveys are very sensitive to the samples chosen. That lack of robustness is not good news. Over time the IFO has been considered a very reliable survey on the German economy. In the U.S., the long lived ISM manufacturing survey also has a solid reputation and a very long history. The ISM manufacturing survey tends to be well connected to other manufacturing data as well anchoring itself with credibility. But the less long-lived ISM nonmanufacturing survey has been fickle and has not been able to track with other service sector data especially not with monthly employment surveys. That is not to say that the Markit survey is better there. But perhaps there is flaw in the services sector or in its respondents. Either service sector data are intrinsically less consistent or the people in the service sector filling reports are less careful than their counterparts in manufacturing. In any event, the services gauges appear to be less reliable.

German services sector going nowhere in the Markit framework...

Recent diffusion indexes do raise some questions with their inconsistencies. Today there is even a very strong diffusion reading for U.K. manufacturing out of the CBI at a time when other U.K. reports have been much more equivocal. U.K. manufacturing data through May have actually been weakening. I think it's a good time to treat the diffusion indexes with kid gloves, especially for services. Certainly, rising breadth is not a bad thing. But it's not the same as strength. And when two professionally executed surveys produce starkly different results, it's time to wonder if someone is not taking the pulse of the wrong patient. Too many gaps are appearing among what diffusion surveys say and between what they say vs. other sorts of surveys. Caveat Emptor!

Recent diffusion indexes do raise some questions with their inconsistencies. Today there is even a very strong diffusion reading for U.K. manufacturing out of the CBI at a time when other U.K. reports have been much more equivocal. U.K. manufacturing data through May have actually been weakening. I think it's a good time to treat the diffusion indexes with kid gloves, especially for services. Certainly, rising breadth is not a bad thing. But it's not the same as strength. And when two professionally executed surveys produce starkly different results, it's time to wonder if someone is not taking the pulse of the wrong patient. Too many gaps are appearing among what diffusion surveys say and between what they say vs. other sorts of surveys. Caveat Emptor!

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief