Global| Jan 25 2018

Global| Jan 25 2018German Confidence Rises...And So Does the Euro

Summary

The German GfK look-ahead consumer confidence metric for February shows German confidence headed for a new high. Conditions in the labor market are touted as driving consumer attitudes. The three components of the GfK index, [...]

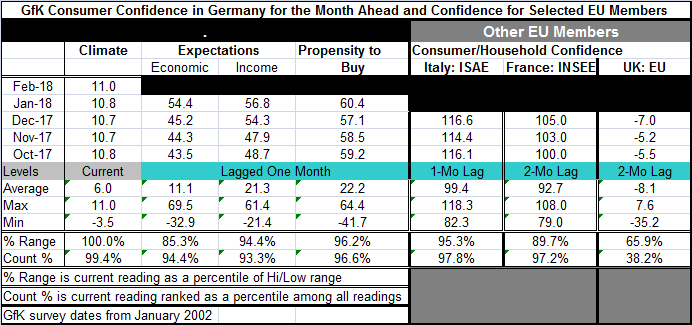

The German GfK look-ahead consumer confidence metric for February shows German confidence headed for a new high. Conditions in the labor market are touted as driving consumer attitudes. The three components of the GfK index, expectations for economic conditions, for income and buying conditions all stand at about the top 5% of their respective historic queues of data (count %).

The German GfK look-ahead consumer confidence metric for February shows German confidence headed for a new high. Conditions in the labor market are touted as driving consumer attitudes. The three components of the GfK index, expectations for economic conditions, for income and buying conditions all stand at about the top 5% of their respective historic queues of data (count %).

Despite great differences in growth and economic performance, both Italy and France also post extremely strong readings for consumer confidence (both lag the German reading by two months) with queue standings well within the top 5% for both of them. Both France and Italy showed further improvements in confidence in their most recent observations. The laggard, of course, continues to be the U.K. where the future is a big question mark as talks about Brexit drag on and on. Despite that, U.K. economic data continue to perform as exemplified by the recent drop in the U.K. unemployment rate to a 42-year low; yep, that's 42-year low not 42-month low. And yet, even with this very strong labor market, U.K. confidence is less than midstream...so much for the labor market calling the tune on consumer confidence.

While GDP growth over the last decade shows very different results for these countries, with Germany flying high and Italy stuck and barely growing at all, on balance consumers in these countries currently are feeling good. With that as background, the ECB just met and kept policy on hold while Mario Draghi did his best version of Winston Churchill trying to convey sheer determination to reach his inflation target against all odds. Unfortunately, market views on Draghi already have shifted. Draghi is a lame duck; while his term is not up until next year, market wags are already handicapping his successor and discounting Draghi's resolve and his ability to continue to lead against German intentions. Draghi clearly came to this meeting trying to stop expectations which have been steamrolling for a faster EMU path of rate hikes and a quicker dismantling of its stimulus programs. All that has ratcheted the euro higher, something that will tend to keep inflation low (read 'below target') as well as to impede the evolution of growth in the EMU. Draghi came out at this press conference being as strident as he could, but markets were prepared for this strategy and were not buying it. On balance, markets seem to see Draghi as trumped by events and the events are strengthening the German (Dutch and Austrian) opposition to ongoing easy monetary policy, especially with a clearly improving economy as a driving tailwind to their view.

In short, do not try to understand today's market reactions by reading what Draghi said. Understand today's market actions by looking at the economic data. Markets are coming to the belief that whatever the ECB says, its policy path is increasingly carved out for it by the reality of the data. The opportunity for the use of rhetoric or moral suasion or whatever you want to call it is becoming limited. Markets can smell blood in the water: the dollar is falling as the euro is rising. And that is the new reality with the U.S. Treasury Secretary giving the dollar a push and economic data giving the euro a pull.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief