Global| Oct 09 2018

Global| Oct 09 2018German Exports and Imports Weaken in August

Summary

Trade trends and conditions With exports at 47% of GDP, it is no wonder that Germans watch export performance very closely and worry about even small perturbances to export trends. In August, German exports fell by a tiny 0.1%, but [...]

Trade trends and conditions

Trade trends and conditions

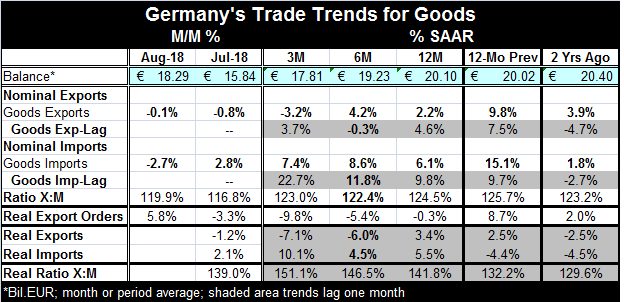

With exports at 47% of GDP, it is no wonder that Germans watch export performance very closely and worry about even small perturbances to export trends. In August, German exports fell by a tiny 0.1%, but the drop was unexpected coming as it did on the heels of a 0.8% decrease in July. German exports are falling at a 3.2% annualized rate over three months, rising at a 4.2% pace over six months, and rising by just 2.2% over 12 months. One year ago at this time, the German year-on-year export growth was at 9.8%. Times change.

Imports, also falling in August, dropped by a larger 2.7%. But that drop came on the heels of a 2.8% rise in July. Imports are rising at a 7.4% annual rate over three months, with six-month growth at an 8.6% pace and year-over-year growth at a 6.1% pace. Imports also are weaker than their year-ago performance when they rose by 15.1% over 12 months.

Is surplus reduction for real?

At 18.3 billion euros in August, the German trade surplus is larger than its 15.8 billion euro surplus in July. But the average deficit size has been gradually falling as its 12-month to six-month to three-month average has continued to drop. The German 12-month, previous 12-month and previous to that 12-month trade surpluses all have hovered at the 20 billion euro mark- that’s three years of stability at 20 billion euros. The drop in the three-month average of the surplus over three months is the largest drop in that surplus measure since February 2009 during the period of the Great Recession. It is the largest surplus reduction in 9.3 years and as such may be a meaningful signal of smaller surpluses to come.

German nominal exports as well as real export orders are on the decline as the growth pace for both over 12 months is under 2.5%. It is the weakest growth for German exports and real orders since mid-to-late-2016. German imports have cycled through higher and lower growth rates as well, but even with the slowing in imports, import growth at its recent slower pace is still closer to 6%. Some of this is attributable to rising energy costs and some to the rise in the real euro exchange rate.

Reason for concerns?

There is reason to worry. Germany’s exports, real export orders and industrial output all have fallen on weak patches at the same time. That constellation of events makes it more likely that there are real forces at work impeding the German industrial sector and not just some statistical noise at work. The PMI gauges from Markit globally and for the EMU have been weakening as well. At its meeting in Bali in Indonesia, the IMF announced weaker growth forecasts for the global economy in the period ahead, the first forecast reduction since it began hiking its outlook in this cycle.

Indicators and actions reconciled or at loggerheads?

The OECD leading economic indicators (LEIs), released yesterday, also pointed to a weakening in growth signals and this was a very broad weakening that spanned developed and developing countries with few exceptions. Of course, markets globally have been fretting; the Asian stock markets are at a 17-month low by some indictors. Europe has been losing confidence as well. I will not here repeat the litany of negative forces that are playing out across Europe as well as globally. But let’s look at central banking actions.

While the Bank of England has made some tentative moves to withdraw its post-Brexit splurge of liquidity, the European Central Bank is still in the planning stages and the Bank of Japan is in the thinking stages. In China, aggressive actions of various sorts have been made to try to stem the tide of weakness that is in train there following U.S. trade actions against China. China is still full throttle on stimulus.

Only in the U.S. has a program of tightening been in place since late-2015. It is a good time to remember that monetary policy works with lags. And just as the U.S. central bank is declaring victory on hitting its inflation target (that it has undershot persistently since its inception in 2012), it may be that contractionary effects are in play reducing growth. Is there such a ‘new kid in town?’ It is often said that monetary policy works with long and variable lags. Economists prefer this langue to admitting that we don’t know how it really works at all. But in fact, there is little difference in the two approaches. It might be a good time for the Federal Reserve to replace its machismo stance on monetary policy with one that is more modest and less ambitious for a while to see what is really happening with growth. The pick-up in growth experience in the U.S. recently may turn out to be a minor tempest in a cooling global teapot. Won’t it prove embarrassing if the Fed keeps throwing ice around the pot making the brew undrinkably cold instead of palatable?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief