Global| Aug 27 2018

Global| Aug 27 2018German IFO Gauge Rises to 5-Month High

Summary

The German IFO index rose to 105.3 in August from 104.6 in July, striking its strongest posture since it logged a value of 105.9 in March. Still, from June 2017 through February 2018, the index had carried readings of 106 or stronger, [...]

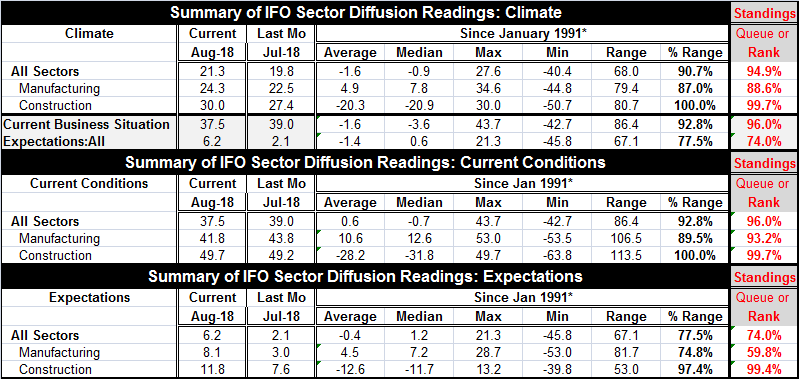

The German IFO index rose to 105.3 in August from 104.6 in July, striking its strongest posture since it logged a value of 105.9 in March. Still, from June 2017 through February 2018, the index had carried readings of 106 or stronger, usually stronger. Despite the month’s rise, the index remains in the 104.4 - 105.9 range it has occupied since March of this year. The table below presents the diffusion values for the index and its components.

The German IFO index rose to 105.3 in August from 104.6 in July, striking its strongest posture since it logged a value of 105.9 in March. Still, from June 2017 through February 2018, the index had carried readings of 106 or stronger, usually stronger. Despite the month’s rise, the index remains in the 104.4 - 105.9 range it has occupied since March of this year. The table below presents the diffusion values for the index and its components.

Continuing on this theme, despite the weaker performance over the last five months, this month’s IFO index still has a percentile standing at 94.9%; that tells us the index has been stronger only about 5% of the time historically – a still impressive outcome.

The climate readings all are extremely high based on their queue standings. Manufacturing is the weakest reading at a standing of 88.6% despite a relatively solid gain in the month. The construction sector improved and stands at its all-time high mark.

The August overall business situation eased on the month with its diffusion reading falling to 37.5 from July’s 39. However, it still logs a 96th percentile standing. Expectations that rose rather sharply on the month gained to 6.2 from 2.1. Nonetheless, the August reading has only a 74th percentile standing, just out of the top 25% of its observations historically.

Manufacturing saw current conditions fall by two points on the month to a 93.2 percentile standing. Construction’s current reading gained and stood at an all-time high.

Expectations for both manufacturing and for construction improved sharply in August. Construction was boosted to a 99.4 percentile standing, but manufacturing only has a 59.8 percentile standing for expectations. Despite a manufacturing jump in expectations from 3.0 in July to 8.1 in August, the sector remains as one showing only moderate expectations for the future, modestly above its historic median (which occurs at a standing of 50%).

An IFO economist predicted that the German economy would advance by 1.8% or 1.9% this year after the IFO issued the results of its monthly survey. The previous outlook had been solidly for 1.8% growth. The economist cited strong domestic results which would dominate international concerns like those stemming from the Turkish crisis or the turmoil over Brexit. The German automotive and services sectors were reported to be bright spots. But since German exports are 40% of GDP, it is pretty hard to claim that the domestic German economy is insulated in any way from foreign events. Moreover, Germany continues to show heightened tensions over the presence of migrants. In Chemnitz in Eastern Germany, a march developed in what was supposed to be a peaceful celebration of the city’s birthday. A crowd of protestors, estimated to be made up of 800 people, was instigated by a far-right group that said it wanted to show who was in charge in the city after a German man was fatally wounded in a fight in which several ‘foreigners’ were involved. The marchers threw bottles at the police. The march and the marcher’s militancy took local police by surprise. Extra police were called in from Dresden and Leipzig. With such things flaring up in Germany, even with Angela Merkel’s coalition government in sharp opposition to such things, it remains difficult not to harbor reservations about the potential for growth in Germany this year.

The sharp turnaround in the IFO index probably is related to the EU and U.S. decision to negotiate their differences instead of launching an all-out trade war as had been threatened; this was alluded to by Clemens Fuest, President of the IFO who commented on the report. As such the rebound in sentiment is probably fact-based. But the Markit PMI indexes of activity are showing only a slow turnaround in Germany and in EMU current conditions. The global situation remains risky with the U.S. and China still battling. In general, there is an environment fraught with various tensions not limited to the trade front. Iran is appealing to the International Court of Justice to have U.S. sanctions removed.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief