Global| Sep 21 2009

Global| Sep 21 2009Forecasters Expect Return Of Positive GDP Growth This Quarter, Slow Thereafter

by:Tom Moeller

|in:Economy in Brief

Summary

Each quarter, the Federal Reserve Bank of Philadelphia surveys a group of professional forecasters to gain perspective on the outlook for the U.S. economy. In the August survey, the panel expected the recession to have reached its [...]

Each

quarter, the Federal Reserve Bank of Philadelphia surveys a group of

professional forecasters to gain perspective on the outlook for the

U.S. economy. In the August survey, the panel expected the recession to

have reached its end, though the recovery is expected to be subpar.

That subpar nature is expected to keep unemployment high but it is not

expected to prevent inflation and interest rates from rising.

Each

quarter, the Federal Reserve Bank of Philadelphia surveys a group of

professional forecasters to gain perspective on the outlook for the

U.S. economy. In the August survey, the panel expected the recession to

have reached its end, though the recovery is expected to be subpar.

That subpar nature is expected to keep unemployment high but it is not

expected to prevent inflation and interest rates from rising.

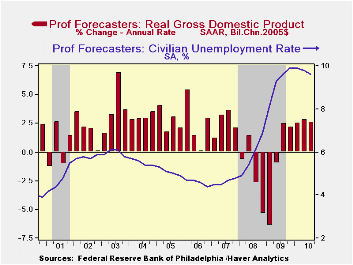

Just 2.4% growth in real GDP is expected during the current quarter to be followed by growth at about that rate into next year. That follows the 3.9% y/y drop in real GDP through last quarter, which was the deepest decline since the Great Depression. Indeed, this recovery is subpar compared to prior periods of severe recession. Following the 1973-75 recession, when GDP fell at a peak y/y rate of 2.3%, growth shortly rebounded to 6.2%. Similarly following the 1981-82 recession, when GDP fell 2.7% y/y, a snapback came quickly at near an 8% rate.

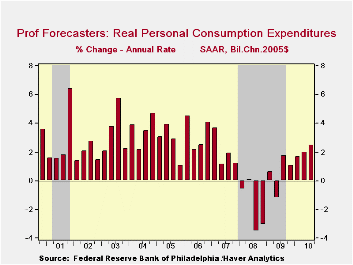

The subpar nature of the coming economic

recovery stems very much from the consumer who remains burdened by

excessive levels of debt.

A swing towards inventory accumulation also should play a part in the pending economic recovery, yet here again it's not a huge part. Accumulation at near a $20 billion annual rate is expected by the end of next year. Certainly that is improved from the peak rate of decumulation of $141 last quarter, and the dollar swing is impressive. But as a percentage of the economy's overall real size it amounts to barely half the swing after prior severe recessions. As for the foreign trade deficit, recent improvement has helped forestall an even deeper decline in U.S. GDP during this recession. However, that improvement is expected to now end with little or no improvement through next year as foreign economies remain weak.

Weak

economic growth is expected to do little reduce unemployment. The

unemployment rate is expected to average 9.9% and then dip just to 9.6%

by next year's third quarter.  These rates are the highest jobless rates

since 1982-83 and reflect little or no growth in expected employment.

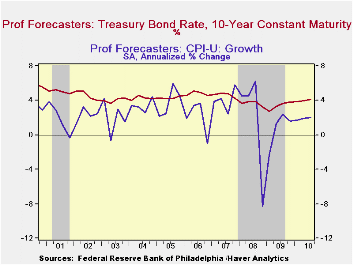

Pricing power is thus expected to be severely constrained. The y/y

growth in the overall GDP price deflator is expected to drift up to

1.5% from its low of 1.0% this year. Perhaps not-so-surprisingly,

forecasters expect that lift to stem from a liquidity-driven rise in

core consumer prices to 1.6% from a low of 1.1% being reached now.

Ten-year Treasury yields are expected to rise in tandem to highs near

4% by the middle of next year.

These rates are the highest jobless rates

since 1982-83 and reflect little or no growth in expected employment.

Pricing power is thus expected to be severely constrained. The y/y

growth in the overall GDP price deflator is expected to drift up to

1.5% from its low of 1.0% this year. Perhaps not-so-surprisingly,

forecasters expect that lift to stem from a liquidity-driven rise in

core consumer prices to 1.6% from a low of 1.1% being reached now.

Ten-year Treasury yields are expected to rise in tandem to highs near

4% by the middle of next year.

The full Third Quarter 2009 Survey of Professional Forecasters from the Federal Reserve Bank of Philadelphia is available here

. The data are available in Haver's SURVEYS database.| FRB Philadelphia Survey of Professional Forecasters (AR) | 2Q '09 | 3Q '09 | 4Q '09 | 1Q '10 | 2Q '10 |

|---|---|---|---|---|---|

| Real GDP | -1.0% | 2.4% | 2.2% | 2.5% | 2.8% |

| PCE | -1.2 | 1.7 | 1.1 | 1.7 | 2.0 |

| Non-Residential Investment | -8.9 | -7.3 | -6.3 | 2.1 | 3.8 |

| Residential Investment | -29.3 | -7.3 | 1.8 | 5.6 | 13.4 |

| Federal Government | 10.9 | 6.2 | 4.1 | 1.5 | 2.1 |

| Change in Business Inventories | $-141.1B | $-89.9B | $-32.7B | $-1.7B | $9.5B |

| Net Exports | -339.3 | -340.0 | -342.1 | -353.6 | -366.0 |

| Unemployment Rate (%) | 9.3 | 9.6 | 9.9 | 9.9 | 9.8 |

| Consumer Price Index (Y/Y, %) | 2.4 | 1.7 | 1.1 | 1.5 | 1.5 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief