Global| Apr 17 2013

Global| Apr 17 2013Europe's Car Registrations Show Faint Pulse

Summary

European car registrations continue to be very weak. Short term trends show some lift. But year-over-year trends are lower by 10.3%. The smoothed, 3-month average trend shows a drop of nearly 12% over 12-months and shows less [...]

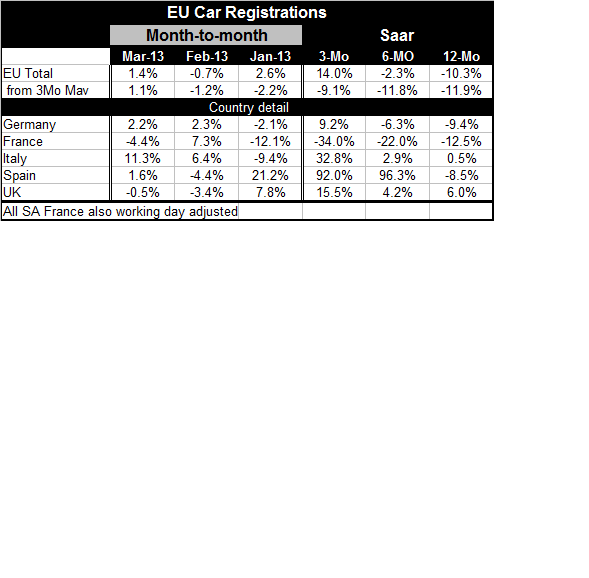

European car registrations continue to be very weak. Short term trends show some lift. But year-over-year trends are lower by 10.3%. The smoothed, 3-month average trend shows a drop of nearly 12% over 12-months and shows less favorable short term trends as well, slipping at a 9.1% pace over three-months and at an 11.8% pace over six-months.

European car registrations continue to be very weak. Short term trends show some lift. But year-over-year trends are lower by 10.3%. The smoothed, 3-month average trend shows a drop of nearly 12% over 12-months and shows less favorable short term trends as well, slipping at a 9.1% pace over three-months and at an 11.8% pace over six-months.

The car registrations series is very 'noisy' even though it is seasonally adjusted- that is apparent from the graph of the data above. Some series are simply very hard to seasonally adjust. For car registrations, the year-over-year and smoothed series may give the best guide to performance and trends. .

Despite the weakness in registrations the series hints at making a bottom looking at smoothed three-month averages of the data country-by-country. Spain's year-over-year weakness has improved since bottoming in November. Italy is showing less weakness since hitting a near eight-month flat spot in terms of its year-over-year rate of decline. France's year-over-year drop has eased for two months running. Germany, however, is the fly in the ointment with the barest of improvements in its year-over-year pace of deterioration in March. In the UK, where registrations have been on a steady rise, March brought a flattening of the year-over-year trends.

On balance activity in the Zone is pressured. Car registrations are been one of the true casualties of the European downturn. European sales are off 32% from their pre-recession peak. Germans sales are off by a 29%, Sales in Italy are down by a huge 46%; in France, sales are off by 38%, in Spain they are off by an outsized 57%. UK sales have been on the mend and are off from their prerecession high by less than 14%.

These results compare to US vehicle sales that are off by 13% from their pre-recession peak with car sales off by 11% and trucks ales off by 17% but with the sale of imports off by much more: 23% for cars and 34% for imported trucks.

Consumer durables were hit hard by the global recession. Registrations in Europe are up by only 3.3% from their cycle low; 1.1% using the smoothed data. Germany is up 8% from its low, France is up less than 3% from its low. Italy is up 18% from its weakest recession reading with Spain and the UK up by some 40% from their respective low points. These data compare to the US where sales of domestically manufactured vehicles are up 92% from their cycle low. Europe is still very much floundering.

The European crisis continues to have many moving parts, among them the fact that no sustainable plan is on the table and the financial crisis is still percolating in the periphery. The inability to solve the riddle of the core Vs the middle is causing growth to dwindle. Cyprus continues to haut the eZone and recent comments by German economic 'wise men' surely must exacerbate fears of what lies in store for those in the Zone that still have things to fix. Politics in Italy are de-stabilizing, and one can only wonder what will come out of Germany when its elections are put behind it. In this environment it's hard to get too excited by European growth prospects.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief