Global| Nov 13 2009

Global| Nov 13 2009European GDP Turns Higher-But Disappoints

Summary

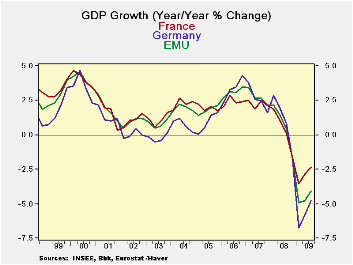

European GDP turned higher in Q3 but the results were generally less than expected. Among the early ‘flash’ GDP reporters France posted a small rise but it was the second rise in a row for France. Greece with always volatile results [...]

European GDP turned higher in Q3 but the results were

generally less than expected. Among the early ‘flash’ GDP reporters

France posted a small rise but it was the second rise in a row for

France. Greece with always volatile results posted the strongest rise

followed by Austria. Italy and The Netherlands have the largest Yr/Yr

declines in this group; the EMU Yr/Yr drop is of 4.1%. Greece is lower

Yr/Yr by just 1.6% Austria but just 2.2%. Germany the largest e-Area

economy is off by 4.8% Yr/Yr even though it has two quarters in a row

of solid growth under its belt.

Flash reports do not provide any GDP detail but the various

authorities do offer some account of their results. Both Germany and

France cited the role of exports in pushing growth ahead. In Germany

investment demand was also described as a key factor.

Paragon of strength or parasite of growth?

-- An unfolding theme in the Area is that exports, external demand, is

driving the European recovery. In France domestic demand was flat in

the quarter despite a ton of ongoing stimulus that has left France

unable to get its fiscal budget gap in line as soon as the EU

Commission wants it to. Hungary, in its GDP release today, complained

that exports were weak and that was sapping GDP strength. The largest

industrial economies would seem to be good candidates to spur world

growth with their own domestic demand instead of relying on the demand

increases elsewhere. Chancellor Merkel has defended Germanys ‘right’ to

be a leading exporters, Japan always seeks a surplus to ‘defend’

against the country’s lack of oil and dependence on oil and other

natural resource imports. China’s trade surplus grew larger last month.

How can ‘everyone’ have export led growth? How can the US (whose

current account deficit surged in November) get its deficit in line if

major competitor countries insist on running trade surpluses, spurring

exports and maintaining weak domestic demand at home? This is something

the G-20 has been completely unable to sort out.

These sorts of structural imbalances helped to lead to the

last financial crisis. Such flows underpinned the 1973-78 oil boom-bust

cycle. Factors that put persistent surpluses sand deficits in play are

dangerous and the G-20 has not plan to sort it out. At the weaker

dollar works to mitigate the US imbalance problem even if it is playing

with fire.

| European Growth for Selected Flash GDP Results | ||||||

|---|---|---|---|---|---|---|

| Q/Q Saar | Yr/Yr | |||||

| Q3-09 | Q2-09 | Q1-09 | Q3-09 | Q2-09 | Q1-09 | |

| Austria | 14.0% | -3.7% | -13.8% | -2.2% | -5.4% | -4.8% |

| France | 1.1% | 1.1% | -5.5% | -2.4% | -2.9% | -3.5% |

| Germany | 2.9% | 1.8% | -13.4% | -4.8% | -5.8% | -6.7% |

| Greece | 17.6% | 32.7% | -29.8% | -1.6% | -1.2% | -0.5% |

| Italy | 2.4% | -1.9% | -10.5% | -4.6% | -5.9% | -6.0% |

| Netherlands | 1.7% | -4.0% | -9.4% | -4.0% | -5.1% | -4.2% |

| EMU | 1.5% | -0.7% | -9.6% | -4.1% | -4.8% | -4.9% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief