Global| Jun 26 2017

Global| Jun 26 2017German IFO Gauge Shows Strong Ongoing Growth

Summary

The IFO ordinary indexes (see Chart) continue to climb in June. The ordinary IFO indexes (not the diffusion indexes) are at their highest marks since January 1991 for both the headline and the current index. The expectation index has [...]

The IFO ordinary indexes (see Chart) continue to climb in June. The ordinary IFO indexes (not the diffusion indexes) are at their highest marks since January 1991 for both the headline and the current index. The expectation index has been higher than its June value 14% of the time.

The IFO ordinary indexes (see Chart) continue to climb in June. The ordinary IFO indexes (not the diffusion indexes) are at their highest marks since January 1991 for both the headline and the current index. The expectation index has been higher than its June value 14% of the time.

Diffusion indexes

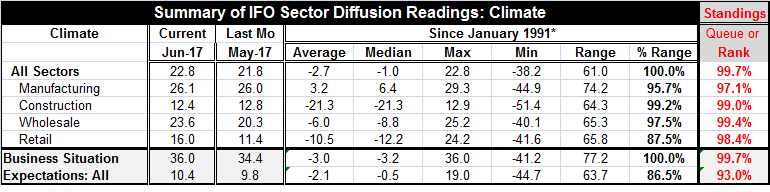

The diffusion indexes (see Table) show that the sector and business situation indexes are at all-time highs on the same timeline as for the ordinary indexes pictured in the chart, back to 1991. As with the level-based indexes, expectations are not as strong as the other gauges. In diffusion terms, the expectation index has been higher 7% of the time. The various sector indexes are strong at their 97th queue percentiles or higher across the board. On a percentile of range basis, they are similarly strong with the exception that the retail sales sector resides in 'only' the 87.5 percentile of its historic range (high-low) of values. The range percentile readings evaluate the current index relative to its historic highs and lows. An 87 percentile standing tells you that the index is at the 87% mark of the high-low range with roughly 87% of the range below it and 13% above it. The percentile standings look at the current observation and evaluate it based on what proportion of the time it is lower or higher. On that basis, an 87 percentile standing implies that it is lower 87% of the time and higher about 13% of the time. The two gauges measure slightly different things and together they help to position the index with some historic perspective and serves to provide an image of sorts of where the index is positioned without looking at a graph.

In June, the IFO showed advances in all its diffusion indexes except construction. That index slipped to 12.4 in June from 12.8 in May. The manufacturing index barely notched a gain, rising to 26.1 from 26.0.

Among the ordinary index level indexes, the current situation index has the strongest year-on-year gain since July 2011 and the 34th strongest year-on-year gain back to January 1991. Since early-2013, the current index has been floating in and out of positive growth rates; there have been three episodes of negative year-on-year growth rates for the IFO current situation index. However, since late in 2016 the index has been rising steadily and accelerating steadily. The business climate index has had essentially companion cycles to the current index but in this episode it has already stopped accelerating. In the 2014 episode, both of these indicators accelerated then contracted. In 2013 the business climate index topped-out first as it is doing again this year, at least preliminarily. It's too early in the cycle to know if this is a topping signal or not. For now the German economy seems to be firing on all cylinders and accelerating. But we know that acceleration phases run out of gas and this one is already driving at a pretty high speed, high enough that it won't be sustained for much longer. Neither is it clear what will happen when this acceleration phase runs out. The German unemployment rate is at a post reunification low, but there are few signs of economic distress or excesses of pressures that might be caused by growth that is taxing economic capabilities.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief