Global| Jul 25 2018

Global| Jul 25 2018German IFO Continues to Bend Lower As Activity Slows

Summary

IFO Indexes The German IFO survey shows that the three major aggregate gauges: climate, current situation and expectations are all weakening year-over-year. The current situation is having its first year-on-year decline in some time. [...]

IFO Indexes

IFO Indexes

The German IFO survey shows that the three major aggregate gauges: climate, current situation and expectations are all weakening year-over-year. The current situation is having its first year-on-year decline in some time. Up until now, it had simply been losing momentum steadily. Declines in the year-over-year expectations index are getting progressively deeper. However, the IFO index numbers show that the climate index is up by a tick month-to-month and the current situation is better by two-ticks as expectations remain dead flat in July at June’s level. The percentile standings tell where the current index sits relative to its upper and lower extremes. The climate index is some 12% off its all-time high, the current index is 6% below its high and expectations are a large 29% off their high. Alternatively looking at this month’s values as a ranking or standing in an historic queue of numbers, the current situation is strongest having been stronger only about 2% of the time. The business climate has been better only about 8% of the time. But business expectations have been better 42% of the time, leaving that metric quite a bit closer to its historic median (at the 50th percentile standing).

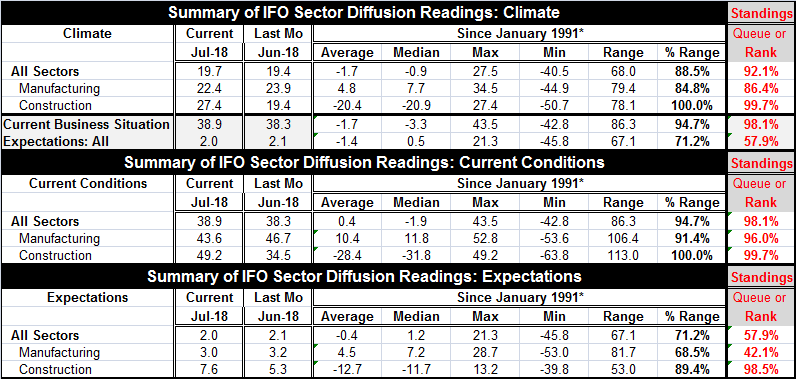

The German IFO sector indexes show weakening conditions except for construction. The aggregate indexes show a tug of war between current conditions that are still edging higher and expectations that are edging lower. Climate, on balance, is still improving. The diffusion readings echo the results of the IFO indexes.

Turning to sectors, the diffusion indexes show that the all sector standing in its 98th percentile reflects high standings for both manufacturing and construction. Expectations, however, are split. The overall diffusion standing is at its 57th percentile. But that is a result of a disparate readings, a very strong construction standing and a below median reading for manufacturing (42.1 percentile standing).

On balance, the IFO indexes and the Markit signals are still quite solid. There are few signs of actual weakness but plenty of evidence of weakening. Growth is still in gear. Yet, there is clearly erosion in play. And the fundamentals in Germany and Europe are worrisome enough that a focus on the changes in these indexes seems most appropriate.

The IFO gauges give us the same signals that we have been getting from the Markit indexes. Germany and Europe have come down from their recent strong levels of activity. Myriad economic and political forces are battering the global and European economies. Individually European economies have their own problems with a variety of local political issues as well.

Construction remains hot; manufacturing is not

Financial conditions and outlook

Financial conditions and outlook

The second chart shows that financial conditions in the EMU remain weak and guarded. In June, M2 growth receded slightly but still is growing strongly over the past two months but still lethargically overall. Total and private credit both contracted in June and that is not a good sign for growth. Private sector credit is an important ingredient for growth and yet it declined in June for the first time since December of last year. In money center countries, real money balance growth rates hover at a pace of 2.5% or less. Real money growth is very weak in the U.K. There is no evidence of global stimulus from money or credit growth. As we see from the IFO report and other private sector surveys, economies apart from the U.S. are losing momentum. It is going to make monetary policymaking more interesting as the Fed faces a tight economy and is on policy tightening track while Europe faces a very different and much weaker situation.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief