Global| Jul 23 2020

Global| Jul 23 2020German Confidence Makes Another Sharp Gain

Summary

The GfK consumer confidence index that projects German confidence for the month ahead is up by 9.1 points in August, the second strongest gain in its 223-month history. The strongest gain came last month at 9.2 points. After dropping [...]

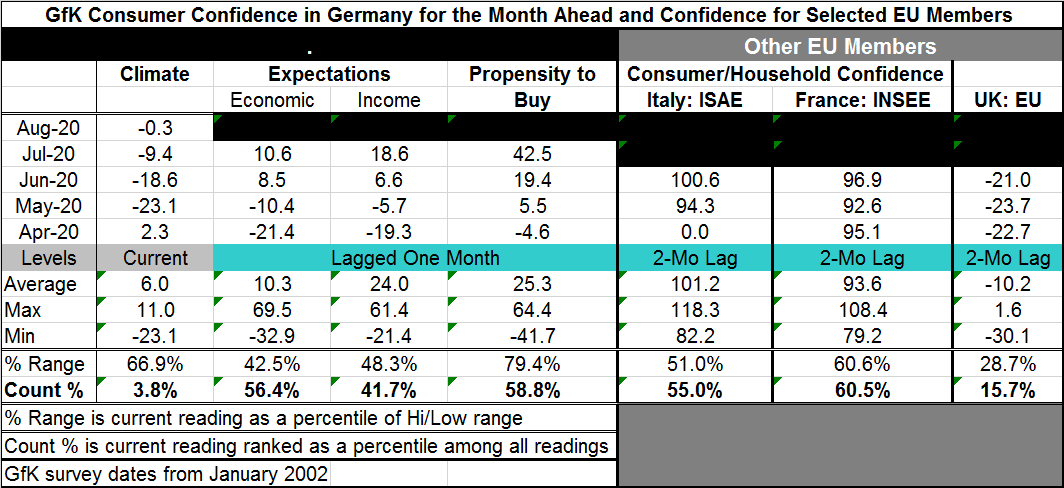

The GfK consumer confidence index that projects German confidence for the month ahead is up by 9.1 points in August, the second strongest gain in its 223-month history. The strongest gain came last month at 9.2 points. After dropping for four months in a row culminating in a severe drop of 25.4 point in May 2020, the GfK climate index is now advancing rapidly.

The GfK consumer confidence index that projects German confidence for the month ahead is up by 9.1 points in August, the second strongest gain in its 223-month history. The strongest gain came last month at 9.2 points. After dropping for four months in a row culminating in a severe drop of 25.4 point in May 2020, the GfK climate index is now advancing rapidly.

However, if we rank the GfK index level rather than its change, the climate ranking is 205 out of 223 observations, still a very weak level of confidence. The mixed message is that while confidence has been rising rapidly in Germany in the wake of its massive decline it is still at level that should be construed as weak in an historic context. German optimism has a good way yet to run to register as a strong reading in an historic context.

The headline reading for climate in August is -0.3, not yet back to a net positive reading despite strong jumps in June and July.

Component readings for the GfK report lag by one month. Economic expectations have improved steadily and strongly after posting three sizable negative readings in March, April and May. In June economic expectations rose to 8.5 from May's -10.4 and now in July expectations are up more modestly to 10.6 from 8.5. Economic expectations still have a modest rank or count standing in their 56.4 percentile, just above their historic median as of July.

Income expectations are up strongly in July, rising to 18.6 from June's 6.6. In April and May income expectations logged sizable negative values; May's -5.7 was a sharp gain from April's -19.3. However, even with these gains, income expectations sit below their historic median at a rank standing of 41.7%.

The propensity to buy has behaved a bit differently. Even as income and economic expectations were poor, various government actions were in place to try to sustain spending. The buying index weakened in March to 31.4 from 53.6 then dropped to a negative reading of -4.6 in April. The month of May saw an improvement to 5.5 with June rising to 19.4 and July surging to 42.5. The 42.5 level has a rank standing at its 58th percentile and counts as a relatively firm standing overall.

Confidence levels elsewhere in Europe are not as timely as for the German GfK, a metric that actually looks ahead. For Italy, France and the United Kingdom, the most current metrics lag by two months and address the month of June (when the GfK German climate index still had a -18.6 reading). As of June, Italy's confidence has a 55th percentile standing, France has a 60.5 percentile standing and the U.K. has a 15.7 percentile standing. Italy and France have readings from June that rank as high or higher that the GfK components and are much higher than the GfK headline for August. Even the U.K.'s low percentile standing is above the climate standing for Germany in August.

These comparisons show how different countries are reacting to the virus and how consumers handicap differently their assessments of conditions and their government's prospects for handling them. The EU has been bargaining and only this week concluded negotiations for an EU-wide support package in the face of damage done by the virus. The virus continues to ebb and flow, creating hot spots and then receding. As it does this, it also turns the dial on growth in the opposite direction as every heating up of the virus requires a cooling down of the economy. As such the outlook continues to be muted and uncertain. What we see in Germany is that the economy was hit very hard, but confidence in the authorities' ability to corral the virus and restore growth is improving apace. Even so, it still has a long way to go to get Germans back where they were before the virus struck.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief