Global| Jan 29 2016

Global| Jan 29 2016French GDP in Q4 Gains at 1% Pace

Summary

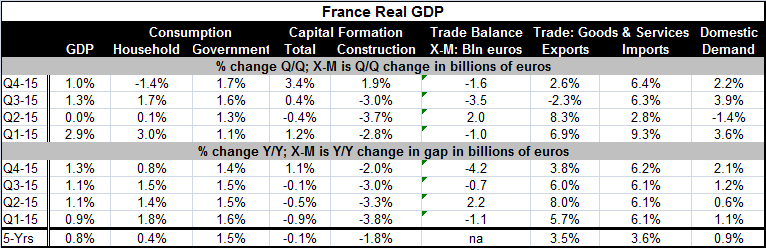

The year-over-year growth in GDP has been gaining for France (as the chart shows), but on that same basis, household consumption has begun to pull back. On a quarterly basis, France GDP slowed to a 1% pace from 1.3% in Q3. France ends [...]

The year-over-year growth in GDP has been gaining for France (as the chart shows), but on that same basis, household consumption has begun to pull back.

The year-over-year growth in GDP has been gaining for France (as the chart shows), but on that same basis, household consumption has begun to pull back.

On a quarterly basis, France GDP slowed to a 1% pace from 1.3% in Q3. France ends the year with GDP up 1.3% on a Q4-to-Q4 basis, its best yearly gain since 2011.

French household spending fell by 1.4% in Q4 annualized and gained only 0.8% Q4 over Q4. Still, that gain was stronger than its 0.5% gain Q4/Q4 last year. Household spending growth has only averaged a 0.4% year-over-year going back over the past five years.

French government spending rose by 1.7% annualized in Q4, up from a 1.6% pace in Q3. Government spending rose Q4-over-Q4 by 1.4% in 2015, just a tick below its five-year average rise.

Total capital spending surged at a 3.4% annualized rate in Q4, pulling the yearly gain up to 1.1% (Q4/Q4) after three previous quarters of investment declines. Construction spending in particular posted a rise in Q4 at 1.9% but fell by 2% Q4/Q4 in 2015.

The international deficit for France shrank in Q4 compared to Q3, but it widened sharply by 4.2 billion euros over the last four quarters. This widening is the result of export growth trailing import growth in Q4 as well as over the last four quarters. Export growth picked up to 2.6% after contracting in Q3. But imports grew at a steady 6.3%-6.4% pace in both Q3 and Q4. The Q4-over-Q4 import growth was 6.2% in 2015 compared to exports at 3.8%. French imports simply are consistently outpacing exports. However, more broadly, over the last five years, export and import growth have been nearly identical.

France shows that it is still making GDP gains, but the gains are not impressive and have relied heavily on the government sector. Consumption has lagged and the growing trade deficit speaks of a loss in competitiveness even though the euro exchange rate has continued to hover at a low level. There is the issue of competitiveness and trade within the EMU community where exchange rates are not an issue.

Euro Area News

Apart for France, euro area member Spain recorded Q4 GDP growth for today too. Spain posted a raw Q4 gain of 0.8%, the same as in Q3 but notched a pace of 3.5% for the year as a whole. Spain also oddly reported a drop in its inflation rate for January to below zero and now has to worry about deflation again.

Economic news for the euro area was mixed as the eurocoin index rose to 0.48 and posted a 4.5-year high. Inflation accelerated for the EMU as a whole despite Spain's problem with deflation. The ECB reported that money and credit each slowed in December. Germany reported that its retail sales fell in December.

Asia Showed Weak Numbers and a Surprise Policy Move

Japan surprised everyone as the Bank of Japan adopted negative interest rates in its meeting overnight. Taiwan recorded its second quarterly drop in GDP in a row prompting the assessment for recession there. Japan's data remain soft as Japanese industrial production fell sharply by 1.4% in December and household spending for the year posted a decline.

Summing Up

By comparison, the French GDP report was breath of fresh air. Problems in China clearly are `dragging down the neighborhood' in Asia. Taiwan is a clear knock-on effect from China. Japan continues to struggle with contracting demographics. Its move to install negative interest rates by the BOJ was shocker, totally unexpected. But the financial markets in China were finally up on the day and European markets were reacting nicely to Japan's news of negative rates. Economic conditions remain touch and go, but for a day at least, the last trading day in January, markets seem to want to right themselves.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief