Global| Aug 26 2020

Global| Aug 26 2020French Household Confidence Waffles at a Weak Level

Summary

French household confidence ticked higher in August to stand at 94.5 compared to 94.1 in July. Confidence had previously risen to 96.3 in June, but it is still below that level. Confidence fluctuated in a range from 102 to 105 from [...]

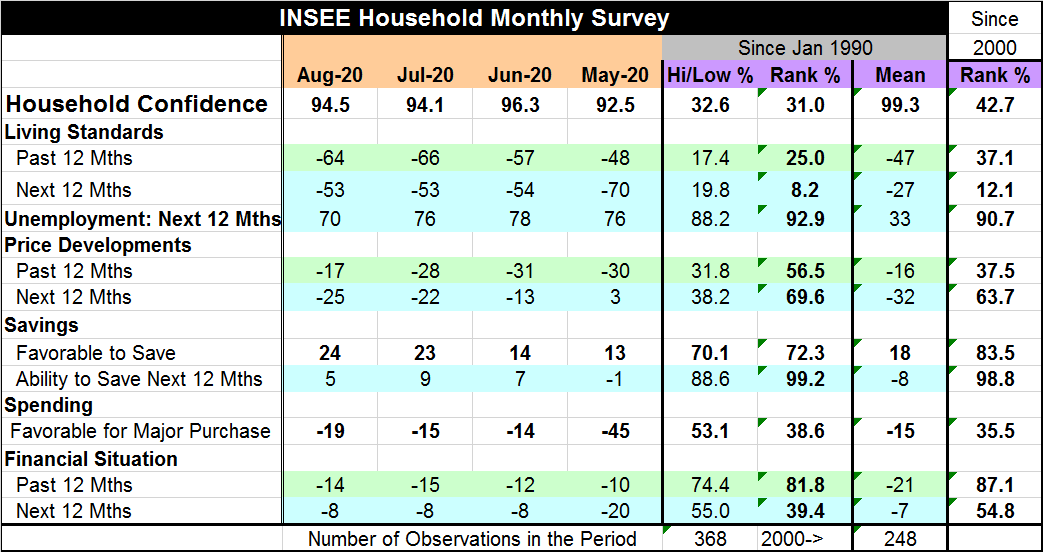

French household confidence ticked higher in August to stand at 94.5 compared to 94.1 in July. Confidence had previously risen to 96.3 in June, but it is still below that level. Confidence fluctuated in a range from 102 to 105 from August 2019 to March 2020. Then the virus hit and took that reading down to 95 in April and to 92.5 in May. The graph shows these as weak levels but not nearly as weak as those reached in the Great Recession and with other readings in early-2019 as well as many in the early post-recession period that had been lower. Still, household confidence has taken a hit. When ranked against its historic collection of values back to 2000, the current reading has a 42.7 percentile standing putting it below its median (the median reading occurs at a rank of 50% for any ranked series).

French household confidence ticked higher in August to stand at 94.5 compared to 94.1 in July. Confidence had previously risen to 96.3 in June, but it is still below that level. Confidence fluctuated in a range from 102 to 105 from August 2019 to March 2020. Then the virus hit and took that reading down to 95 in April and to 92.5 in May. The graph shows these as weak levels but not nearly as weak as those reached in the Great Recession and with other readings in early-2019 as well as many in the early post-recession period that had been lower. Still, household confidence has taken a hit. When ranked against its historic collection of values back to 2000, the current reading has a 42.7 percentile standing putting it below its median (the median reading occurs at a rank of 50% for any ranked series).

As is always the case these days, the virulence and progression of the virus drives French policy and that policy in turn either relaxes its grip on the economy or constricts it. France is currently in a re-tightened policy grip since the virus has been spreading again.

France reported 3,304 more cases on Tuesday, raising its overall count to 248,158. The death toll increased by 22 and stands at 30,513, while 4,600 patients remain in hospital, 410 of them in intensive care, according to the Health Ministry's latest figures. Most of France's larger cities have now reinforced safety measures in place since the start of the pandemic, particularly the wearing of masks (Source here).The assessments of living standards for the next 12 months have been essentially unchanged in this survey for the last three months. There was an abrupt move up from the May level that has had no follow though. As of August, the expectations for living stands had a 12.1 percentile standing that compares to a 37.1 percentile standing for the same measure looking backward 12 months. Clearly living standard expectations have ratcheted lower.

Despite the ongoing virus issues this month, unemployment expectations took a sizeable step lower. They had been essentially unchanged over the previous three months back to May. Still, unemployment expectations are high with a standing that has been higher less than 10% of the time.

Expected price developments have changed markedly as the virus hit and time passed. In May expected prices 12 months ahead had a positive value of 3. That eroded to -13 in June and to -22 in July and now to -25 in August. Expected price developments now have a 63.7 percentile standing which is an above their median standing and above the 37.5 percentile standing for price developments assessed looking back at the past 12 months; but the August reading also represents a sharp lessening of price expectations compared to May and expectations may still be in the process of deflating.

In May the environment for spending ‘improved' to -45 from a -60 reading in April as the virus rocked the economy in full force causing massive dislocations. Since then, the spending environment has improved but it did all of that in the month of June. Conditions then deteriorated a bit in July and eroded again in August so that the spending environment now has a 35.5 percentile ranking. If that does not improve, it is not going to drive much growth. Government may force-feed people income, but unless people have confidence in the future that income will not be as substantially spent and its impact on growth will diminish.

The financial situation for 12 months ahead, as perceived by those surveyed, made a sharp improvement in June and has stayed at that level for three months in a row. That level puts the assessment of the financial situation at a ranking in its 54.8 percentile which is a few points above its historic median. However, the backward assessment for how things ‘were' over the previous 12 months finds an assessment in its 87th percentile- quite a bit higher. A few pips above the median is hardly the same assessment as the top 13th percentile.

On balance, France has been hit hard by the virus. It has taken down peoples' perceptions and expectations for important economic conditions across the board. Expectations for the 12 months ahead are still quite adversely impacted and this is with government policy firing on all cylinders desperately trying to keep the economy together and to make people whole in the face of this public health calamity. And this statement is a general one, not simply applicable to France. The French survey, however, is a frightening indictment of how far short of normalcy even the most supportive government policies fall. It is very hard – seemingly impossible- for government to replicate the conditions and drive expectations the same as those created by a well-functioning private economy – even one with all the government intervention and intrusions found in France.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief