Global| Feb 02 2016

Global| Feb 02 2016European Unemployment Rates Continue to Fall and Remain High

Summary

It is a global paradox of sorts that unemployment rates are behaving relatively well even as economies do not. Part of it is the global slump in manufacturing which is a productivity-centric sector rather than a jobs-centric center. [...]

It is a global paradox of sorts that unemployment rates are behaving relatively well even as economies do not. Part of it is the global slump in manufacturing which is a productivity-centric sector rather than a jobs-centric center. So if manufacturing is weak, economic signals can be muted, but it may not cost a lot in terms of unemployment. It will cost growth and it will lower productivity gains, however.

It is a global paradox of sorts that unemployment rates are behaving relatively well even as economies do not. Part of it is the global slump in manufacturing which is a productivity-centric sector rather than a jobs-centric center. So if manufacturing is weak, economic signals can be muted, but it may not cost a lot in terms of unemployment. It will cost growth and it will lower productivity gains, however.

In the United States, the ISM manufacturing index is lower for several months running and industrial production is declining while unemployment is so low that the Federal Reserve has started to hike interest rates despite an absence of any actual inflation pressure. In Europe, the European Central Bank is still pedal to the metal as unemployment has continued to fall, and has fallen slowly while marking historically uncomfortably high levels for most EMU members. As always Germany's performance is leaps and bounds out ahead of most EMU members and of the EMU as a whole.

Japan just tilted policy to embrace negative interest rates. Japan's unemployment rate is 3.3%. Money can't leave China fast enough, giving it a real policy conundrum.

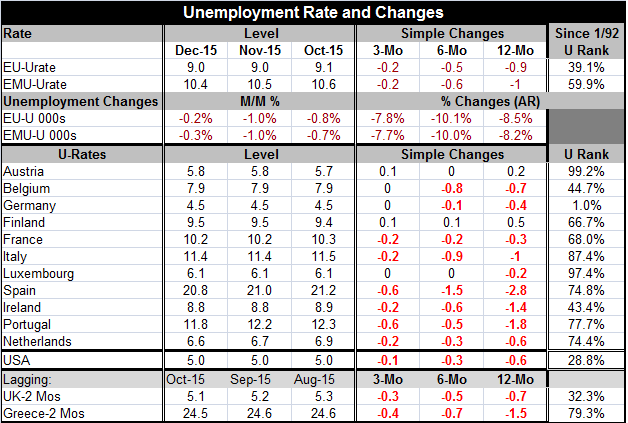

For all of the EU and EMU, the number unemployed over three months, six months and 12 months is declining. There also are declines in the number unemployed in at least each of the last three months. The signs of progress are clear, but it is also true that the annualized percentage drop for the number unemployed has slowed over three months compared to both six-month and 12-month.

The core of the hard currency EMU members (Austria, Belgium, Germany and Finland) shows no unemployment rate declines over three months, but both Belgium and Germany show declines over six months and 12 months. These countries also have some of the lowest unemployment rates in the EMU.

Unemployment rates are declining over three months, six months and 12 months in France, Italy, Spain, Ireland, the Netherlands and Portugal. Finland and Austria show no unemployment rate decline on any of these horizons and Luxembourg shows a decline over 12 months alone.

The lowest unemployment rates are Germany (4.5%), Austria (5.8%), Luxembourg (6.1%), and the Netherlands (6.6%). The highest rates again for reporters with December rates posted are Spain (20.8%), Portugal (11.8%), Italy (11.4%), and France (10.2%). Of course, less-up-to-date is Greece with an unemployment rate of 24.5% as of October. On the low side, there is EU member the U.K. with an unemployment rate of 5.1% in October.

The gap between the EMU rate and Germany peaked at 6.8 percentage points in 2013 and early 2014; it stands at 5.9% in December 2015. The gap is still large and the German rate is still falling, but the rest of Europe is catching up albeit slowly.

Germany's unemployment rate has been this low or lower only 1% of the time. Compare that to the U.S., which is another unemployment rate success story, with its rate at 5%, a rate that historically has been this low or lower 28.8% of the time. Germany is at an extreme position in terms of the level of its unemployment rate compared to history. Compare it to the EMU average the rate (which includes Germany) and is lower 59.9% of the time. Ireland's rate has been lower 43% of the time. Belgium's rate is lower 44% of the time. After those two countries, the next best is Finland with an unemployment rate that is lower two thirds of the time; higher only one third of the time. The rest of EMU members have rates lower 70% of the time or more; one has rates lower 80% of the time or less; two have rates lower 90% of the time or less. Austria is an exceptional result with an unemployment rate that is the second lowest in the EMU; yet it has been higher less than 1% of the time historically. Finland, France, Italy and Portugal have rates near at or above the 10% mark; Spain's is over 20% and Greece continues with one quarter of its workforce out of a job- one quarter.

Yes, there is progress in Europe. Unemployment rates are coming down as many writers are pointing out. It is a numeric fact, but one of dubious merit. A few countries have made great progress in absolute or relative terms. But the bulk of Europe is represented by countries with unemployment rates that remain high and are stuck high, moving lower in some very frustrating slow-motion technical dance. Four of 11 of the original EMU members in the table show unemployment declines of 1% or more over 12 months. Two more show declines of more than one half of one percentage points over 12-months; that's still only six of 11. Finland and Austria show net higher rates over 12 months; Luxembourg's rate is net lower by 0.2% points; France's rate is lower by 0.3 percentage points. Should we characterize this as good progress? Is it acceptable?

This is why the ECB is contemplating more action. The real question is: why is it contemplating? Why isn't it acting? If it has something it can do, it should be doing it.

Today also the PPI finalized for the EMU; all 10 of the reporting original EMU members through December show PPI declines on all horizons: three-month, six-month and 12-month. The pace of decline is slowing over three months compared to six months for each of those members. But in late December and January, oil has fallen further. Price trends tell us that distress is still being circulated through the pricing mechanism at the PPI level. Some central banks see the commodity price drop and strong dollar as anomalies that will pass. But they are passing slowly and some are getting worse as they `pass.' It's enough to make you wonder if the tactic to wait for the distress to pass makes any sense at all.

Yesterday Fed Vice Chair Stanley Fischer basically championed that view. The Fed can't figure out if the global selloff means anything for policy. That is a curious view. The Fed apparently also has the view that a declining manufacturing sector (in addition) is not an impediment to its view of rising inflation and coming rate hikes. One wonders, what would change the Fed's view? Policy in the U.S. is increasingly being run on the basis of dogma, something that is believed and does not have to be reaffirmed. Incoming data do not deter a dogmatic Fed. Every other central bank seems to have its eyes wide open. At the Fed, they are wide shut.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief