Global| Apr 28 2015

Global| Apr 28 2015French Household Sector Confidence Rises Further

Summary

French household confidence has increased in seven of the last nine months and has gone nine months without a setback to confidence. However, the confidence reading is still weak historically. At 94 the current confidence reading is [...]

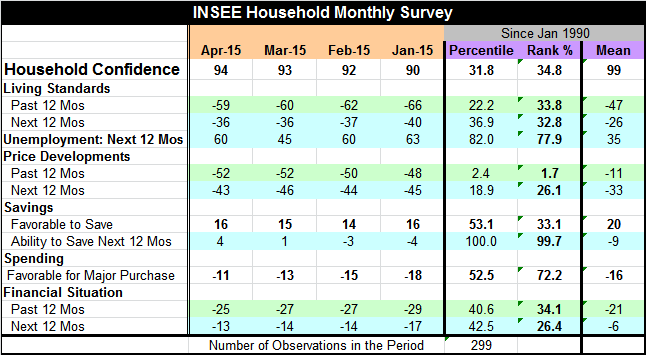

French household confidence has increased in seven of the last nine months and has gone nine months without a setback to confidence. However, the confidence reading is still weak historically. At 94 the current confidence reading is below its average of 99 since 1990 and over that period it stands only in the 34th percentile of its historic queue of data. Confidence in France is better than this about 66% of the time.

French household confidence has increased in seven of the last nine months and has gone nine months without a setback to confidence. However, the confidence reading is still weak historically. At 94 the current confidence reading is below its average of 99 since 1990 and over that period it stands only in the 34th percentile of its historic queue of data. Confidence in France is better than this about 66% of the time.

Households' assessments of living standards over the past 12 months have been experiencing ongoing improvement this year. Looking ahead, over the next 12 months, improvement into the future has been expected to continue. Still, both the past and the next 12-month outlooks stand in the lower one-third of their respective historic queue of values.

Just today the number unemployment in France was announced to have reached a record high in March, with number unemployed up by 0.4% from its February level. Still, the April household confidence report shows the probability of unemployment still at its February level and below its January level. Expected unemployed over the next 12 months is much higher than its March reading, but that March drop now appears to be a fluke. Expected unemployment is still high at a reading of 60 this month, well above its historic average of 35 and it is high as illustrated by its 77th percentile queue standing (higher only 23% of the time). Both the household survey data and the official unemployment data show that unemployment in France remains a problem.

The assessment of price developments shows that deflation has been rather intensely and consistently experienced over the last 12 months. The current reading on past inflation has been lower historically only 1.7% of the time. Looking ahead, readings for expected prices are still weak but more stable at a higher 26th percentile standing.

The environment for spending has improved for four consecutive months. Consumers' assessment of this environment has been better only about 28% of the time. This is the truly `strong reading' of this report.

The household financial situation as seen over the past 12 months and as expected over the next 12 months has improved in each measure over the past three months. Both measures are on their cycle highs. Each of these measures was last higher in November 2010 for one brief month. But the past financial situation was last consistently better prior to February 2010 and the expected financial situation was last consistently better than this before April 2010. Still, these standings remain depressed. The past financial situation stands in its 34th percentile. The situation for the next 12 months stands in its 26th percentile

As shown in the chart, the consumer sector has been on an upswing that is stronger than the rise of the business sector. But the business sector's percentile standing is still higher, standing in its 57th percentile, compared to the household sector in its 34th percentile. France's recovery clearly still has a long way to go. It still one of the weaker euro area economies. France is currently trying to reduce its government deficit as a percent of GDP to EMU requirements so there is no scope for fiscal stimulus. France's manufacturing data tell us that its foreign orders are slightly stronger than its overall orders, an indication that the weak euro may be providing some stimulus for French manufacturing. France's future may be on a rise that can have some legs.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief