Global| Nov 13 2008

Global| Nov 13 2008German GDP Drops in Q3

Summary

German GDP drops -German GDP drops by 2.1% saar in 2008-Q3. As has been the case in Germany for sometime, the Bundesbank continues to blame the thrust of events on outside forces. Germany's Bundesbank said that the global growth [...]

German GDP drops -German GDP drops by 2.1%

saar in 2008-Q3. As has been the case in Germany for sometime, the

Bundesbank continues to blame the thrust of events on outside forces.

Germany's Bundesbank said that the global growth slowdown was to blame

for Germany slipping into recession this year, after gross domestic

product data on Thursday showed that its economy shrank by 0.5 percent

in the third quarter of the year.

Germany as Victim: "National production in

Germany has significantly fallen in the summer ... compared to the

previous quarter. The broad global economic slowdown is now

increasingly making its presence felt," the German central bank said in

a statement.

Germany as free rider - There is no

disputing these facts but the Bundesbank does not point out that

Germany has an economy geared to exporting and one that therefore is

set to do better when the world economy does better and to do worse

when the world economy does worse. Blaming the world economy in this

circumstance is like the caboose blaming the engine for going too slow.

This arrangement is one that Germany has sought and has prospered under

in the past. Now that it is not working, it is not Germany’s fault.

Right.

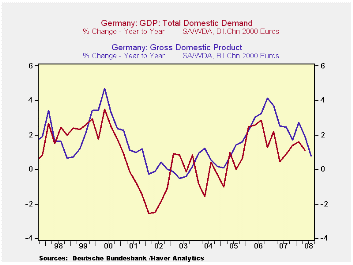

Germany as braggart laggard - In the

chart at the top of this report notice that the RED German GDP line

usually exceeds the blue line. The red line is for all of GDP. The blue

line is for German domestic demand alone. Germany has been pulled ahead

by the global economy consistently since 2003. I don’t understand all

this complaining and the ongoing assertion of German superiority we

have been hearing from the Bundesbank, from the German finance ministry

and others. It has been about growth, the euro and German banks -

everything.

Giving or taking? No one forced German

banks to buy and hold the bad assets they have accumulated. Yet they

did that and suffered after the Bundesbank assured us that German banks

had no such problem. Germany is an intrinsically slow growing economy

with a high rate of unemployment. Its choice has been to accept that

and to seek growth through exports instead of though domestic means. At

a time that the US has had a big payments imbalance, and developing

countries were pursuing strategies of export-led growth, Germany would

have contributed to the world economy more by putting its unemployed to

work and by exporting less.

Global summit and blame: We are preparing for a global summit

where countries will sit across the table from one another and listen

to the pot calling the kettle black. Be sure that there will be a lot

of blaming and evading of blame at this G-20 meeting. But be clear that

as the center country in a currency system like this, if countries

choose a lower rate VS the dollar, they get it, and the US gets the

resulting deficit from trade.

What to fix: The currency monetary system is not set up to

encourage currencies to trade at their proper parities or to remedy

balance of payments imbalances when they arise. Breton Woods collapsed

because of disputes arising over payments imbalances and the US

tendency to grow faster than its trading partners (…and amass deficits

and lose gold reserves). And now some 35 years later these same root

differences are the nemesis of the Bretton Woods’ successor system of

fluctuating exchange rates. It’s not a matter of ‘is Germany better’

but rather ‘is it doing its share?’ Is it contributing to the world

order or is it adding to the burden or the excess? That is the real

question.

| German GDP | ||||||||

|---|---|---|---|---|---|---|---|---|

| Consumption | Capital Formation | Domestic | ||||||

| GDP | Private | Public | Total | Housing | Exports | Imports | Demand | |

| % change Q/Q; X-M is Q/Q change in Blns of euros | ||||||||

| Q3-08 | -2.1% | #N/A | #N/A | #N/A | #N/A | #N/A | #N/A | #N/A |

| Q2-08 | -1.7% | -2.6% | 1.2% | -2.0% | -13.5% | -0.6% | -5.3% | -4.1% |

| Q1-08 | 5.7% | -1.4% | 4.6% | 6.7% | 24.6% | 8.9% | 13.2% | 6.7% |

| Q4-07 | 1.4% | -0.8% | 0.2% | 16.0% | 1.6% | 5.2% | -1.2% | -1.7% |

| % change Yr/Yr; X-M is Yr/Yr change in Gap in Blns of euros | ||||||||

| Q3-08 | 0.8% | #N/A | #N/A | #N/A | #N/A | #N/A | #N/A | #N/A |

| Q2-08 | 1.9% | -0.9% | 1.9% | 6.5% | 3.0% | 5.1% | 4.2% | 1.1% |

| Q1-08 | 2.7% | 0.5% | 1.6% | 8.8% | 3.0% | 6.7% | 5.1% | 1.6% |

| Q4-07 | 1.7% | -1.3% | 2.0% | 8.3% | -2.7% | 3.2% | 2.7% | 1.4% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief