Global| Sep 26 2008

Global| Sep 26 2008French Consumer Sentiment Makes a Small Bounce

Summary

The small rise in French consumer sentiment comes as Q2 GDP is revised to show a larger drop amid weakness across other Euro Area countries. The rise in sentiment is somewhat like the improvement in US consumer sentiment in September. [...]

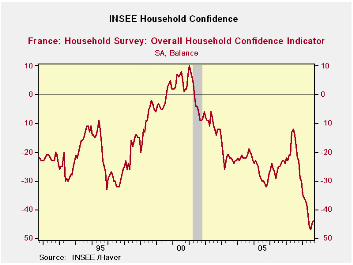

The small rise in French consumer sentiment comes as Q2 GDP is revised to show a larger drop amid weakness across other Euro Area countries. The rise in sentiment is somewhat like the improvement in US consumer sentiment in September. Energy prices moved lower for a spell and consumers usually react strongly to changes in energy prices. But energy costs have since moved higher. The overall French index stand in the lower five percent of its historic range. Survey respondents say over the past 12 months their living standards were in the bottom 2% compared to historic responses. For the next 12 months they expect an improvement with responses that are in the bottom 10 percentile of their historic range.

The spending environment is not very favorable for major purchases with a rating only in the lower 8 percent of its historic range or a ranking that is 221st out of a possible 225.

Putting range percentiles aside over this period there are 225 months of observations. Seven of the key measures rank 221 or worse. That is by ranking the readings we find they reside in the bottom two percent among all observations (see table to identify those categories).

The bounce in the French household confidence reading is not significant. It will have to show it can weather more storms ahead instead of just react well when global oil prices fall.

| INSEE Household Monthly Survey | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Since Jan 1990 | Since Jan 1990 | |||||||||

| Sep 08 |

Aug 08 |

Ju 08 |

Jun 08 |

%tile | Rank | Max | Min | Range | Mean | |

| Household Confidence | -44 | -45 | -47 | -46 | 5.3 | 222 | 10 | -47 | 57 | -18 |

| Living Standards | ||||||||||

| past 12 Mos | -80 | -80 | -82 | -78 | 2.0 | 223 | 18 | -82 | 100 | -38 |

| Next 12-Mos | -51 | -54 | -59 | -57 | 10.8 | 222 | 15 | -59 | 74 | -19 |

| Unemployment: Next 12 | 51 | 43 | 36 | 21 | 80.0 | 60 | 73 | -37 | 110 | 29 |

| Price Developments | ||||||||||

| Past 12Mo | 44 | 54 | 61 | 63 | 83.5 | 7 | 64 | -57 | 121 | -16 |

| Next 12-Mos | -54 | -42 | -30 | -29 | 6.6 | 223 | 31 | -60 | 91 | -34 |

| Savings | ||||||||||

| Favorable to save | 17 | 18 | 18 | 20 | 36.1 | 173 | 40 | 4 | 36 | 23 |

| Ability to save Next 12 | -16 | -18 | -20 | -21 | 24.1 | 198 | 6 | -23 | 29 | -9 |

| Spending | ||||||||||

| Favorable for major purchase | -37 | -38 | -38 | -37 | 8.6 | 221 | 16 | -42 | 58 | -13 |

| Financial Situation | ||||||||||

| Current | 8 | 7 | 7 | 8 | 23.8 | 172 | 24 | 3 | 21 | 12 |

| Past 12 MOs | -34 | -35 | -36 | -34 | 6.5 | 222 | -5 | -36 | 31 | -17 |

| Next 12-Mos | -18 | -20 | -21 | -23 | 14.7 | 221 | 11 | -23 | 34 | -1 |

| Number of observations in the period: 225 | ||||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief