Global| Mar 15 2018

Global| Mar 15 2018European Car Registrations Fall- What Does It Mean?

Summary

Auto sales are a very cyclical economic variable. They are usually very good at pegging the business cycle. However, registrations in Europe are now following a path that is a bit hard to place. Forecasting and making economic [...]

Auto sales are a very cyclical economic variable. They are usually very good at pegging the business cycle. However, registrations in Europe are now following a path that is a bit hard to place.

Forecasting and making economic assessments sometimes is a more straightforward proposition than it has become these days. The current low level of interest rates is clouding policymaker's judgments as they all are filled with the "fear of God" that policy has been too easy for too long and that this will unleash a powerful inflation pulse at some yet-to-be-determined time in the future. At the same time policymakers are disappointed that all their efforts at stimulus have borne such little fruit. Europe suffered some prices deflation and worried that it might have been worse. European monetary policy all-but jumped through hoops and a Herculean effort was made to bring the Germans on board for participation by the central bank in a stimulus program that Germans had no taste for.

However, even after all of that, inflation continues to run below target and even though in Germany, the hottest economy in Europe with the least slack and lowest rate of unemployment, there is no clear evidence that inflation pressures build. Yet, because of past policies and their interaction with post-War dogmatic beliefs policymakers sniff a pick-up in growth and divine the potential for inflation everywhere. Is Europe planning an exit from stimulus before inflation is planning a presence?

Yet in Europe EMU retail sales have been moderate. And car sales are erratic across Europe with much weaker sales in the UK in the wake of its Brexit decision.

Vehicle sales which are usually a solid cyclical signaling mechanism continue to rise from the ashes of their recession- and post-recession lows, but have not yet reacquired their pre-recession peaks. And, the harsh reality is that, in this cycle, they may not make a new peak.

The chart on the left shows overall European auto registrations. They have moved higher more or less steadily given the intrinsic variability in the registrations data. The pace of sales gains was dialed back about a year or two ago and, while growth has continued, the pace has been reduced.

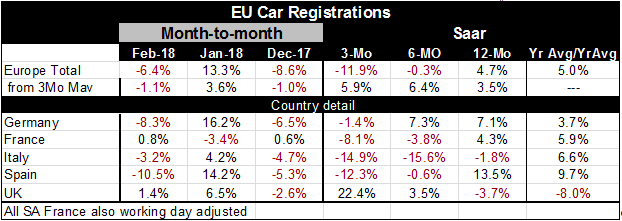

Country level data show us the clear fall off in UK car sales in 2017 although there is some revival in UK registrations from the low level and the revival has life over a period of several months. Sales in France and in Italy are trending lower. Germany, where sales had previously been floundering in the wake of emission standards scandals, is now showing some revival.

However, the trend for European sales is not clear and signal from sales about the state of the business cycle is not clear either.

The data in the table below show us that Europe-wide registrations are lower by 6.4% in February after a 13.3% surge in January and an 8.6% drop in December. With that sort of volatility it is no wonder that solid trends are hard to extract from this report.

Growth rates based on three-month averages of data show that growth from 12-months to 6-months to 3-months is on a somewhat accelerating path. But raw growth that is unsmoothed shows a steady deterioration in the growth rate of registrations from 4.7% over 12-months to -0.3% over 6-months to -11.9% over three months.

However, if we look at the growth rates of registrations as a time series using both smoothed and unsmoothed data over a long period we find that for both series there is a very steady deceleration that has been in place since early 2017. Unsmoothed data show it, as we point out above, on trends inside one year: the steady erosion in the rate of growth of registrations from 12-months and in. Smoothed data that make the same calculations for 3-month averages of data show that there is currently a bit more strength than for unsmoothed data but there is still a broader loss in momentum that is underway despite some modest firming in growth over 3-months and 6-months. Broad trends point to an ongoing slowdown in registrations.

In the US auto sales already have begun to run out of gas. They had been losing momentum late last year then revived as hurricanes damaged a huge quantity of cars in Texas and in Florida, After that, unit auto sales in the US popped back above trend. But now with the special demand caused artificially by hurricanes gone, sales in the US are well below trend and decaying again.

Of course, in the US interest rates also are rising and rates are not yet elevating in Europe. Based on central bank actions the US is well ahead of Europe in the tightening cycle. But also in the US as in Europe retail sales have failed to move to the fore to drive growth. European retail sales volumes are up at a 2% pace which makes sales slower in January than in seven of the previous 12 monthly readings (on year-over-year growth rates). In the US economists are looking for some impact from the new tax package and instead retail spending is lower in February for the third month in a row - in nominal terms.

The thing to watch in this expansion is the consumer sector. Consumer readings in the US and in Europe are all still somewhere between solid and strong. But Italy is a good example where consumer confidence readings seem to have come unglued from reality. Confidence readings are actually quite good yet in Italy; yet, GDP levels in real terms are still below their past cycle peak. Italy has still not fully recovered from the last recession of a decade ago; it has not even restored real variables to their previous levels and yet consumers seem relatively content; even happy! Yet voters are clearly much more restive. I think we need to be careful about how we vet consumer confidence data. It is never clear to me how much relativity there is a consumer's response. Are consumers relatively more content with the conditions that exist today than they would have been had we polled them with the same circumstances one decade ago? Have consumer expectations been set lower so that they are now easier to surpass? And does that make the surveys less useful?

There are three salient trends to watch. One is that Asia is lagging behind Europe (and the US) as growth has turned up recently. Western PMI data in particular are stronger than Asian PMI reports. Still, a lot of manufacturing comes out of Asia so Asia still has a lot of potential to ramp up output. This should make the emergence of inflation in Europe less likely despite relatively highly usage resources in the West. The second point is that Asia never drives anything with consumption. Asia fulfills the Westerner's demands; Asian consumers tag-along with weaker spending supported by weaker wages and higher rates of savings. The final piece of this puzzle is how the US trade position is going to play out. How aggressive will the US really be and what will be the responses? The US clearly has done the least to protect its markets. It has run a string of persisting current account deficits that extend back to the early 1980s. By comparison Germany has one the highest and most stubborn ratios of current account surpluses to GDP in the world. By any standard it is clear that by enforcing commercial policy or nontariff barriers or exchange rate manipulation the US has been gamed in the world of Free Trade. Foreigners have been given free rein in the US market and the US has been shut out of or severely restricted in markets overseas. And while the US may have some deficiencies that explain some this poor performance, exchange rates, left on their own, should have moved to help the US restore balance to its balance of payments. But exchange rates have not been free. They have been manipulated. They are part of the problem.

Yes, Asia and Europe want to continue trade under the old rules. But the old rules were not fair and no longer are an option. Are they going to be willing to share global demand with the US in a fair fashion or will Donald Trump be forced to push harder to gain fair treatment for the US? How much damage does the global economy want to suffer before it is willing to share? This is an important question for global growth as we look ahead. Many brand the US as the bad guy in this game of pressure. I don't.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief