Global| May 02 2016

Global| May 02 2016European Manufacturing PMIs Make Small Gains in April

Summary

In these early reporting EMU countries (Germany, France, Italy, Spain, Austria, and the Netherlands), the manufacturing PMIs are lower in three in April (France, Austria, and the Netherlands). Only two were lower in March (France and [...]

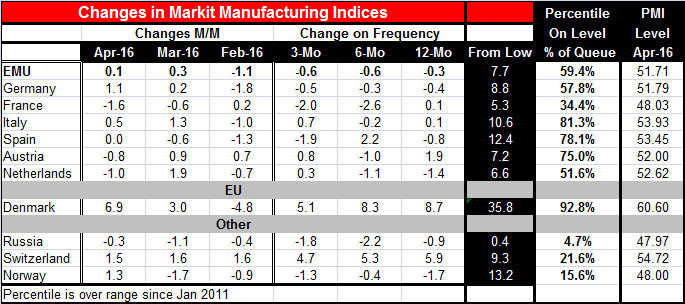

In these early reporting EMU countries (Germany, France, Italy, Spain, Austria, and the Netherlands), the manufacturing PMIs are lower in three in April (France, Austria, and the Netherlands). Only two were lower in March (France and Spain). But four - plus all of the EMU- were lower in February. Over three months, the Markit manufacturing indices are lower in three countries plus in all of the EMU. Over six months, only Spain is higher. Over 12 months, Austria is higher along with barebones gains in France and Italy. All in all, this is not impressive stuff.

In these early reporting EMU countries (Germany, France, Italy, Spain, Austria, and the Netherlands), the manufacturing PMIs are lower in three in April (France, Austria, and the Netherlands). Only two were lower in March (France and Spain). But four - plus all of the EMU- were lower in February. Over three months, the Markit manufacturing indices are lower in three countries plus in all of the EMU. Over six months, only Spain is higher. Over 12 months, Austria is higher along with barebones gains in France and Italy. All in all, this is not impressive stuff.

Despite what are rather widespread gains in manufacturing PMI gauges as of April, the gains are small and the overriding problem is still that EMU and country-level manufacturing readings are largely without upward momentum (see the graphic as well for corroboration).

The percentile standing metrics for the EMU show Italy, Spain and Austria with queue standing positions from the 75th to the 81st queue percentiles. These are relatively firm readings but not outstanding readings. For the EMU as a whole, the queue percentile standing is in its 59th percentile. Germany stands lower in its 57th percentile and France stands lower still in its 34th percentile.

Elsewhere in Europe, Denmark has a very strong 92nd percentile standing with Russia, Switzerland and Norway each posting queue standings below their respective 25th percentile levels. Russia's sector is in the lower 5% of its historic queue of data (as weak or weaker only 5% of the time since January 2011!).

Denmark and Austria, two relatively small or specialized economies, are the exceptions to the general pattern in this table. They each show substantial gains in manufacturing being made over 12 months, six months and three months.

Manufacturing PMIs overall

The improvement in PMIs in April is not changing the momentum in Europe. Moreover the queue standings with a few specialized exceptions show still very weak manufacturing sectors. With the Federal Reserve in its recent meeting having taken the spotlight off of international risk and weakness, it is important to note that the Fed has done what it has done for its own reasons. Conditions in the international economy are broadly unchanged and still are touch-and-go. Monetary policy has virtually pulled out all the stops while fiscal policy remains under lock and key most places with few exceptions (like China).

PMI lexicon vs. percentile standings

The actual traction being generated is small and I recommend not getting carried away with the PMI lexicon that anything above 50 on a PMI index indicates expansion. What we want to do is to evaluate performance relative to historic standards and the queue standings do that best. PMI levels are below 50 in April in France, Russia and Norway in this table. Yet Russia's 47 diffusion value seems only slightly below 50 until you see it has a queue standing in its bottom 5%- it is weaker only 5% of the time. The queue standing clearly provides a better perspective than the notion that sector is either expanding or contracting. We do want to know how countries are performing relative to past standards. On that basis, there is still a lot of moderation and weakness with few places where we can breathe easily. And since the countries where PMIs are strong are not exactly large countries, they really don't carry much weight when it comes to breathing a sigh of relief. Despite the Fed's policy statement this past month, we are all holding our breath to some extent.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief