Global| Mar 14 2014

Global| Mar 14 2014German and European Inflation and the Dilemma-Zone

Summary

The chart shows the path of inflation for the three largest countries in the European Monetary Union (Spain is the fourth largest). It's clear from this chart that inflation for Germany, France and Italy tends to follow the same [...]

The chart shows the path of inflation for the three largest countries in the European Monetary Union (Spain is the fourth largest). It's clear from this chart that inflation for Germany, France and Italy tends to follow the same cycles. However, Italy in late 2011 and 2012 was stubbornly different from France and Germany. Italian inflation remained quite a bit higher and was flat while inflation fell persistently in the other two countries. Eventually Italian inflation broke lower, too, and is currently running slightly lower than either in France or Germany. However, this sort of thing does not eliminate price level misalignment for Italy. Italy's inflation rate has not been as far below German or French inflation as it was above it, when it was higher. Also for a longer period of time than it has been lower, Italian inflation was higher. Despite the fact that Italian inflation rates have come roughly back in line with those in Germany and France, that does not mean that Italian competitiveness has been restored. Far from it.

The chart shows the path of inflation for the three largest countries in the European Monetary Union (Spain is the fourth largest). It's clear from this chart that inflation for Germany, France and Italy tends to follow the same cycles. However, Italy in late 2011 and 2012 was stubbornly different from France and Germany. Italian inflation remained quite a bit higher and was flat while inflation fell persistently in the other two countries. Eventually Italian inflation broke lower, too, and is currently running slightly lower than either in France or Germany. However, this sort of thing does not eliminate price level misalignment for Italy. Italy's inflation rate has not been as far below German or French inflation as it was above it, when it was higher. Also for a longer period of time than it has been lower, Italian inflation was higher. Despite the fact that Italian inflation rates have come roughly back in line with those in Germany and France, that does not mean that Italian competitiveness has been restored. Far from it.

Germany used to be the persistently lowest inflation country in the euro area, but over the last year, out of the original members of the monetary union plus Greece, German inflation year-over-year is running as the fourth highest exceeded by Finland, Austria and France. The list of countries with lower inflation than Germany is impressive. It includes Luxembourg, Italy, the Netherlands, Ireland, Belgium, Portugal, Spain and Greece. Among these, Greece has the price level still falling year-over-year.

It's notable that the countries with inflation running below the German level include those countries that have undergone austerity in the EMU. This might tempt some to conclude that austerity has worked. But austerity has a long row to hoe and it is not successful until- or unless- it reaches the end of that row. That may prove to be its Achilles heel.

Despite these countries running inflation rates lower than Germany's for the last year, all of them are still behind Germany in terms of changes in competitiveness since the euro area was formed. There is still a long way to go for these countries to restore the competitiveness gap with Germany that was lost since the euro area fused exchange rates. For example, Greece's price level has risen by nearly 50% since the euro area was formed. Germany's price level has risen by only 28% over that period. That's a huge gap to be closed; until Greece closes that gap, it remains at a competitive disadvantage to Germany as well as to other member countries that were prone to lesser rates of inflation while the euro area was in place. Right now with extraordinary effort, Greece is gaining on Germany by 1.6% per year.only 13.75 years ((50-28)/1.6) of this left to go.

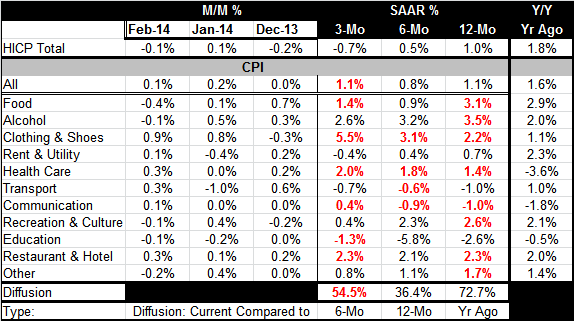

For Germany alone, there are slightly different trends emerging between the harmonized inflation measure for the euro area, the HICP, and Germany's traditional domestic CPI. The HICP inflation reading shows inflation falling from 1% over 12 months, to one-half of 1% over six months, to declining at a 0.7% annual rate over three months. This compares to a domestic inflation reading which is 1.1% over 12 months, 0.8% over six months, and then back to 1.1% over three months. The German domestic measure says inflation is actually higher over three months, at least.

The diffusion of German inflation measured off of the domestic price index shows that year-over-year inflation tended to accelerate in relatively more categories than it decelerated (diffusion>50%) with the diffusion reading of nearly 73%. However, over six months when the inflation rate fell to 0.8%, inflation was only higher than it had been over 12 months in 36% of the categories. Over three months when inflation ticked back up to 1.1% inflation compared to its pace over six months showed only minor tendencies to accelerate across the various categories with the diffusion reading at roughly 54%. That means inflation was accelerating in only 54% of the categories, barely more than half, which means barely more than neutral.

Germany is only one of three countries showing negative harmonized inflation movements over the last three months; the other two are the Netherlands and Portugal, both of which show deeper declines than Germany.

But German inflation is important for the EMU - perhaps the most important of all- since Germany has such a large economy that, in turn, has a large weight in the setting of the overall EMU inflation rate that the European Central Bank is committed to control.

When German inflation is very low, it puts a lot of pressure in other countries to keep inflation rates low to keep up with Germany. Since all countries are behind Germany in terms of their past inflation performance, in order to restore competitiveness other countries want to run inflation rates lower than Germany's. But when Germany's inflation rate is extremely low, it creates real problems for its fellow EMU members, especially those with high unemployment rates and a need to grow faster.

This inflation arithmetic is one of the reasons that I'm concerned about the ability of the EMU to continue with its cohesion. Other countries will be able to catch up to Germany faster if Germany runs a higher inflation rate. Traditionally, however, Germany has no taste to run a higher inflation rate. The more that Germany runs an inflation rate at or close to 2%, which is the ECB ceiling rate, the more that other countries are going to have to push their inflation rate below 2% across the board in order to keep inflation in the EMU in check and to keep the ECB from raising rates to fight off excess of inflation (and quash growth). Keeping inflation low outside Germany is something that would have to be done by most of the other EMU nations were Germany to run an inflation rate at or above 2%. Such persistent and informal coordination without the help of monetary policy would undoubtedly be difficult. Getting Germany to try to play this game might be even more difficult.

For the time being, the euro area is for the most part walking that walk and talking that talk. The euro area is cohesive and its inflation rate is under control. German inflation is being undercut by the countries that need to gain competitiveness on Germany. And all is well. And while all may be well, it's also true that growth is weak and improving slowly. One of the reasons that improvement is slow is because the weak growth outside of Germany is keeping the lid on prices there. The countries like Greece and Spain with low inflation but very high domestic rates of unemployment need to see growth pick up for the sake of political stability. But if growth were to pick up, the euro area might not be able to stand the attendant inflation in those countries, especially not in Spain, the fourth largest EMU country.

The countries with the highest unemployment rates need to grow the fastest to rebuild lost jobs. Yet, these are countries that have undergone austerity and need to improve their competiveness the most. While these two things are not incompatible -and are compatible in the long run- more generally the short-term tradeoffs are the opposite. The operational question is whether these nations that have so far to go in improving competitiveness, can find a way to do it fast enough while keeping inflation low before they are overtaken and blown apart by the political instability that comes from entrenched high unemployment. Therein lies the fate of the euro area and its dilemma with arithmetic.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.