Global| Oct 26 2015

Global| Oct 26 2015German Ifo Index Slips But Not As Much As Feared; The Strength in Expectations Is A Surprise

Summary

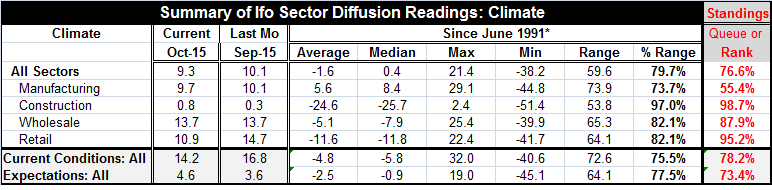

The Ifo index fell to 9.3 in October from 10.1 in September. The all-sector drop is less that the drop of the ZEW index reported earlier. The expectations portion of the Ifo index actually saw improvement in October and it is hard to [...]

The Ifo index fell to 9.3 in October from 10.1 in September. The all-sector drop is less that the drop of the ZEW index reported earlier. The expectations portion of the Ifo index actually saw improvement in October and it is hard to understand how that has happened.

The Ifo index fell to 9.3 in October from 10.1 in September. The all-sector drop is less that the drop of the ZEW index reported earlier. The expectations portion of the Ifo index actually saw improvement in October and it is hard to understand how that has happened.

The Markit PMI indices saw weak reports for manufacturing with relatively more strength in services. Still, the Markit readings are quite moderate. There is the chaos being caused by the large adoption of migrants that Angela Merkel has committed to absorb in Germany. Global conditions remain difficult, with weak growth and low inflation - or deflation. The ZEW expectations index has backtracked strongly in October. So the rise in expectations in this report is a contrary to some previous reports and in sharp contrast with the forward-looking portion of the ZEW report.

Still, the details of the Ifo, evaluated over the same period as the Markit PMIs, show a weaker manufacturing sector than in the Markit framework. The services sector picture in the Ifo is, however, stronger than the services in the Markit schematic. Both surveys show services as superior in strength to manufacturing, however. Compared to ZEW, and evaluated on the same horizon, there is simply no comparison between the high expectations standing in the Ifo and the low reading in ZEW.

This creates a dilemma in trying to assess the German economy. Both surveys are respected. Both the ZEW and Ifo have relatively strong current readings. But the outlook or expectations portions are now a dilemma.

While the ZEW survey is a canvassing of financial experts, and the Ifo is an assessment given by experts in the industry, it is not clear which of these groups has the best vantage point to assess the future. On current conditions, we can give the nod to the Ifo experts who have feet on the ground in their respective sectors. But on that score there's little Ifo/ZEW difference this month.

For now I think we have to simply realize that the global economy is in flux and still under a lot of pressure. Demand is weak and it is weak enough that the ECB is considering stepping up its QE program. Also in Europe the migrant crisis is getting exponentially worse and creating serious divisions among EMU members about how to deal with it. Tensions are especially high among member countries employing the Schengen agreement which allows for free movement of people among the Schengen member countries.

There are really no signs of growth picking up to any significant degree in Europe or in Germany. Germany is still doing much better than its fellow EMU members, but it is showing signs of wear and tear, too. China's backlash has hit an important German export market very hard. Economic barometers mostly indicate continuing subpar growth in Europe. But the introduction of the migrant issue has destroyed the idea of a singular approach to the crisis and portends heavy government spending to economically support them. Will this schism undermine the regional cooperation in other areas? Germany has stepped up with a promise to absorb a large number of migrants, but the rest of Europe has not followed suit and some have explicitly rejected the notion of migrant absorption.

I am skeptical of the Ifo reading on expectations. I see too many challenges rising for Europe and no sign of economic acceleration. Even with the ECB apparently getting ready to step up its clout on the monetary side, it is not clear that more QE will have the desired impact. The ECB's talk of stepping up stimulus most clearly is an admission that things are not getting better. That, in and of itself, should be very worrisome. Remember that the Fed in the U.S. stopped QE because it was becoming less effective. Does the ECB still have leverage with this program or not? Europe remains between a rock and a hard place with few viable policy options. It's hard to see how expectations in Germany rise in this environment.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.