Global| May 15 2020

Global| May 15 2020GDP across the EMU Region Takes a Deep Dive

Summary

While the chart shows the hint of GDP weakening ahead of the hit from the coronavirus, the virus clearly was a blow out of the blue. Among the nine early reporting long-standing EMU members, GDP fell everywhere except in Finland where [...]

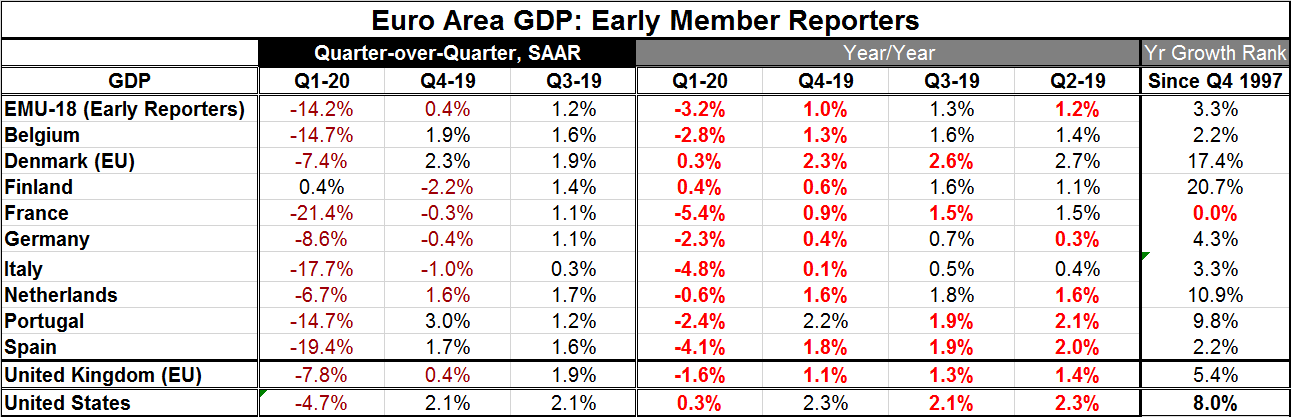

While the chart shows the hint of GDP weakening ahead of the hit from the coronavirus, the virus clearly was a blow out of the blue. Among the nine early reporting long-standing EMU members, GDP fell everywhere except in Finland where it rose 0.1% q/q for a 0.4% annual rate of increase. Elsewhere across the EMU, the annualized quarterly rates of change all fell and ranged from -6.7% (The Netherlands) to -21.4% (France). The EMU logs a decline for the region at a -14.2% annual rate.

While the chart shows the hint of GDP weakening ahead of the hit from the coronavirus, the virus clearly was a blow out of the blue. Among the nine early reporting long-standing EMU members, GDP fell everywhere except in Finland where it rose 0.1% q/q for a 0.4% annual rate of increase. Elsewhere across the EMU, the annualized quarterly rates of change all fell and ranged from -6.7% (The Netherlands) to -21.4% (France). The EMU logs a decline for the region at a -14.2% annual rate.

Europe is ‘ahead' of the U.S. with its GDP getting hit harder in Q1 compared to the U.S. (-4.7%) and the U.S. is bracing for a much harder hit in Q2. For example, U.S. retail sales just fell by 16.4% in April and industrial output also fell by double digits. Globally data are showing ongoing hits from the coronavirus; only China today showed a 3.9% gain year-over-year in industrial output in May as it was hit first and hard in Wuhan. Of course, what happen to China as well as when is still a matter of some dispute.

Among the nine early-reporting long-standing members in the table only two Denmark and Finland log year-on-year increases in GDP in Q1 2020.

France shows the deepest year-on-year drop in GDP at -5.4%, followed by Italy and Spain. Only Italy, Germany and France have consecutive quarterly declines in GDP on the books already. While GDP in Q4 2019 decelerated everywhere (except Portugal), there are no countries with two consecutive drops in year-on-year GDP. The recession process is just starting.

Recession or not here we come? It will be recession across the board, across the seas, across the world. And let's not lose sight of the fact that this is an induced economic coma. There is nothing ordinary or organic about it. Most of the stuff I read about the incoming data makes me cringe...like how consumer demand has dried up. Believe me, consumer demand has not dried up. Consumer SPENDING has dried up. These are different things. But when you shut all the stores and threaten people who go out with arrest or just scare them that they will get a killer-disease, people stay at home and do not shop. That does not mean demand is not strong or won't return once the restrictions are lifted. The retail data from the U.S. are in hand and it is clear that internet sales went through the roof along with food sales. Building materials sales were not at their worst (but were very weak) probably because the mega home improvement stores were another of the few retailers U.S. authorities allowed to stay open.

There will be a snap back in consumer sales but how fast and how full? That will depend on several things. It will depend on how badly consumer incomes and finances were hurt by the shutdown/lockdown. It will depend on what lingering fears have been instilled in consumers by these extreme measures. It will also depend on how quickly and thoroughly jobs bounce back as there is re-opening. If shops open very piece-meal, then jobs are reinstated very piecemeal as well and incomes are still being curtailed; those conditions will cause consumer spending to lag. Some businesses, of course, are not going to open quickly or fully. Restaurants and movie theaters are two clear cases. But don't write the consumer off.

Business spending for a while will be ramped up to create a safer workplace. There will be plastic screens installed and barriers to create space from customers and lots of sanitization work. All of that will be to enhance safety for workers and consumers and will not add to productivity. Firms are heading out to find a new normal. As for conventional investment, that is really off the books for a while as GDP is knocked below trend and it will lag behind for a number of quarters. There is no need for much capital spending beyond the world I just described to create safer conditions.

One question is how much the virus will impact peoples' desires to live and work in high density areas. Much of Europe is high density. In the U.S., there is more of a suburb-city tradeoff that occurs. But there could be some post virus impact on housing and housing investment.

Summing up

On balance, European GDP has been hit hard and U.S. GDP is getting hit hard. China appears to be farther along in a work-out phase. But international trade is still going to be slow to come back on line. Oil demand has been weak and will probably continue to lag. U.S.-China tensions are back in the news as U.S. President Donald Trump is angry at China over the spreading the virus and the way it handled informing the world. The U.S. has just taken an aggressive action against Huawei. The EU is seeking a fair scientific inquiry into how the virus was started. Australia has been pushing for that as well and has gotten the wrath of China in return along with reduced Chinese purchases of Australian foodstuffs. The fallout from the virus is not over and will now take many different forms. There could even be a relapse- a second wave. We are not going to have recession and then normal recovery. This is an abnormal essentially manmade recession, but now ‘man' has lost control of the recovery process. While there are some artificial actions that can be taken to speed recovery, for the most part recovery will be up to getting back to normal – whatever ‘normal' is now going to mean. And all that is still subject to the idea that the virus does not get loose again.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief