Global| Feb 06 2018

Global| Feb 06 2018German Foreign Orders Soar; Domestic Orders Bore

Summary

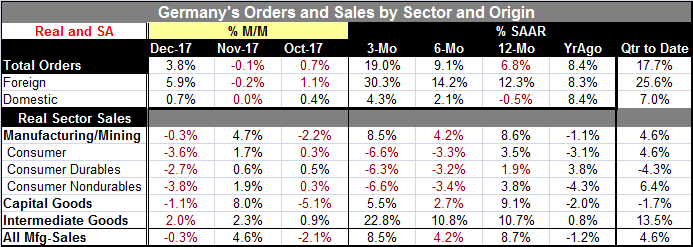

German orders are hopped up on foreign demand. In December foreign orders surged, rising by 5.9%, as domestic orders waddled ahead by 0.7%. Still, both foreign and domestic orders are accelerating from 12-month to six-month to three- [...]

German orders are hopped up on foreign demand. In December foreign orders surged, rising by 5.9%, as domestic orders waddled ahead by 0.7%. Still, both foreign and domestic orders are accelerating from 12-month to six-month to three-month as sequential growth rates get larger on shorter horizons. But foreign orders are up by 12.3% over 12 months. And even with a 0.7% gain in December, domestic orders are lower by 0.5% over 12 months. Germany is advancing on demand from abroad not at home, as though it were an Asian economy (except that Asian economies are not doing this half as well at this game these days). An added problem is that global demand is only just recovering and Germany is siphoning off a large share of that to an economy that is close to overheating.

What is clear is that German growth is being pushed higher by foreign orders. A look at German capacity utilization (see Chart on the right) shows that capacity use in Germany is uncharacteristically high. Except for a brief period around 2006-2007, German capacity use has not seen these kinds of usage rates over the last 25 years. And the Bundesbank has been leaning on the ECB to dismantle its stimulus programs and to begin to move toward restraint.

The picture that emerges for the EMU is not one that really sees that as the best solution. The rest of the EMU has grown by much less than Germany in this cycle. Other EMU nations do not generally have such high capacity usage or the historically low rates of unemployment (lowest since German reunification!). A more equitable solution would be for the euro to be allowed to float to higher levels. While Europeans are wary of this, it might be the better solution. The euro is already under sporadic upward pressure on the back of anticipated ECB policy changes. A rising euro would reduce the competiveness of all EMU nations and could slow growth, but so would higher interest rates. A higher euro would in addition put downward pressure on inflation at a time that the ECB is still not hitting its inflation target and for that reason alone might be undesirable (although raising rates has that same effect).

On balance, there are few actions the ECB can take that would be wholly desirable. Among them doing nothing at all might be the most consistent with its goals. Doing nothing would take pressure off of interest rates and off the euro. Both of those would be pro-growth (compared to current policy) and would be policies that would not keep downward pressure on inflation. And while the ECB is procrastinating making more aggressive moves, it has a public plan to be less accommodative and plenty of pressure to speed things up in that direction. More fiscal stimulus is exactly what the doctor ordered in this situation, but because of budget constraints across most members, that is not going to happen. Moreover, fiscal policy is still decided at the national level not at a consolidated monetary union level except when a country has been found in violation of its Maastricht responsibilities. At that point, the EU Commission pounces.

The impact of a stronger euro policy is that it might target Germany more than other countries because Germany is such a prolific exporter. Germany is at least near an overheating threshold that it could be pushed back from if the euro were to rise. A stronger euro would provide restraint to inflation possibly encouraging a looser monetary policy to persist for longer. For the time being, inflation is not stimulated and EMU money and credit growth are still weak. With a more gradual move to normalcy, the deflationary impact of a stronger euro could be damped. And the rest of Europe still needs monetary policy accommodation. The stronger euro route might be the lesser of two evils.

On balance, I have no information saying that any such moves are being contemplated, but they would make sense although would probably not be to the liking of Germany. A switch over to a tighter monetary policy might just bring with it a stronger euro anyway and then the EMU would be under the double whammy of a stronger euro and higher interest rates with inflation still undershooting. How does that look like good policy?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief