Global| Oct 16 2015

Global| Oct 16 2015European Car Registrations Continue to Surge Higher Year-over-Year

Summary

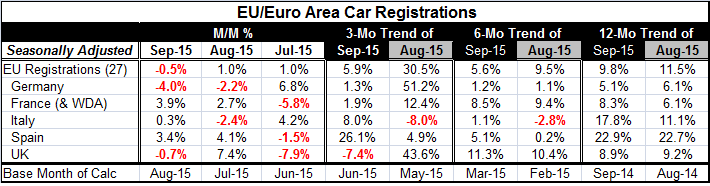

Car registrations in Europe edged lower month-to-month but continue to show solid and strong gains year-over-year across all the countries and aggregates listed in the table. European registrations are up by a strong 9.8% year-on- [...]

Car registrations in Europe edged lower month-to-month but continue to show solid and strong gains year-over-year across all the countries and aggregates listed in the table. European registrations are up by a strong 9.8% year-on-year. That pace, however, is somewhat slower in the neighborhood of 5.5% to 6% over three months and six months.

Car registrations in Europe edged lower month-to-month but continue to show solid and strong gains year-over-year across all the countries and aggregates listed in the table. European registrations are up by a strong 9.8% year-on-year. That pace, however, is somewhat slower in the neighborhood of 5.5% to 6% over three months and six months.

Germany's registrations are up by 5.1% over 12 months and slow to growth rates of 1.2% over six months and 1.3% over three months. Germany is now in the grip of the Volkswagen scandal and with a 4% drop in registrations in September there is a hint of something wrong. The 4% drop is the second consecutive monthly registration drop and the largest monthly setback since May of this year when sales fell by 7.8% in one month. In September the two-month sales drop is 6.1%; that is the largest two-moth drop since May 2013.

French registrations are doing quite well. They are up by 8.3% year-on-year with an 8.5% pace over six months and a slower 1.9% pace over three months. Despite that slower growth, the last two months have seen extremely strong monthly gains. It was weakness in July that slowed France's three-month gain. It looks as though that weakness has been shaken off.

Italy's gains are strong year-on-year at 17.8%. But the pace slows to 1.1% over six months then jumps back up to a solid 8% pace over three months. However, recent monthly Italian registrations have been faltering.

Spain shows quite strong gains of 22.9% over 12 months that slip to 5.1% on six months and jump back to a 26.1% pace over three months. Spain has had the most consistently strong sales in this group over the past year.

The U.K., an EU member country, has an 8.9% gain over 12 months. That strengthens to 11.3% over six months then the trend crashes as the U.K. shows the only net contraction in registrations over three months with a decline at a robust -7.4% annual rate.

The U.K. shows registration declines in two of the last three months but with a strong pop in between in August. In contrast, the weakness in Germany is in the most recent and consecutive months. Italy shows one monthly drop in the last three months, that being in August. Spain and France each have one-month declines in July.

On balance, despite the strong year-over-year results the monthly patterns have us wondering the most about the U.K. and Germany. Italy shows two recent weak months even if only one of them was a decline. Registrations in France and Spain seem solid enough. But this weakness in registrations may not be indicative of overall sales weakness. Germany still has steady retail sales through August as does the UK. France and Italy show retail sales through July with French sales solid and Italian sales looking a bit slippery. Spanish sales are solid.

On balance, Europe's auto sales/registrations are much like those in the U.S. They are stronger by far than any other sector in the economy. I suspect that there are two reasons for this. First, while banks are being closely watched and residential lending is occurring only for those with the best credit quality, auto lending is often done outside the banking system using securitization. This form of asset-backed lending has been able to deliver credit even to those with too poor credit standing to buy a house. Secondly, autos are a big-ticket item and not purchased weekly like groceries. Having a large proportion of the population feeling more secure and working may be enough to generate solid auto sales even with large blocks of disadvantaged workers. A recovery in autos can occur on smaller base of well-off consumers than can general retail sales.

Looking ahead:

The auto sales recovery has been able to carry both Europe and the U.S. to the recoveries they currently enjoy. Butt can these sales continue on the torrid path they have had? Will slowing in auto sales slow retailing in general or will it be an opportunity for retail funds to matriculate into other sectors? Finally, will the problems with Volkswagen continue to significantly affect Germany?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief