Global| Feb 24 2020

Global| Feb 24 2020German IFO Index Shows SLIGHT Expectation Improvement Contrary to Zew Survey ...as the Corona Impact Infects [...]

Summary

With the coronavirus spreading to Europe and now harassing economic conditions in Italy spreading to Iran and Iran in turn spreading it in the Middle East, it is clearly a time to micro-manage the outlook. Every new piece of [...]

With the coronavirus spreading to Europe and now harassing economic conditions in Italy spreading to Iran and Iran in turn spreading it in the Middle East, it is clearly a time to micro-manage the outlook. Every new piece of information needs to be scrutinized for any evidence of new weakness and at the same time compared to any similar survey to avoid being taken in by the idiosyncrasies of any particular report. Germany’s IFO shows us a survey result for manufacturing that traditionally has tracked the Markit MFG PMI well; but it lags behind its rebound this month. However, the expectations for the IFO surpass the soured outlook of the Zew financial experts. Here it is important to note that the IFO surveys industry participants for market conditions while the Zew survey is one of financial experts assessing the economy. They don’t always see eye to eye or have the same perspective.

With the coronavirus spreading to Europe and now harassing economic conditions in Italy spreading to Iran and Iran in turn spreading it in the Middle East, it is clearly a time to micro-manage the outlook. Every new piece of information needs to be scrutinized for any evidence of new weakness and at the same time compared to any similar survey to avoid being taken in by the idiosyncrasies of any particular report. Germany’s IFO shows us a survey result for manufacturing that traditionally has tracked the Markit MFG PMI well; but it lags behind its rebound this month. However, the expectations for the IFO surpass the soured outlook of the Zew financial experts. Here it is important to note that the IFO surveys industry participants for market conditions while the Zew survey is one of financial experts assessing the economy. They don’t always see eye to eye or have the same perspective.

The IFO and the Markit surveys AGREE that there is a bottoming and some degree of rebound in the offing for manufacturing. What the two surveys do not quite seem to agree on is the degree of rebound. For now their agreement on bottoming is more significant than their disagreement on the degree of rebound. A slight difference in survey dates could be responsible for differences in degree.

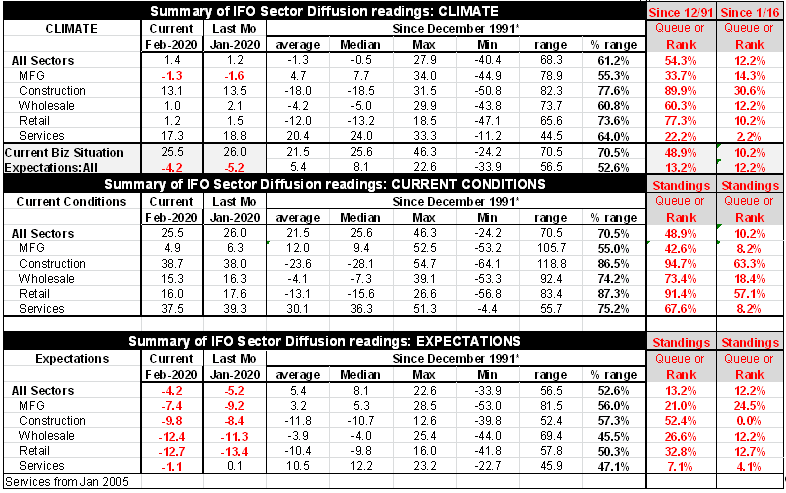

Sector indices show all on declining TRENDS

Except for...some stabilization hinted at in manufacturing and wholesaling

IFO sectors, however, show that the hint at a rebound is an artifact of manufacturing and of wholesaling. Construction, clearly the best performing sector, also has clear ongoing decay. And retailing also remains either flat on a low reading or with some slight deterioration.

Expectations: danger!

While the whole of the IFO expectations have perked up on the month; the expectation reading still carries a negative sign with more pessimists than optimists weighing in. Also, the current business situation slightly eroded in February.

Percentile standings

The story of the percentile standings remains the same it has been for some time with more weakness measured in sectors relative to the recent time period than when measured against the longer time period. This is just another way of saying that the recent time period has been generally stronger than the longer period. Still, both forms of relative rankings have their own validity, if applied correctly to the situation at hand. (Let’s not get embroiled in game of fake-news; this is a ‘game’ of relativity, and all relativity gauges are different).

Climate readings show more "cooling" than "warming"

For example the climate reading shows an all-sector index with a 54.3 percentile rank on data back to 1991. However on data back to 2016 the ranking is only in its 12 percentile. This tells us than compared to a longer history today’s climate reading is just above its median (the median reading occurs at a rank of 50). Yet on a ranking since 2016 the climate ranking has been weaker only about 12% of the time. So on recent data Germany is showing at a relatively weak reading yet it cannot be called troubling yet because compared against a longer history it is still above ‘normal.’ However, the slippage is to be noted and it is here that the notion of momentum becomes very important. Wholesaling and manufacturing show signs of stabilizing. That is good news since manufacturing has a climate ranking over the long term of 33.7 percent well below its median and clearly in the too-weak zone. Wholesaling has a long-history comparative rank of 60.3% above its median so stabilization in this zone would be comforting. The important service sector with a long-period climate ranking of 22% vs a short cycle ranking of 2.2% is worrisome and its climate reading is slipping on the month. Services show weakening current conditions on the month and weakening and now negative expectations as well.

Expectations and momentum

Expectations show month-to-month improvements in February overall and for manufacturing and retailing. Still, construction, wholesaling and services deteriorate. All sectors have net negative expectations assessments. Expectations’ percentile queue standings are all much more similar for expectations than for current or climate rankings. Since expectations in the period rank much more similarly to the longer period that do current conditions, that makes momentum a more important characteristic to track. And right now momentum is a split decision worsening in more sectors than it is improving but improving in two sectors by enough to drive the overall higher this month. That will be the thing to keep an eye on.

The corona syndrome

At this time the coronavirus has not impacted economic activity as much as it currently beginning to disrupt financial markets. Today and Friday, in particular markets began to take the impact of the virus very seriously. The Baltic Dry Freight index remains very weak but it has been creeping up very slowly from its recent low. That small but positive ‘trend’ is still in play for now. But now financial markets, especially the US stock market, global bond yields and exchange rates are being pulled into the vortex of danger that surrounds the corona-syndrome. There is no telling where it goes next or how virulent its spread will be outside China. WHO is now more concerned with the spread of disease that it can’t clearly link back to China. I doubt (CAVEAT: I’m not a health expert, but I doubt) that the virus has sprung up independently in other places. I suspect that what is at work is that health officials have lost containment. The virus has spread though unexpected contact to people and through people that WHO can no longer track with any certainly back to China. It is the loss of containment, the loose end of contagion that is now a fear. Iran seems slow to act. And it has been quick to blame “the West” for the spread of the virus (curious isn’t it?) claiming that it was a ‘scare perpetrated to keep people away from voting in their election where turnout was so poor. Contrarily was Iran in denial and did it act slowly to admit the existence of the virus and was it slow to contain it in order to try to get more people to vote- that is to get them to congregate in a way that would spread the virus faster? If so, Hall of Shame for Iran and its leaders.

The blame game – don’t play it!

Who knows who will be blamed next? But it is clear that countries that place their own political agenda’s above the health and safety of their people are going to suffer. Iran easily slots into that category and I worry that China is taking off travel restrictions too soon to try to get growth back in gear while the danger of contagion is still high. Only time will tell. Just as the proof of the pudding is in the eating, the spread of the disease is in the infection and contagion. No matter where you are pursue good hygiene practices and be wary. There is no telling how the disease might be spread to someone you have even passing contact with. It is still a global economy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief