Global| Feb 22 2018

Global| Feb 22 2018German and French Sector Confidence Slip

Summary

Business climate in Germany, as measured by the IFO index, has been on the rise, but it suffered a setback in February. Similarly, the French INSEE survey for manufacturing and for services has been on the rise, but each of these [...]

Business climate in Germany, as measured by the IFO index, has been on the rise, but it suffered a setback in February. Similarly, the French INSEE survey for manufacturing and for services has been on the rise, but each of these measures hit an air-pocket in February.

Business climate in Germany, as measured by the IFO index, has been on the rise, but it suffered a setback in February. Similarly, the French INSEE survey for manufacturing and for services has been on the rise, but each of these measures hit an air-pocket in February.

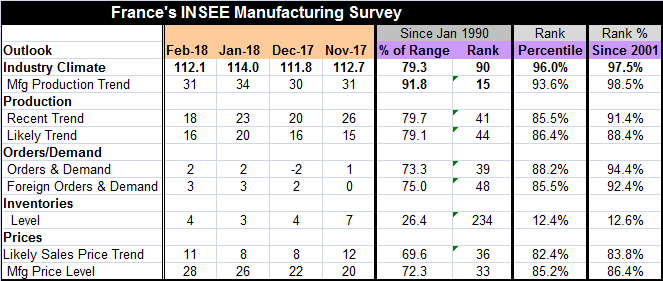

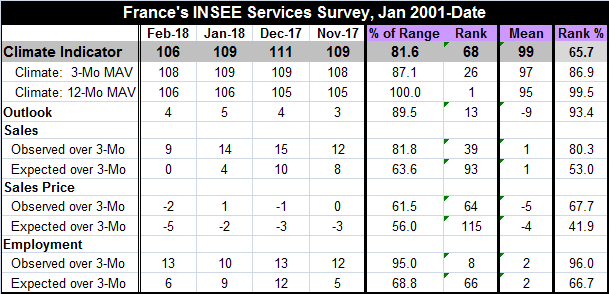

While these surveys still point to solid growth, there is a sense of backtracking. The French services climate indicator is at its lowest reading since May of last year. The French manufacturing trend has essentially been a one month stumble. The German IFO reading was last weaker in September of last year but has only been consistently weaker since June of last year.

The rankings of the various IFO segments continue to be exceptionally high. The weakest sector is retailing at its 93rd queue percentile standing. The overall business situation, as evaluated by the IFO, has been this good or better only 0.6% of the time while the queue standing for expectations is only in its lower 80th percentile decile at 81.7% (lower nearly 18% of the time).

For France, the INSEE survey puts the industrial climate in its top 2.5 percentile- another extremely strong reading. The manufacturing production trend is in its top 1.5 percentile. However, the recent trend and likely trend for production are somewhat weaker, a similar phenomenon to the IFO expectations standings that are weaker than its current readings. French orders and demand are still very strong. The price outlook is elevated with a strong reading in the mid to low 80th percentile range for manufacturing prices and the likely sales price trend.

The French services sector on this broader time span shows weaker prices with readings for expected prices substantially below their median in the 41.9 percentile (the median is at the 50th percentile). Expected sales are only in their 53rd percentile while observed sales over three months have a much stronger 80th percentile standing. Employment has a 96th percentile standing, but the outlook for employment has a much weaker 66th percentile standing. Do you see a trend here?

The bottom line is that there is some weakness creeping into even these strong readings. The German IFO index has weakening expectations- still at a strong level but much weaker than the standings for current observations. In France, we see solid and strong manufacturing readings with a service sector reading that is exaggerated by comparison with recent weak conditions and that suffers further when we step away from current readings to ask about expectations.

Also on the day, the U.K. released a Q4 GDP estimate that showed growth trimmed back by a tick to a quarterly gain of 0.4% instead of 0.5% and year-on-year growth of just 1.4%. Moreover, a quarterly 'distributive trades' survey for the U.K. has showed weaker retail sales expectations there.

Of course, monthly data ebb and flow. I cite theses various elements to counter the still growing belief that the global economy is gathering momentum. Conditions are improved from what they were one-and two-years ago. But what I fail to see is the sense of ongoing acceleration. As such, I still tend to see current growth as relying upon and being helped by the degree of accommodation in monetary policy. The lack of building inflation pressures and repeated softness in retail measures suggest that demand is still not on track. Perhaps the biggest misjudgment about demand being put back on track is in the U.S. where hurricane damage put a brave face on consumer spending, but now a lower saving rate and fading real earnings trends offer a starker view of the future.

Central bankers are quick to switch their worries over to inflation-fearing. They know that they will not get the credit for extending growth but will be blamed if they let inflation prop a foot in the door and gain entrance. But the largely unasked question is whether this sort of bias still suits the global economy well. Inflation and episodes of hyperinflation can color memories and dictate policies. But history is also replete with long episodes of stable prices. Central bankers are not asking themselves if they are making policy in a different risk regime from the pre-great recession predecessor periods. Essentially no one is asking the right questions. During a period in which academics in the U.S. have scrutinized inflation models and concluded that there is no model that has worked consistently well, the Federal Reserve continues to make policy that relies on its forward-looking beliefs. We should ask ourselves if this means that economics has become a religion instead of a science.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief