Global| Dec 11 2015

Global| Dec 11 2015France's Current Account Swings Back to Deficit

Summary

France's current account surplus proved to be short-lived. A smattering of monthly surpluses has given way to deficits again. The current account averages deficits over 12 months, six months and three months. French export growth [...]

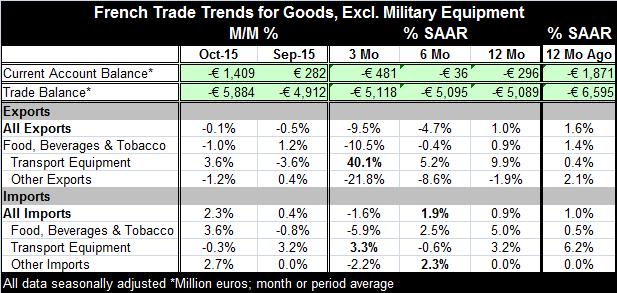

France's current account surplus proved to be short-lived. A smattering of monthly surpluses has given way to deficits again. The current account averages deficits over 12 months, six months and three months.

France's current account surplus proved to be short-lived. A smattering of monthly surpluses has given way to deficits again. The current account averages deficits over 12 months, six months and three months.

French export growth peaked early in the year but has since lost its zest and exports are backsliding. Export growth currently logs a gain of 1% over 12 months. Exports are falling at a 4.7% pace over six months and at a faster 9.5% annual rate over three months. The thrill is gone. Whatever fundamentals were supporting the rebound in French exports, they are gone too.

Exports of food and other items are decelerating and contracting at a horrific pace over three months. The single strong category that staves off some of this weakness in total exports is transportation equipment where shipments are up at a 40.1 annualized rate over three months. The auto sector has been the one resilient sector for all of Europe as well as in the U.S. France is no exception to this exception.

French import trends are not as easily pigeon-holed. Overall imports are up by just 0.9% over 12 months, just a hair slower than exports. Import trends are erratic across timelines with six-month growth at a 1.9% pace and three-month growth at a -1.6% pace.

Import categories have somewhat mixed trends. Two of three categories show a drop off in growth from 12-month to six-month with `other imports' as the exception. Then, over three months, imports fall in all categories except transportation equipment. Both transportation equipment and good imports are higher year-over-year, but other imports are flat.

The overall lethargy in French imports speaks to the weakness of domestic demand in France. While the euro has regained a slight amount of strength recently, it is still weak and should be helping to boost French exports and should help to stave off imports. The euro may be helping to keep imports in check, but there is no boost to speak of for exports.

France's economy has been showing some signs of picking up as its manufacturing PMI has drifted above 50 and its services PMI has held above 51. But while these are positive readings, they still aren't strong and we see little evidence of strength in either French imports or exports. In that respect, this trade and current account report seems to be evidence of more that same-old, same-old in France. The economy is neither contracting nor accelerating. It's as though it is caught in some no-where zone of stunted growth and can't get out.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief