Global| Sep 14 2017

Global| Sep 14 2017European Car Registrations Pick Up in August

Summary

After falling for two months in a row, European car registrations sprang back strongly to gain 11.9% month-to-month in August. Still, the drops in the previous two months dominate the trend as the three-month (annualized) growth rate [...]

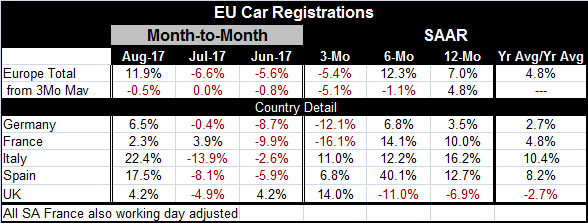

After falling for two months in a row, European car registrations sprang back strongly to gain 11.9% month-to-month in August. Still, the drops in the previous two months dominate the trend as the three-month (annualized) growth rate for car registrations is -5.4%; but the six-month (annualized) growth rate is 12.3% and change over 12 months is 7%.

After falling for two months in a row, European car registrations sprang back strongly to gain 11.9% month-to-month in August. Still, the drops in the previous two months dominate the trend as the three-month (annualized) growth rate for car registrations is -5.4%; but the six-month (annualized) growth rate is 12.3% and change over 12 months is 7%.

Growth rates calculated from three-month averages of data show a bit more lingering weakness with growth lower in two of the last three months and lower on balance over both three-month and six-month and higher year-over-year by 4.8%. The long-term smoothed average that calculates the 12-month average gain relative to the 12-month average of 12-months ago finds a similar rise of 4.8%. Euro area sales momentum of about 5% seems well entrenched by those two longer term gauges.

Viewed by countries, sales were higher in all five markets in August with France the weakest logging a rise in registrations of just 2.3%. Italy and Spain are the strongest by far, with gains of 22.4% and 17.5%, respectively. In both cases, those two countries were coming off substantial monthly drops in registrations in July.

Over three months, annualized growth rates are lower on balance in Germany and France where each country logs a double-digit drop. These results contrast with double-digit gains in Italy and the U.K. as well as a solid gain in Spain.

Over six months, only U.K. registrations drop and the annualized growth rate drop is in double digits. Spain logs a ridiculous growth rate of 40.1% over six months as Italy and France show double-digit gains and German registrations rise at a 6.8% pace.

Over 12 months, France, Italy and Spain have double-digit gains with German registrations at a weaker 3.5% pace. The U.K., however, logs a year-on-year decline to go with its six-month drop. Recent U.K. monthly sales have been bouncing up and down. The U.K. market is looking more like it is struggling.

The European Central Bank is vetting all the economic statistics more closely to get a sense of economic strength. Today's data seem pass the test of strength as the weakest sales are in the U.K. outside the domain of the ECB. EMU-area countries' registrations remain solid or even solid-to-strong. Inflation has shown some firmness in the euro area over the last four months as well. Economic data continue to give the ECB the basis it will need to begin its policy shift to less accommodation.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief