Global| Aug 26 2009

Global| Aug 26 2009German Ifo Index Is Showing Widespread Recovery

Summary

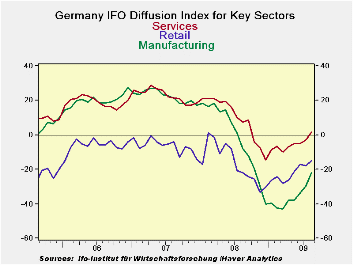

The month-to-month improvement in the all sector IFO diffusion index is the second largest since 1991. All sectors improved in the month. The manufacturing index is improving especially rapidly. The services sector has dug itself out [...]

The month-to-month improvement in the all sector IFO diffusion

index is the second largest since 1991. All sectors improved in the

month. The manufacturing index is improving especially rapidly. The

services sector has dug itself out of its declining phase and has

posted not just an improvement but an outright gain in the month.

Still in relative terms, ranking sectors within each one’s

range of actual variation finds construction as the relative strongest

reading. Its -24 reading in August is above the mid point of its range

and just below its average reading of -29 compared to a current reading

of -24.

Retailing stands in the 44th percentile of its range.

Wholesaling and services stand in the upper thirty percentiles of their

respective ranges. While manufacturing is rising strongly it remains as

the relative weakest sector in the bottom 29th percentile of its range.

The overall index stands at the 30th percentile of its range.

The strong rise in the MFG sector drove the improvement this

month. as the MFG sector showed the greatest rise in the history of its

index. Wholesale’s improvement ranks eighth. The improvement in

services is the ninth largest in its shorter history since June 2001;

the other series date from 1991.

The rebound in the IFO index is impressive. The levels of the

various sectors fall short of being construed as a complete recovery,

but they do show that a recovery process is in train. It is too soon to

be able to guess accurately at when the economy will be on an even

keel. But for now the improvement is rapid and in the right direction.

The IFO confirms other reports that suggest that the recovery phase has

begun.

| Summary of IFO Sector Diffusion readings: CLIMATE | ||||||||

|---|---|---|---|---|---|---|---|---|

| CLIMATE Sum | Current | Last Month | Since Jan 1991* | |||||

| Aug-09 | Jul-09 | Average | Median | Max | Min | Range | % range | |

| All Sectors | -19.7 | -25.9 | -9.4 | -9.9 | 17.5 | -36.2 | 53.7 | 30.7% |

| MFG | -22.0 | -29.7 | -2.0 | -0.3 | 27.5 | -42.8 | 70.3 | 29.6% |

| Construction | -24.0 | -25.3 | -29.3 | -30.3 | 0.7 | -50.1 | 50.8 | 51.4% |

| Wholesale | -14.6 | -22.5 | -14.7 | -16.3 | 23.9 | -39.0 | 62.9 | 38.8% |

| Retail | -15.0 | -17.8 | -16.0 | -15.1 | 16.8 | -40.4 | 57.2 | 44.4% |

| Services | 1.4 | -3.0 | 10.9 | 9.5 | 28.5 | -14.5 | 43.0 | 37.0% |

| * June 2001 for Services | ||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief