Global| Apr 30 2010

Global| Apr 30 2010Euro Unemployment Bucks Image Of Recovering Region

Summary

European unemployment continues to rise in March and the figure reported for 2010 in-Q1 in Spain reached 20%; We report monthly data in the table above. Only Germany shows any hint of a turn to lower rates of unemployment. Of course [...]

European unemployment continues to rise in March and the figure reported for 2010 in-Q1 in Spain reached 20%; We report monthly data in the table above. Only Germany shows any hint of a turn to lower rates of unemployment. Of course we know that the unemployment rate lags the cycle, but we are now pretty well into this cycle and the ongoing unemployment difficulties are beyond what has been cyclical normalcy.

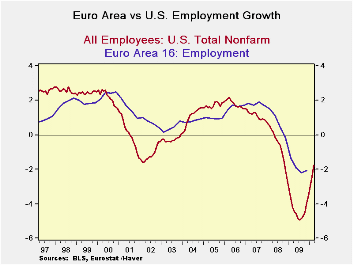

The chart at the top juxtaposes the EMU trend to the US trend for employment. Two things stand out. One is that the US series is more volatile than the European series with generally higher highs and lower lows. The other is that the low in this recent recession was much worse in the US than it was for Europe where the social safety net is much cushier. Still the turn after the fall has been much sharper in the US where Yr/Yr job losses are now occurring at a slower pace than they are in Europe.

One price that Europe pays for more government intervention in its economy is less economic vitality. The US economy is mending faster from what was admittedly a harder fall. But the US appears to be on the road to repair as jobs and GDP are showing sharper turnarounds even if they are still struggling

In Europe unemployment is very slow to repair and unemployment rates are generally still rising. Spain’s 20% rate of unemployment in 2010 Q1 is a huge burden to that economy. Also it socks a wicked punch to the rate for all of EMU that will give even the inflation-angst-ridden ECB pause on how it views inflation risks.

One of the biggest problems for the ECB is making policy in a one currency zone that has multiple fiscal policies. The regional unemployment rates in Europe have a different meaning than the regional and state-level reports in the United States where the country, currency and fiscal situation all are under one umbrella (except for state and local budgets, of course).

The recent problems in Greece and credit down grades meted out to Spain and to Portugal simply underline the sort minefield though which the ECB must pick its way. Even the tough-minded Germans did a sharp about face yesterday when the situation in Greece turned sharply for the worse. True, Germany’s stance is complicated by its being in the middle of elections. But such is the risk in such a community. With such a disparate flock of counties; there are always going to be elections somewhere in Europe. The game of musical chairs played in economics and by financial markets does not agree to let the music keep going just because one key country has an election. Contrarily, chances are that such an event brings more attention to bear on a tough call that is in the middle of deciding.

Having separate fiscal policies has just revealed what its risks are. Germans are hot that Greeks ‘lied’ bout their fiscal position and did it for the second time. But I really don’t see any reason for surprise. These countries want to have separate fiscal polices and separate political relations. Still they do want to become a single economic zone but not a country called ‘Europe.’ Their tendency to call themselves European breaks down into a laughable faced of falsity when things go wrong. Then they return to being German, or Dutch, or Greek, or whatever.

As to their relations, nations have always lied to one another. It is known as diplomacy. Diplomats are among the best trained in their respective countries and they are taught to meet you face to face and to mis-represent their country’s views from time to time for their own advantage speaking to you in your language and doing it with eloquence. I don’t see why Germans are so upset that Greeks fudged their fiscal position because to the Greeks it may have seemed ‘fair game.’ Clearly the Mass-Trick laws do not punish a county enough for cheating yet its restrictions are burdensome enough to make nations want to avoid them and cheat. Are the Mass-trick restrictions too severe to be obeyed?

Europe must take a good hard look at itself and decide what relations it wants to reserve for its member countries and which it wants to assign to an amalgamated European zone ( it already has done this is the treaty that was ‘approved across member countries. But it may need to do some fine tuning on what the ‘state’s’ rights and responsibilities really are). We need to know in what sense EMU is Europe and what sense is it not. And Europeans need to figure out when they draw that line exactly what it means.

If they are going to continue to have the usual diplomatic relations, and if they do not want those standards to percolate to their economic relations, then they are in need of requiring an independent AUDIT for each country just as there is such a requirement for a bank. Because either you can believe the numbers or you can’t. Europe needs to adopt one common set of budget accounting rules and to stick to them, to monitor them (audit compliance to them) and to enforce them. Then it may have a chance to succeed under its separate country/budget model should it choose to stick with it.

Even if it does this it will find its economic results will remain disparate because Europe is not uniform.

| Unemployment rate and changes | ||||||

|---|---|---|---|---|---|---|

| Rate | Level | Simple Changes | ||||

| Feb-10 | Jan-10 | Dec-09 | 3-Mo | 6-Mo | 12-Mo | |

| EU-Urate | 9.6 | 9.5 | 9.4 | 0.2 | 0.4 | 1.3 |

| EMU-Urate | 10.0 | 9.9 | 9.9 | 0.1 | 0.4 | 1.2 |

| Unemployment rate and changes | m/m% | Changes (ar) | ||||

| EU-U 000s | 0.6% | 0.9% | 0.5% | 2.0% | 4.3% | 15.8% |

| EMU-U 000s | 0.4% | 0.7% | 0.3% | 1.4% | 3.4% | 13.3% |

| U-Rates | Level | Simple Changes | ||||

| Germany | 7.5 | 7.5 | 7.5 | 0 | -0.1 | 0.2 |

| France | 10.1 | 10 | 10 | 0.1 | 0.4 | 1.2 |

| Spain | 19 | 18.9 | 18.9 | 0 | 0.3 | 2.3 |

| USA | 9.7 | 9.7 | 10 | -0.3 | 0 | 1.5 |

| Japan | 4.9 | 4.9 | 5.2 | -0.4 | -0.5 | 0.5 |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief