Global| Apr 16 2018

Global| Apr 16 2018French Sales Step Up; But for How Long?

Summary

The series for French retail sales is volatile and hard to pin down. Nonetheless, consumer spending is having an upswing with three-month sales volume up at a 15% annual rate. Over three months, all retail components are rising. Five [...]

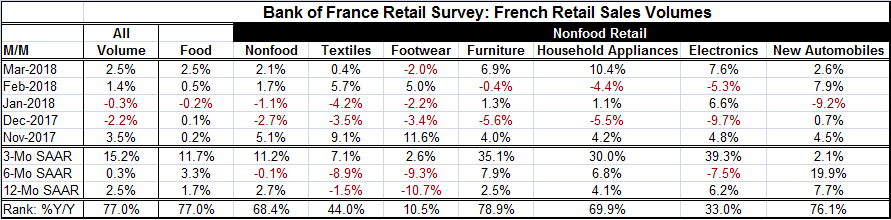

The series for French retail sales is volatile and hard to pin down. Nonetheless, consumer spending is having an upswing with three-month sales volume up at a 15% annual rate. Over three months, all retail components are rising. Five of eight components have double-digit annualized growth rates over the most recent three months. The slowest three-month gains are for new auto sales and footwear.

The series for French retail sales is volatile and hard to pin down. Nonetheless, consumer spending is having an upswing with three-month sales volume up at a 15% annual rate. Over three months, all retail components are rising. Five of eight components have double-digit annualized growth rates over the most recent three months. The slowest three-month gains are for new auto sales and footwear.

Despite the size of some of the three-month growth rates, the current ‘surge’ in growth has not impacted the year-on-year growth rates in an impressive fashion, but it obviously has helped to elevate them.

At the bottom of the table, we rank the year-on-year growth rates from November 2000. On that timeline, overall sales volume growth ranks in the 77th percentile among all annual growth rates for the period. The overall pace has the same ranking as for food, furniture, and new autos with the nonfood aggregate and household appliance spending ranking a bit lower and other components ranking much lower. The year-over-year growth rates have not been boosted to show real strength by the three-month surge. But there is a three-month surge. The three-month value of growth has ranked as strong, or stronger than its current pace less than 3% of the time back to 2002. French sales are really having a revival. Why?

The real question for France is whether this sales revival will be long lived. It is likely that this burst in sales is temporary as spending ramped up ahead of the nationwide strikes that now are in progress. French President Emmanuel Macron is under pressure for his unpopular reforms that are aimed to make France more competitive by making labor markets more flexible. French workers are known for being especially obstreperous in protesting changes in work rules and other regulations. French farmers are downright militant.

The French police currently are encountering physical protests in the French Southern city of Montpellier that has seen clashes with the police and 52 people arrested.

While the people are protesting, most experts have pointed out that labor unions have not orchestrated widespread resistance and that probably indicates that the reforms still do not go far enough. François Hollande, President before Macron, had a round of labor market reforms implemented that he had to all but rescind.

“All nine of France’s main unions united for the strike action, the first time this has happened in a decade. However, only 209,000 of the eligible 5.4 million union members participated in the latest countrywide strike, the fourth such demonstration since Macron took office" (Source here).

Macron’s 36 measures of labor market reform have just been implemented. One of these reforms limits payment to laid a laid off employees who worked at a firm for 30 years or more to 20 months of salary. For five key reform points, see here.

The ongoing strikes and resistance are like to interfere with consumer spending in the coming weeks and perhaps beyond. Not only does striking and other antisocial behavior take time away from engaging in economic commerce, there may be a secondary impact on spending if workers are made to feel less safe or less protected by the labor market reform itself. For example, consumers’ savings rates could rise. Finally, there will be a third kind of impact if firms really take advantage of the new ways to realign operations and let workers go.

So far, the impact on spending is positive. But it would be surprising if this surge were the vanguard of a new burst in spending. Not only is there the impact of the adoption of the labor laws and the reform of the railway system to consider, but also the fact that growth has been slowing in France after a long period of recovery. The French manufacturing and service sector PMI gauges from Markit have been showing some backtracking for several months.

This surge in French spending is welcome. But it is likely not to be lasting and it is even less likely to be the cutting edge of a pick-up in growth. It may be a bit more like a last hurrah.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief