Global| Oct 20 2017

Global| Oct 20 2017Five-Month High for German PPI; Is Inflation or Trouble Brewing?

Summary

In the short run, oil prices drive a lot of the changes in Germany's PPI. Over the past three months, Brent prices have been steady rising and that has passed on an impact for rising prices to the PPI. While the German headline PPI is [...]

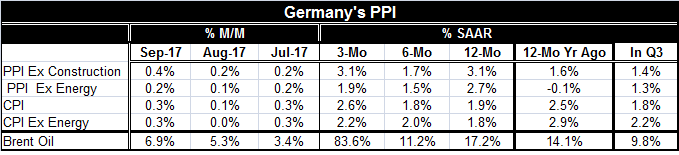

In the short run, oil prices drive a lot of the changes in Germany's PPI. Over the past three months, Brent prices have been steady rising and that has passed on an impact for rising prices to the PPI. While the German headline PPI is up by 0.4% in September, the core PPI is up by only 0.2%. But year-on-year, both are cranking at a pace near 3% with the headline gain at 3.1% and the core up at a 2.7% pace.

Consumer prices are the target

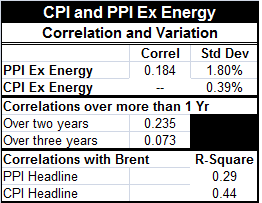

But what matters for policy is consumer prices. The European Central Bank makes policy based on the EMU-wide HICP (Harmonized Index of Consumer Prices) for the euro area. Germany's own core CPI bears a weak correlation to its own core PPI. The core of the CPI and the core of the PPI have a correlation of 0.18; over two years that correlation is 0.23, but over three years it drops sharply to 0.07. While the PPI is an import price index, it is not an enduring important determinate of the core CPI.

The PPI matters but the CPI matters more

As the chart (on the right) shows, the core PPI is much more volatile than the core CPI. The core PPI standard deviation is around 1.8 percentage points, compared to the core CPI which is around 0.4 percentage points. However, when we correlate the headlines of the PPI and CPI to Brent oil movements, it is the CPI with the higher correlation at 0.44 compared to the PPI at 0.29. Basically, the PPI does respond to oil and oil can have an important influence there, but the PPI has a lot of other influences as well. Meanwhile, the CPI is very trend dominated, but it does swerve in reaction of oil price changes and at those times the PPI also moves sharply. The bottom line is that higher oil prices are pushing the CPI up and may also have modest impact on raising the core. Still, these effects are transitory, not permanent.

The German CPI is on the brink

The German CPI is on its brink with the year-on-year headline at 1.9% and core at 1.8%. The Bundesbank -were it making monetary policy- would be aiming to get interest rates at least to their neutral position or higher since the German economy is so tight with a record-low post unification unemployment rate. But Germany also has a very solid fiscal position with its budget in balance. The rising euro exchange may help to keep inflation at bay in these circumstances. But at this moment in history, the Bundesbank is not making monetary policy. The ECB is making it and it is making it for all of the EMU. And inflation in the rest of the EMU is lower and economic performance is not as good as it is in Germany. Fiscal positions in the EMU are less-well consolidated than Germany's. Of course, the EMU area and Germany face identical exchange rate conditions. But even there, because of Germany's tight-fisted ways with inflation over the years, at current exchange rate levels Germany is more competitive than the EMU as a whole. So despite being the same exchange rate, it impacts Germany vs. the rest of the EMU asymmetrically.

Inflation: A parallax view

Because Germany literally sees inflation and its impact through a different lens than the rest of Europe, we can expect to hear more protestations from Germany about the need for higher rates and the desire to unwind existing stimulus programs. It is not so much that the German view is from a different perspective, although there is some truth in that, but that Germans will be obsessing over their own CPI while the ECB will be making policy from the broader EMU area HICP. Germany no longer has the option to use monetary policy to fight inflation even with its own inflation measures on the brink of excess. Germany basically gets whatever posture the ECB takes. And Mr. Draghi has been more concerned with the whole of Europe and the fact is that EMU-wide inflation is still not up to target (just below 2%). Germany has been on the verge of a policy dilemma for some time. Of course, with Angela Merkel having to engage in some exceptional coalition building, she no longer will have the free hand to do what she wants. It is not yet clear that anyone in Germany sees inflation there as threat enough to want to tighten an already buttoned down fiscal policy any more. But that is a possibility if inflation creeps over 2% (in Germany) and the ECB is not acting. And that is a real possibility. While traditionally what we see is lower inflation in Germany than elsewhere in the euro area, those tables have been turned in recent years. And now the ECB has an inflation target dilemma of another sort - inflation is undershooting in the EMU even as it threatens to overshoot in Germany. Nonetheless, Germany would like to see the ECB act by dismantling the special stimulus and lifting the interest rates back to neutral. But that approach does not seem to work for the rest of the EMU. This tension will be worth watching especially if European PMI indexes continue to do well as Germans are getting nervous about inflation. Their own country's level of inflation is not yet excessive, but it is on the brink. And if German inflation goes over 2% (on the CPI or HICP gauges), there will be even more discomfort in Germany and I'm sure it will pass that discomfort on to the ECB or to whoever is running it at the time.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief