Global| Oct 17 2018

Global| Oct 17 2018European Vehicle Registrations Plunge After Soaring

Summary

New inspection regulations push leads and lags behavior through new car sales trends New car sales in the European Union in September plunged after registrations had ramped up ahead of the introduction of new emissions inspection [...]

New inspection regulations push leads and lags behavior through new car sales trends

New inspection regulations push leads and lags behavior through new car sales trends

New car sales in the European Union in September plunged after registrations had ramped up ahead of the introduction of new emissions inspection rules.

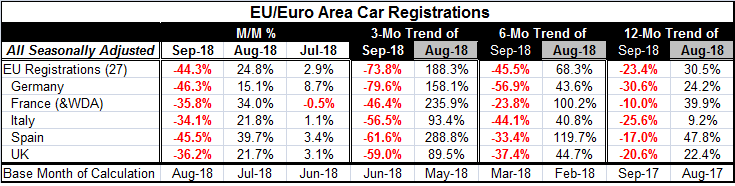

New car registrations fell 23% across the EU compared with a year earlier in September. New registrations had surged by 30% year-on-year in August. Month-to-month registrations plunged 44.3% after soaring by 24.8% in August. The introduction of the new WLTP (Worldwide Harmonized Light Vehicle Test Procedure) at the beginning of last month caused an exceptional surge in registrations in August. In September, that surge unwound.

European car makers had offered large discounts to offload noncompliant vehicles ahead of new emissions rules which came into effect in September, leading to increased competition and pricing pressure. Those discounts were responsible for the surge in August registrations.

The data show that these regulation effects dominate trends across markets as all EU members in the table show highly similar patterns of registrations surging in August then plunging in September.

The trends are present in the year-over-year data as well in the month-to-month behavior of buyers. By comparison, retail sale volume trends have been showing signs of topping, but looked at more broadly, retail sales are still on a trend rise. The trend for vehicle sales is a bit harder to pin down at the moment given its volatility.

While some data for Europe have been showing a slowing, for the most part growth is still in train. Fresh final inflation data released on the day show EMU inflation trends. The EMU HICP is at a 12-month gain of 2.1%, over the top of the EMU’s slightly less than 2% objective. But inflation, excluding food and energy (core inflation), has been dead flat at zero for two months in a row and the core is up by just 1.1% over 12 months. During the period, oil prices have been volatile and rising; the ECB has informally shifted its focus to core inflation from the headline. While the headline is just a bit more than a tick excessive, the core rate is undershooting by a wide margin. Still, there are disagreements within the ECB about how to proceed. Bundesbank purists will probably still be taken in by headline inflation excess. But the excessive headline for inflation in Germany itself has inflation up by 2.2% over 12 months; in France, it is up by 2.5%. But inflation excluding energy for both German and French inflation rates is well below the 2% mark.

Europe may be on the edge of a policy dilemma.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief