Global| Feb 17 2010

Global| Feb 17 2010Euro-Area Trade Surplus Moves Up Sharply

Summary

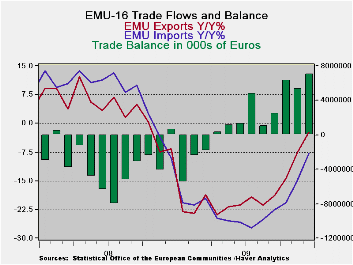

Exports rebounded strongly in December after coming up flat in November. Overall exports rose by 3.1% in December as MFG exports rose by 2.7% in December. Three month growth rates continue to show strong growth, accelerating slightly [...]

Exports rebounded strongly in December after coming up flat in November. Overall exports rose by 3.1% in December as MFG exports rose by 2.7% in December. Three month growth rates continue to show strong growth, accelerating slightly for overall exports but with MFG exports losing a bit of momentum compared to their six-month pace

Import growth is positive. Its three-and six-month rates of growth have steadied at or below the 10% growth rate mark. Manufacturing import growth is positive but barely growing at all, rising at 0.3% annualized rate of growth over three months, having slowed from nearly a 7% pace over six months.

Europe’s trade surplus is at a five year high. Exports are at their highest level in 12-months as well. Europe continues to act as a region with export-led growth. Exports are digging out from the recession faster than imports. Imports are lower by 8% Yr/yr compared to exports that are lower by just 2%.

Domestic demand is lagging in the Euro-Area. Exports are pulling the region into recovery faster than its own consumers. Europe’s recovery depends on the continuation of global growth as much as any region.

| Euro-Area Trade trends for goods | ||||||

|---|---|---|---|---|---|---|

| m/m% | % Saar | |||||

| Dec-09 | Nov-09 | 3M | 6M | 12M | 12M Ago | |

| Balance* | € 7,003 | € 5,294 | € (3,252) | € 4,482 | € (3,450) | € 1,384 |

| Exports | ||||||

| All Exp | 3.1% | 0.0% | 25.6% | 22.6% | -2.3% | -6.6% |

| Food and Drinks | 4.8% | 1.7% | 18.3% | 10.6% | -1.9% | 4.6% |

| Raw materials | 7.7% | -0.7% | 51.4% | 31.5% | 24.6% | -19.2% |

| Other | 2.9% | -0.2% | 25.6% | 23.4% | -2.9% | -7.1% |

| MFG | 2.7% | -0.3% | 17.7% | 21.3% | -5.2% | -7.2% |

| IMPORTS | ||||||

| All IMP | 1.7% | 0.9% | 7.2% | 10.7% | -7.8% | -9.1% |

| Food and Drinks | -1.3% | 3.2% | -14.0% | -3.1% | -8.7% | 1.7% |

| Raw materials | 4.4% | 3.2% | 41.2% | 43.8% | -19.0% | -6.3% |

| Other | 1.7% | 0.6% | 7.5% | 10.5% | -7.2% | -9.9% |

| MFG | 1.5% | -0.1% | 0.3% | 6.9% | -9.2% | -8.5% |

| *Eur mlns; mo or period average | ||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief