Global| Feb 08 2018

Global| Feb 08 2018French Survey Hits an Air Pocket

Summary

The Bank of France uses its survey to sort out its expectations for growth in the current quarter. At a level of 104.7 in January, the BoF business survey index is at its weakest level since June 2017. The BoF now thinks that this [...]

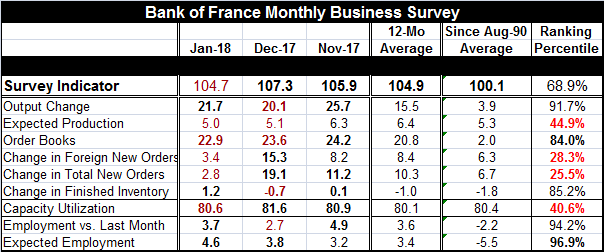

The Bank of France uses its survey to sort out its expectations for growth in the current quarter. At a level of 104.7 in January, the BoF business survey index is at its weakest level since June 2017. The BoF now thinks that this implies that the economy is set to grow at a slower pace in the first quarter of 2018. Gross domestic product is expected to climb 0.4% in the first quarter, slower than the 0.6% increase seen in the fourth quarter of 2017.

The Bank of France uses its survey to sort out its expectations for growth in the current quarter. At a level of 104.7 in January, the BoF business survey index is at its weakest level since June 2017. The BoF now thinks that this implies that the economy is set to grow at a slower pace in the first quarter of 2018. Gross domestic product is expected to climb 0.4% in the first quarter, slower than the 0.6% increase seen in the fourth quarter of 2017.

Indeed, French retail sales already are on a weakening trend with volumes off at a 13.8% pace over three months (as of December) and lower by 0.3% year-on-year. While Germany continues to run out stellar numbers, the French economy is beginning to turn up some weak spots.

The BoF business survey itself showed strength in output changes in January. That indicator rose to 21.7 from 20.1 and is well above its 12-month average of 15.5. It stands in the 91st percentile among its historic queue of data back to 1991. Output is still in very good shape. But while the current indicators in this report are still in good shape, some of the future barometers show evidence of more troubles.

Expected production is not so robust. That reading slipped to 5.0 in January from 5.1 in December and holds only a 44th percentile standing; thus, leaving it below its historic median (which occurs at a percentile value of 50). The January reading is also below its 12-month average of 6.4.

Order books overall slipped in January to a 22.9 reading from December's 23.6. The January level is below its 12-month average although it is still quite solid with an 84th percentile historic standing.

However, foreign orders and new orders both have dropped sharply in January compared to December levels. This is in marked contrast to Germany where orders data up-to-date through December show roaring foreign orders although in Germany domestic orders are lower on balance over 12 months. But for France, in each case, for new orders and for foreign orders, it is a drop of double-digit proportions month-to-month. Both measures also are significantly below their 12-month averages. And both of them also have historic queue standings below their respective 30th percentiles, marking them as quite weak.

The capacity use measure has slipped month-to-month, but it is still above its 12-month average although with a queue standing at 40.6%, below its historic median. France should not be experiencing price pressures from capacity usage.

In the end, the French economy is still a creature of its times. Like the U.S. and so many other economies, it shows some of its best relative strength in its labor market. Its employment reading for last month as well as for expected employment ahead, both improve month-on-month and both stand above their respective 12-month averages. Both have rank standings around their respective 95th percentiles, marking these as very strong readings.

There has not been any hint of weakness in France from the monthly PMI readings where both manufacturing and service sector readings have been strong and on rising trends. However, retail sales have not been especially strong for a while. Add to that vulnerability in new orders and foreign orders and a prescription for weakening in the French economy is complete. These are trends we will want to keep an eye on. France is the second largest economy in the euro area and its growth matters.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief