Global| Aug 27 2019

Global| Aug 27 2019French Manufacturing Improves While Services Run Flat

Summary

A one-month bounce amid trend confusion The French industry climate gauge for manufacturing may have bounced higher in August, but there is no sense in which climate is turning the corner and improving. It’s just a monthly wiggle that [...]

A one-month bounce amid trend confusion

A one-month bounce amid trend confusion

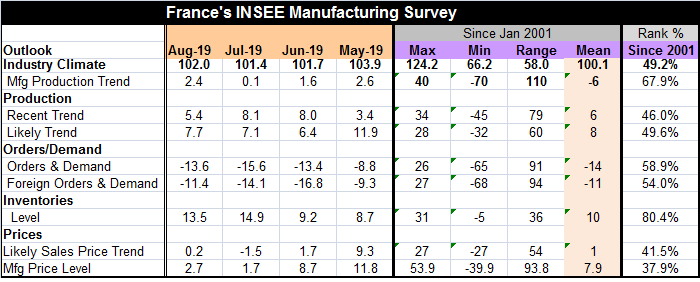

The French industry climate gauge for manufacturing may have bounced higher in August, but there is no sense in which climate is turning the corner and improving. It’s just a monthly wiggle that shows improved industrial climate compared to July, little change since June, and a level still below May as well as below all months of 2018 and all months back to December 2016.

On data since 2001, the current climate gauge is still below its period median although it is above its mean.

Production expectations picked up in August and are at their strongest since May and with a 67.9 percentile standing- in the top one third of its historic range of values. So there is some production optimism in France despite the negative environment, weakness in Germany and the expectation of ECB stimulus.

The recent trend for production shifted lower and has a 46th percentile standing. The likely trend has improved for two months running but also has a below median 49.6 percentile standing.

Orders and demand have a chronic negative sign (even the mean!). The recent responses are simply waffling at a 58.9 percentile standing. Meanwhile, foreign orders and demand (also with a negative mean) have improved slightly and have a 54th percentile standing. The rankings for the total and foreign series on orders and demand are highly similar and decidedly moderate.

French inventory readings are lower month-to-month but have more generally crept up. Their percentile standing is relatively high at an 80th percentile mark. With moderate sales and orders growth, this seems to be a bit of a warning sign of excess inventories.

Price expectations are a bit firmer month-to-month but clearly have ebbed on trend. The standing for the likely sales price trend is below its median at a 41.5 percentile standing; the level of manufacturing prices has a 37.9 percentile standing, similarly weak.

Manufacturing and services trends

The services reading has behaved similar to the manufacturing sector in terms of its shifts, but its moves have been much more muted (See Chart above). Both sectors peaked early in 2018 then slid, ending that slide in late-2018 and now the mini-revival appears to be running out of gas. What happens next is still a matter of speculation since the mini-trend is now too hard to evaluate because of its brevity as well as its unevenness. Both manufacturing and services are well off their 2018 peak, but it is still hard to tell from the trend what is next.

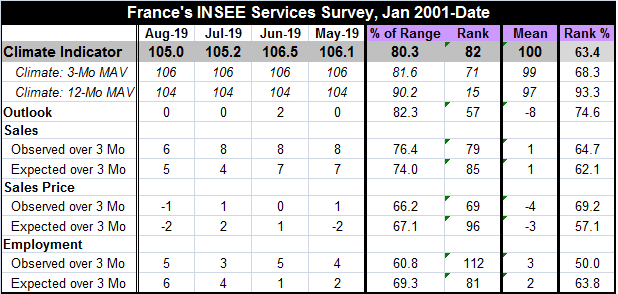

Service sector details

Services have been flatter overall in comparison with manufacturing. The climate indicator has barely slipped month-to-month and has weakened for two months running. The climate indicator averages 104 over 12 months, 106 over three months and is at 105 currently, underscoring the point about the ambivalent trend. The climate indicator’s 12-month average has a huge 93.3 percentile standing, while the three-month gauge (which is higher!) has only a 68.3 percentile gauge. The August climate gauge standing is at 63.4 in percentile terms.

The outlook has been at zero in three of the last four months; that is actually a good reading for France with a 74.6 percentile standing.

Both expected and observed sales trends for services have weakened. Observed sales have a 64.7 percentile standing and expected sales have a slightly weaker 62.1 percentile standing. The readings are quite close in standing and at moderate levels.

Sales prices observed and expected both turned negative in August. Observed prices have a 69th percentile standing while expected prices have a weaker 57th percentile standing. Despite negative diffusion values, the standings are moderate and not consistent with deflation.

Employment readings for observed and expected conditions have strengthened slightly recently. The observed trend has a 50th percentile standing. The expected trend has a 63.8 percentile standing.

Sum up

The French readings for manufacturing and services are all about moderation. Manufacturing has a little more outright weakness while the services gauges are more decidedly with moderate readings and above median standings.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief