Global| Feb 09 2010

Global| Feb 09 2010German: HICP Moderate But Accelerating

Summary

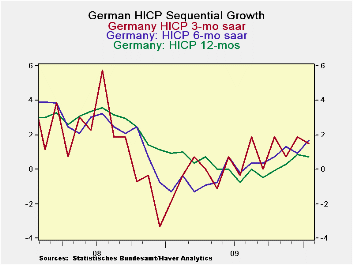

Germany’s HICP and domestic CPI show modest inflation in Germany but headline inflation is still in a steady upward progression. Since the headline rate for the HICP is only 0.7% that is not disturbing at all. The HICP core is not yet [...]

Germany’s HICP and domestic CPI show modest inflation in Germany but headline inflation is still in a steady upward progression. Since the headline rate for the HICP is only 0.7% that is not disturbing at all. The HICP core is not yet available but the domestic German CPI measure shows core inflation at 0.8% Yr/Yr and yet dropping at a pace of 0.8% over the most recent three months. Domestic inflation shows modest diffusion. Inflation is accelerating over six months in only 54% of the categories and inflation is accelerating over three-months in only a bit more than one-quarter of the categories.

Germany, a big part of the e-zone and its inflation measure, shows inflation pressures are still contained but not entirely dormant. At this point that is good news since we want inflation to stay under control but we do not want it so docile that the economy appears to lack any life. The economy needs to make a recovery so the existence of some price pressure is a good signal, too.

Germany has a mixed mission. It is to keep inflation under wraps and still to generate recovery. The German CPI and HICP seem consistent with those goals.

| German HICP and CPI details | |||||||

|---|---|---|---|---|---|---|---|

| Mo/Mo % | Saar % | Yr/Yr | |||||

| Jan-10 | Dec-09 | Nov-09 | 3-Mo | 6-Mo | 12-Mo | Yr Ago | |

| HICP Total | 0.1% | 0.1% | 0.2% | 1.5% | 1.7% | 0.7% | 0.9% |

| Core | #N/A | 0.2% | -0.1% | #N/A | #N/A | #N/A | 1.2% |

| CPI | |||||||

| All | -0.1% | 0.2% | 0.1% | 0.7% | 1.1% | 0.8% | 0.9% |

| CPIxF&E | -0.3% | 0.1% | 0.0% | -0.8% | 0.0% | 0.8% | 1.2% |

| Food | 0.5% | -0.1% | 0.4% | 2.9% | -0.5% | -1.3% | 1.0% |

| Alcohol | 0.1% | 0.1% | -0.1% | 0.4% | 1.1% | 3.6% | 1.9% |

| Clothing & Shoes | -1.9% | 2.2% | -1.3% | -4.2% | 2.8% | 0.3% | 1.0% |

| Rent &Util | 0.1% | 0.1% | 0.0% | 0.7% | 0.7% | -0.3% | 2.4% |

| Health Care | -0.3% | 0.1% | 0.1% | -0.4% | 0.2% | 0.9% | 0.9% |

| Transport | 0.5% | 0.2% | 1.4% | 8.7% | 10.0% | 4.6% | -2.7% |

| Communication | -0.3% | -0.2% | -0.3% | -3.5% | -2.0% | -1.9% | -3.0% |

| Rec &Culture | -0.5% | 0.0% | -0.5% | -3.9% | -1.8% | 0.1% | 1.2% |

| Education | 0.1% | 0.5% | 0.8% | 5.9% | 4.6% | -1.5% | -4.3% |

| Restaurant& Hotel | 0.1% | 0.5% | 0.1% | 2.6% | 2.0% | 1.5% | 3.1% |

| -0.7% | 0.3% | -0.3% | -2.9% | 0.7% | 1.3% | 1.4% | |

| Diffusion | 27.3% | 54.5% | 36.4% | -- | |||

| Type: | Diffusion: Current Compared to | 6-mo | 12-mo | Yr-Ago | -- | ||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief