Global| May 23 2017

Global| May 23 2017European PMIs Scrape the Sky While Japan Scraps the Optimism

Summary

Themes of scraping and scrapping emerge this month as the EMU manufacturing and services gauges continue to post strong readings as well as truly stellar readings compared to previous scores in this business cycle. But Japan's [...]

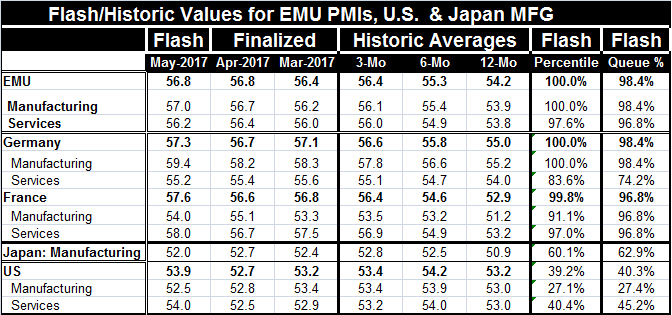

Themes of scraping and scrapping emerge this month as the EMU manufacturing and services gauges continue to post strong readings as well as truly stellar readings compared to previous scores in this business cycle. But Japan's manufacturing PMI steps back to mark a six-month low. So its six-month low meets six-year highs in this case. The U.S. is reporting out very moderate PMI readings in May, some of the weakest in the table and the weakest on a percentile standing basis.

Themes of scraping and scrapping emerge this month as the EMU manufacturing and services gauges continue to post strong readings as well as truly stellar readings compared to previous scores in this business cycle. But Japan's manufacturing PMI steps back to mark a six-month low. So its six-month low meets six-year highs in this case. The U.S. is reporting out very moderate PMI readings in May, some of the weakest in the table and the weakest on a percentile standing basis.

Asia is not showing the same ebullience as Europe. And even for Europe, we can question the staying power.

Asian prevarication

But for Asia, here are a few contrary readings du jour. It all starts with Japan's manufacturing PMI (table below) which is at a six-month low at a reading of 52.0. Manufacturing is still showing expansion, but it is not very solid. Japan's all-industry gauge which is only current through March fell at a pace faster than expected. This gauge wraps industry, services and agriculture. It fell by 0.6% in March (month-to-month), reversing most of February's 0.7% rise. In addition, there was an unexpected drop in Taiwan's index of industrial output which fell for the first time in nine months, dropping by 0.6% year-over-year in April.

EMU is doing well

In Europe, the overall EMU private sector gauge at 56.8 in May has been this high or higher only 1.6% of the time and is at its six-year high. The manufacturing sector is on its six-year high as well with the services sector strong at a reading that has been this high or higher only 3.2% of the time. For France, the overall PMI gauge is strong as are both sector gauges. Clearly France, Germany and all of the EMU are doing well on the PMI gauge.

Markit gauges supported by local survey results

Separately, European reports such as Germany's IFO, released today, show strength across a more detailed sector break out. Ranked over a broader horizon back to 1991, the all sector IFO gauge for Germany has been this high or higher only 0.3% of the time (yes that's zero point three percent of the time), a standing that puts it as its best level back to 1991. Manufacturing in Germany has finally recovered and logs a 97th percentile standing; the service sector components all rank extremely high in the IFO. Its business situation is the best score seen since at least 1991 while expectations have a 91st percentile standing. Germany clearly is hitting home runs here. Separately, a domestic gauge from INSEE in France evaluated the French manufacturing sector as the best since June 2011. The upbeat Markit surveys for Europe do not stand alone.

The euro-budget is better

Budgetary affairs in Europe are much better overall too. The U.K. did report a wider deficit in April and logged the highest April borrowing since 2014. But for the EU, only four member states are still under corrective procedure protocols: France, Spain, Greece, and the U.K. This is down sharply from the 24 countries that were under the corrective protocol in 2011... just six short years ago.

Meanwhile back at the ranch...

We await fresher economic news in the U.S. where conditions have been dodgy with markets reacting like there is a return of weakness as the bond market has rallied sharply and done a real investment led flip flop. Still, actual economic data are spotty and not really signaling any real change in the economy that has showed some weak consumer spending amid some surprisingly firm job growth and weak GDP. But the upcoming Q2 GDP report is looking more like it will break out of this weakness and post a significant rebound for GDP. The just released U.S. PMI readings from Markit are not along for that ride. They underscore U.S. weakness and represent much weaker readings that are present in the U.S. ISM PMIs gauges. How the U.S. economy performs will be important with Asia sputtering and Europe looking strong. However, the U.S. stance on trade is still worrying our trade partners. The release of the Trump budget is just one more perplexing aspect as the President has a framework to balance the budget eventually but wants to sell oil from the SPR to fund some of his programs and to make huge cuts to Medicare and to food stamps, programs whose shrinkage will adversely affect the poor. All in all, the President's budget is a political document if nothing else. It would seem to have little chance of passing. And as a source of stimulus for the economy it is looking less and less viable the more we see of it. It is hard to imagine politicians who want to be re-elected voting to eviscerate Medicare and food stamps.

Geopolitics is not a supporting player to growth

S&P has put Brazil on a negative credit watch over its unfolding political drama. This barbaric attack against young concert-goers in Manchester England which is being claimed by ISIS once again points to lingering global issues. The ISIS 'Caliphate' is now confined to a relatively small 10 square mile area and as its base is further shrunk it will be left with no way to make an impact except by acts of terror. In some ways, ISIS may be about to become more dangerous. North Korea has become more dangerous. Russia remains dangerous as it continues to stir things up in Ukraine and to saber rattle around the Baltics. In addition, it is a cause of confusion on the U.S. political scene.

Economic cycling

The economic cycle may have turned in Europe. It has not turned in Japan and the U.S. continues to defy any simple characterization of its state. It really sounds like it's all just about the same 'business as usual' but with participants simply trading hats to signify their changed business cycle positions and with the central bankers still stuck in their same old ruts. Europe's data turnaround has not yet impressed policy at the ECB. In the U.S., markets have shifted, but it's not clear if the Fed has been derailed from its multi-rate hike plan. In Japan, it's as though nothing has changed and data cycle to the better and to the worse month-to-month without changing opinions or even expectations. The times remain strange in many respects.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief