Global| May 26 2020

Global| May 26 2020German Confidence Improves a Bit for June: GfK

Summary

The look-ahead view for German confidence in June from GfK shows some improvement for the headline gauge and also improvement for the component measures that lag by one month. GfK climate The GfK climate gauge fell very sharply in [...]

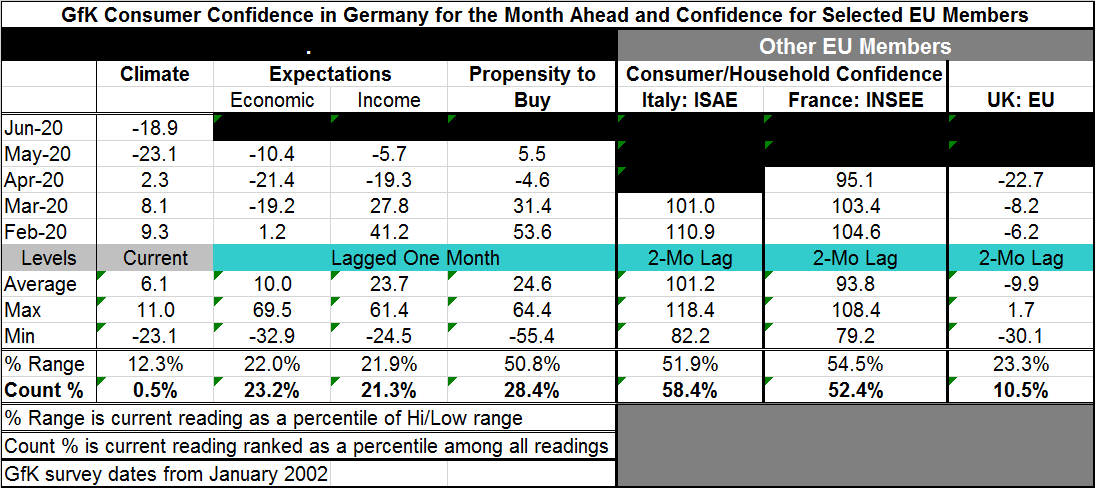

The look-ahead view for German confidence in June from GfK shows some improvement for the headline gauge and also improvement for the component measures that lag by one month.

The look-ahead view for German confidence in June from GfK shows some improvement for the headline gauge and also improvement for the component measures that lag by one month.

GfK climate

The GfK climate gauge fell very sharply in May; it had seen its gauge drop from a value above 10 in late-2018 and early-2019 to value in the 'high nines' in 2019. It then eroded sharply in early-2020; by April the GfK gauge was at 2.3 and from there it plunged to -23.1 in May. The fresh reading today for June is at -18.9, a small improvement from May and a still deeply negative reading.

Economic assessment

The economic assessment has fallen sharply. While there were flirtations with negative readings in late-2019, they ebbed and flowed into early-2020 vacillating between small positive and small negative readings. Then in March, the economic index fell to -19.2. Then it hit its slow reading of this cycle at -21.4 in April. This month's reading halves that assessment's weakness cutting the reading to -10.4 in May. That is up-to-date as this series gets; it lags the headline climate series by one month. Clearly the economic readings are weak, but in late-2012 to early-2013, there was a span of six-months in which the economic climate readings also were deeply negative. In the Great Recession, there were 12-months in a row from 2008-2009 with even larger negative readings. So while April's -21.4 low reading registers as particularly weak, May's reading at -10.4 has only a bottom 23rd percentile standing. That is weak, but it is not extreme. Germany is weathering the storm.

Income expectations

Income expectations had a reading in their 60s in 2017 but settled into a range of readings in the mid-50s or so though nearly mid-2019. In June 2019, income expectations slipped to 45.5. The reading continued to struggle in that lower range into early-2020. In February the index fell to 41.2 then it stumbled to 27.8 in March. It fell to its current cycle low at -19.3 in April, but with a fresh reading in May that weakness has been cut to -5.7. At that level income expectations, have a bottom 21st percentile rank or count standing. That is a similar standing as for economic expectations.

Propensity to buy

From late-2017 to early-2018, propensity to buy indexes hovered at a level at or above 60. Into 2018, that slipped to the mid-50s. After mid-2019, values in the low-50s and mid-40s were more common. In March 2020 a reading of 31.4 was recorded then the bottom fell out as April's reading fell to -4.6. Now the topical reading for May is up to 5.5, still well below previous ranges of values but off the negative path. The propensity to buy has a rank or count standing in its 28th percentile, slightly higher than those for economic and income expectations.

Summing up GfK

Clearly the standing for the GfK climate index at the 0.5 percentile is weaker than any of the other lagging gauges. Even so, all of the various GfK gauges are showing a tendency to turn higher. Germany is currently considering taking some of the special measures off their borders and offering more freedom of movement. It is making progress toward reducing restrictions in the wake and ongoing presence of the coronavirus and its various risks.

Elsewhere in Europe

The confidence readings lag much more in the rest of Europe compared in Germany where a look-ahead gauge is also available. We can see from the German data how much difference it makes to have a reading that is just one or two months older. In view of that, we can look at readings elsewhere but can make few comparisons because of temporal differences.

France and the United Kingdom post April readings while Italy's freshest reading is for March. Still, all three of these other confidence metrics in the table regardless of their timeliness show deterioration. The U.K. shows the most deterioration and it has been hit hard by the virus. But the U.K. had previously been struggling with its negotiations over Brexit. The U.K. finally did take action on Brexit and left the EU, but it is still negotiating trade terms and conditions with the EU. Italy was very hard hit by the COVID-19, but its readings lag baldy in terms of timeliness. Even so as of March, Italy's confidence gauge fell to 101.0 from February's 110.9. France's topical reading is for April at 95.1, a drop off from 104.6 in February. The standings of these various confidence indicators find Italy at a 58.4 count or rank percentile standing, France is at a standing at its 52nd percentile and the U.K. much weaker at a standing in its 10th percentile. Of course, as noted above, the U.K. has been fighting off a series of problems. Prior to the onset of the COVID-19 problems, there had been global angst over the ongoing trade conflict between the U.S. and China that contributed to a drop off in global trade.

Summing up

It is too soon to know much about the rest of Europe because the data there lag too much compared to Germany. But Germany shows both evidence that it is still being hit hard by the COVID-19 issue and evidence that consumers are beginning to see an improved future. For Italy, France and the U.K., all that we can see in the data is the slippery slope ahead. However, we know that in 'real time' all three of these countries, like Germany, are beginning to peel back various COVID-19 restrictions. As we all know, the future will be one with virus activity in play. There is a lot of effort to find a vaccine, but regardless of effort there is no guarantee a vaccine will be found although there seem to be already some 'treatments' that might reduce the severity of a coronavirus infection. Few countries are trying to generate 'herd immunity,' that means there will continue to be a risk of a second wave of infections. The global economy remains at risk as the disease for now still accelerating in Brazil and clearly still very active globally. There is no one making a forecast for the months ahead that does so without a caveat. Clearly the outlook remains speculative and more uncertain than in the past.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief