Global| Oct 15 2018

Global| Oct 15 2018Finland's Inflation Stays Low -- Mostly

Summary

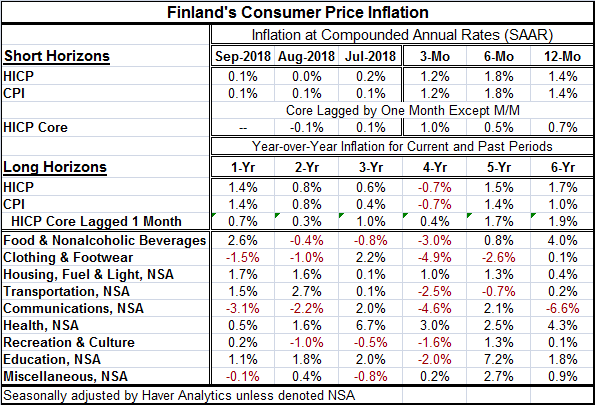

Finland is experiencing three distinct forces on the inflation front. Within the last year, inflation is low and stable. Yet, over the past year, inflation has been rising on a year-over-year basis (see Chart). However, at the same [...]

Finland is experiencing three distinct forces on the inflation front. Within the last year, inflation is low and stable. Yet, over the past year, inflation has been rising on a year-over-year basis (see Chart). However, at the same time core inflation over recent broad annual periods (as well as within the past year) has remained unaffected and is low and stable even in the face of rising oil prices and a rising headline inflation pace.

Finland is experiencing three distinct forces on the inflation front. Within the last year, inflation is low and stable. Yet, over the past year, inflation has been rising on a year-over-year basis (see Chart). However, at the same time core inflation over recent broad annual periods (as well as within the past year) has remained unaffected and is low and stable even in the face of rising oil prices and a rising headline inflation pace.

Finland's core inflation rate hit a low pace in 2015, barely north of zero then accelerated to reach a high barely above a 1% pace. It since has settled down to more sideways movement at a very moderate pace. The year-over-year core inflation rate, with its temperature taken last one month ago and then taken annually at 12-month intervals, has no reading higher than 1% over the last four years (see Table below).

Meanwhile, headline HICP and domestic CPI inflation are rising at a pace of 1.4% each over the last 12 months as of September. And both of these are at their relative five-year high pace (CPI is tied with its result of five years ago).

The message here remains that inflation is contained – well contained.

If we look at the HICP measure plotted vs. year-over-year percentage changes in oil prices, we see that oil explains a lot of the recent inflation acceleration and deceleration. Since 2015, Brent prices can ‘explain' about 85% in the year-over-year variability in Finland's HICP. Over the same period, Brent can ‘explain' only 0.01% of the variance in Finland's core HICP.

If we look at the HICP measure plotted vs. year-over-year percentage changes in oil prices, we see that oil explains a lot of the recent inflation acceleration and deceleration. Since 2015, Brent prices can ‘explain' about 85% in the year-over-year variability in Finland's HICP. Over the same period, Brent can ‘explain' only 0.01% of the variance in Finland's core HICP.

This phenomenon that we observe in Finland, the EMU, Japan, and the U.S. is a broad-based modern phenomenon. Central banks have won back their credibility. When oil prices fly higher, of course, the ‘CPI' gauge geos up, because oil is in it. But other prices generally do not join in. People do not form their expectations and firms do not make their pricing plans off of what oil does ‘today.' It is not just central banks having gained ‘credibility, however. It is true that central banks truly are more focused on inflation and on containing it. But it is also true is that in this effort they are back-stopped by a highly competitive environment. A number of factors make price discipline more of the law of the land than just what we get from having a more vigilant central bank. There is better communication which means more and faster information transmittal. There is the internet as a specific example of this that not only speeds pricing information rapidly, but it also facilitates sales of all sorts of products so that formerly remote localities where local firms used to have a virtual monopoly find that those firms cannot as easily exploit that monopoly power any more. There is rapidly changing technology that enhances information flow, low prices and labor conservation. And there is more trade and fierce international competition.

In this environment, consumers come to believe more strongly in price stability because it is not just about the central banks and trusting your local head banker. It is about the state of the world and a number of interlocking forces that keep price increases at bay with all sorts of implications including implications that keep your compensation and wages low. And people with poor prospects for a wage increase are much more diligent shoppers and that further reinforces the price disciplining trends. Firms feel as if they are trapped in a crucible with unrelenting pressure for low prices from consumers and intense heat from competitors. Trapped in this environment, pricing power and inflation melt away.

Finland hardly stands alone in this. But it is a good example and reminder of what is going on in the world as central banks take action to raise rates or ponder such actions. Is raising the base interest rate in the absence of inflation pressure really such a good idea? It seems that we are about to find out as the Federal Reserve in the U.S. plows ahead with policies and an objective for ‘wishing to make it so' as if ‘restoring' interest rates to some semblance of historic normalcy will restore normalcy to the economy around it. Will it? Soon we may find out if such a policy is wise or foolish.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief