Global| Sep 26 2017

Global| Sep 26 2017French Biz Climate Edges Lower Stays High-Valued

Summary

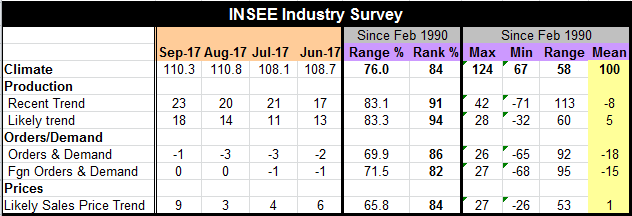

French business climate edged lower in September but is still a very high-valued reading. At 100.3 it is down from 110.8 in August but the standing is still at its 84th percentile, higher historically only 16% of the time. The recent [...]

The Report's Inflation Diagnostic Starts to Read Hotter

French business climate edged lower in September but is still a very high-valued reading. At 100.3 it is down from 110.8 in August but the standing is still at its 84th percentile, higher historically only 16% of the time. The recent and likely trend ratings both expanded and have standings in the 90th percentile of their respective ranges. The past and current trend growth assessments in France continue to be strongly evaluated.

French business climate edged lower in September but is still a very high-valued reading. At 100.3 it is down from 110.8 in August but the standing is still at its 84th percentile, higher historically only 16% of the time. The recent and likely trend ratings both expanded and have standings in the 90th percentile of their respective ranges. The past and current trend growth assessments in France continue to be strongly evaluated.

The French orders and foreign orders series have much lower diffusion values than other components but when ranked against their historic standings they still stand up as relatively strong levels. Orders and demand have an 86 percentile standing despite a raw diffusion score of -1. Foreign orders and demand with a zero net diffusion score have an 82nd percentile queue standing. While both of these readings are weak in diffusion terms they are still among the stronger readings French industry has seen since 1990.

The likely sales prices trend reading made a significant move higher to +9 in September from +3 in August. That reading is a top 16 percentile queue standing reading. The outlook for prices was last greater than this value in July of 2011- over six years ago.

The plot of the climate index shows that there have been eight episodes since 1980 when the Climate index has gotten to be this high of higher. In three of the past cycles the index peaked out at readings close to the level the index is now posting.

One surprising development in this poll is the higher inflation reading. Oil prices remain relatively well contained. And the Euro-Area as been seeing the exchange rate start to buck-up to higher level as the ECB has been flirting with a less accommodative policy. A stronger euro is more likely to depress prices yet in France expectations for prices are firming and at an 84th percentile standing the current reading is already reasonably high. And the monthly jump in the prices series make it one of the largest month to month changes in the likely prices trend series in its history, a top 10% reading. Apparently there are some price pressure in the French manufacturing sector that are unique to it since we are not seeing these in the EU data or even reported yet in France's HICP (which is not updated though September yet). The French Insee series puts us on the outlook for inflation pressures in France.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief