Global| Jan 29 2020

Global| Jan 29 2020German and Other EMU Consumer Confidence Strengthens

Summary

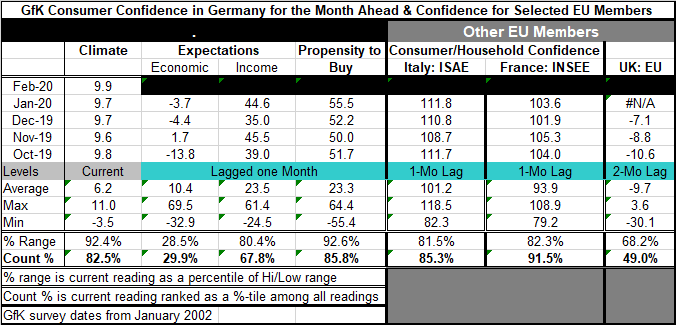

Germany's consumer confidence is projected to strengthen in February by the GfK survey as the climate gauge rises to 9.9 from 9.7 in January. The 9.9 reading is its strongest since June 2019 when it stood at 10.1. The top reading on [...]

Germany's consumer confidence is projected to strengthen in February by the GfK survey as the climate gauge rises to 9.9 from 9.7 in January. The 9.9 reading is its strongest since June 2019 when it stood at 10.1. The top reading on this gauge is 11 which was reached two years ago in February 2018. The GfK process projects confidence for the month-ahead when the end of the previous month is near. At the time, it does not provide any component information for the month ahead, just a projected comfort reading. The three components for this index have been tracking very different paths: the propensity to buy index rose in December and January. That two-month trend of improvement is consistent with a gain in the climate index in February. The income expectations reading fell sharply in December then rose nearly as sharply in January. Its path is impossible to sort out. The economy gauge has an unclear trend but has net negative readings in three of the last four months including the last two months. However, the negative assessment for January was not as adverse a reading as the one from December. Again, trend is elusive for this expectations component.

Germany's consumer confidence is projected to strengthen in February by the GfK survey as the climate gauge rises to 9.9 from 9.7 in January. The 9.9 reading is its strongest since June 2019 when it stood at 10.1. The top reading on this gauge is 11 which was reached two years ago in February 2018. The GfK process projects confidence for the month-ahead when the end of the previous month is near. At the time, it does not provide any component information for the month ahead, just a projected comfort reading. The three components for this index have been tracking very different paths: the propensity to buy index rose in December and January. That two-month trend of improvement is consistent with a gain in the climate index in February. The income expectations reading fell sharply in December then rose nearly as sharply in January. Its path is impossible to sort out. The economy gauge has an unclear trend but has net negative readings in three of the last four months including the last two months. However, the negative assessment for January was not as adverse a reading as the one from December. Again, trend is elusive for this expectations component.

However, the standing for Germany's climate is very high, higher only about 18% of the time. The propensity to buy reading (one month older, of course) has an 85.8 percentile standing. Income expectations have a 67.8 percentile standing and economic expectations have a very low, well below-median, 29.9 percentile standing. And yet despite concerns about the economy, income expectations are firm and buying plans are strong. However, a look at trends shows that despite a relatively firm standing for income expectations that series has been eroding for the past year and there is also a very minor trend erosion in play for the assessed propensity to buy. The angst exhibited in the economy index is not being ignored elsewhere and it is, in fact, spreading to other concepts of personal welfare despite this month's rise in the index.

Italy, France and the U.K.

Germany is not the only EU member with consumers' heads in the clouds. In Italy, despite ongoing political upheaval with conservatives fighting to make further political inroads, confidence in January rose for the second month in a row and its standing is in its 85th queue percentile- higher only about 15% of the time. In France, confidence made a partial rebound in January after a December drop and holds to a very lofty 91.5 percentile standing. The U.K., with its political upheavals behind it and Brexit of some sort ahead of it, has a (slightly) below median standing in its 49th queue percentile on a survey value of -7.1 for confidence in December. U.K. confidence has improved for two months in a row. Confidence in the U.K. has been range-bound largely between the values of -5 and -10 since late-2016.

Concerns go viral; countries take steps to control contagion; growth expectations are being cut

Of course, all bets on future growth are off for now as we have to step back and assess the impact of the coronavirus on global, regional and individual country growth. Today a German spokesman said it was too soon to assess the impact on Germany. Japan is worried about the economic impact on its country as it has just brought plane-load of citizens back from Wuhan. China has already put a number on its fear, saying that first quarter GDP growth could dip below 5%. This is easy to believe since the virus was in its early stages of discovery as the important Chinese New Year celebrations were scheduled and then all that was shelved and that will take a toll on Chinese GDP; the lunar New Year's celebrations are a significant economic event.

While it is hard to find a silver-lining in this cloud of killer-virus, one thing it has done is to quell the rioting and demonstrations in Hong Kong. There is nothing like the fear of transmitting a killer disease to keep people in their homes and off the streets. I wonder if this virus will create a ‘cooling off' period for Hong Kong protesters and help to smooth the way for some accommodation between these demands and what China will allow.

For now the impact of the virus is still spreading, there are more cases discovered and more deaths occurring. Nations are taking radical steps to bring citizens home, provide quarantines, and to reduce flights to China as well as to eliminate in flight amenities that otherwise might spread infection. It is too soon to handicap the impact of the virus but never too soon to worry about it or plan for it. In the U.S., the Fed meets today and it will be interesting to note what this key policymaking body has to say about risks and policy in the midst of these new setbacks.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief