Global| Nov 15 2017

Global| Nov 15 2017Euro Area Trade Surplus Jumps to New Record!

Summary

The euro area trade surplus jumped sharply in September, reaching its maximum surplus since the euro area was formed at 25.044 billion euros. The EMU current account surplus as a percentage of GDP reached 2.67% in Q2, the most recent [...]

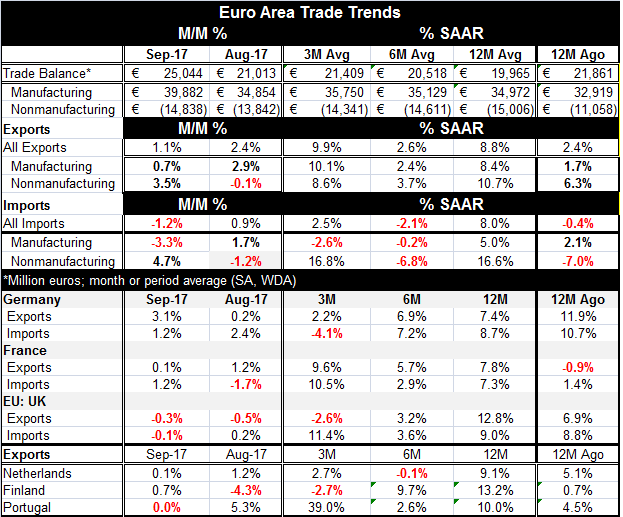

The euro area trade surplus jumped sharply in September, reaching its maximum surplus since the euro area was formed at 25.044 billion euros. The EMU current account surplus as a percentage of GDP reached 2.67% in Q2, the most recent data for that metric and at that level it ranks as the 15th highest ratio in the last 74 quarters over the period that the euro area has existed back to 1999. Germany is an important contributor to this result. While the German surplus as a ratio of GDP stood at 'just' 7.2% of GDP in Q2 (for a ranking of the 15th largest ratio on that same timeline), the German ratio for Q3 is now available and it stands at 8.2% and is the 7th largest ratio of current account surplus to GDP in the last 75 quarters. So much for global trade flows moving to adjust their imbalances. Remember these huge imbalances were a big factor behind the financial crisis we are still emerging from.

The euro area trade surplus jumped sharply in September, reaching its maximum surplus since the euro area was formed at 25.044 billion euros. The EMU current account surplus as a percentage of GDP reached 2.67% in Q2, the most recent data for that metric and at that level it ranks as the 15th highest ratio in the last 74 quarters over the period that the euro area has existed back to 1999. Germany is an important contributor to this result. While the German surplus as a ratio of GDP stood at 'just' 7.2% of GDP in Q2 (for a ranking of the 15th largest ratio on that same timeline), the German ratio for Q3 is now available and it stands at 8.2% and is the 7th largest ratio of current account surplus to GDP in the last 75 quarters. So much for global trade flows moving to adjust their imbalances. Remember these huge imbalances were a big factor behind the financial crisis we are still emerging from.

Of deficits and surpluses

While there is a good deal of optimism about the rekindling of global growth and a revival of global manufacturing, it is clear that the euro area is taking the lion's share of global domestic demand along with Asia where growth is bought and paid for with exports. Thanks to U.S. oil production and oil exports, the U.S. trade balance has been steady and the U.S. current account deficit as a percentage of GDP has been steady at around 2.5% of GDP. In nominal terms, the U.S. current account deficit has hovered about 434 billion dollars in the last two years. What is clear is that with Asia having export-led growth and the EMU running stubborn large surpluses and the U.S. deficit stabilizing in part because of oil exports commencing (and also because of oil imports being reduced), there has to be 'some place' where deficits are expanding! The one place we can identify a clear contrary movement is among OPEC members where the combination of lower oil prices and increased U.S. supply have made a dent in reducing OPEC surpluses.

TPP

Of course, in pursuit of a TPP without the U.S., what is missing from any TPP construct is a market into which to sell goods. All of the aspiring TPP members are exporters; which sort of begs the question of the point of TPP. China can try to muscle in and take the U.S. role there but it is not a net consumer nation; it is a trade surplus country and a net exporter. How does that square peg fit in the round hole that the U.S. leaves behind? How does that version of TPP make any sense?

What's wrong with Europe

In this context, what is wrong with Europe is quite clear. Its surpluses are way too large which ultimately will mean that the euro exchange rate is not strong enough. When the ECB finally does begin to exit its easy money stimulus polices, the euro will rise and at that point the competitiveness of the EMU will be put to a real test. For now forecasts of strength in the EMU and the German economy are being lifted. But that cannot last for too long without some current account consequences. Europe simply cannot keep running this size of surplus without adverse global consequences.

The data show that while the EMU has been growing 'better' its imports have slowed. Imports are stronger over the last 12 months than over the previous 12 months, but over six months imports are falling at a 2.1% pace and over three months imports are rising at only a 2.5% annual rate. Imports are actually slowing over these shower horizons compared to the full year even though growth is getting stronger. For manufacturing imports, flows have fallen over three months and six months.

Meanwhile, the EMU area's exports are at 8.8% over the past year, up from a 2.4% pace one year ago at this same time of year. And exports are accelerating to 9.9% pace over three months. Both manufacturing and nonmanufacturing exports are strong over three months as well as over 12 months. EMU area exports are bullet-proof while imports have gone lethargic. It's a fine combination for Europe but not for the rest of the world.

By country

Germany shows strong exports and imports over 12 months, but both flows are weaker over three months and six months. German imports fall over three months. France shows strong nominal exports and imports over 12 months with even stronger growth rates over three months. On the export front, the Netherlands, Finland and Portugal all show strong exports over 12 months at or near double-digit growth. The Netherlands and Finland show weakening flows over three months, but Portugal registers an export surge over three months.

The curious case of the U.K.

The U.K. is a curious case of a European economy not tied into the EMU currency arrangement and a country whose currency fell sharply about one year ago. While U.K. exports and imports over 12 months are up strongly at or near double-digit rates. Imports have accelerated despite the pound's drop and exports have withered and are falling at a 2.6% annual rate over three months. Improved competiveness from a weaker pound sterling paradoxically has destroyed U.K. trade! It is a very odd outcome. It seems too soon for Brexit effects to be impacting U.K. trade flows, but I have little explanation for it. U.K. imports act as though their sterling prices were marked up when the pound fell and yet import volumes have been maintained. U.K. exports, on the other hand, have recently gone very weak despite what appears to be improving growth in the EMU area, an important U.K. export market after the pound fell sharply and at a time when U.K. competitiveness should be sharp.

Stop making sense!

On balance, one tells very different stories about trade generally depending on whether one looks at year-on-year growth rates or shorter growth rates. Maybe much of trade is in transition. If that is true, then trade is decelerating everywhere except for France, Portugal and U.K. imports. Meanwhile, in the U.K., the Bank of England is raising rates as wages continue to be eroded by inflation. That is nothing short of peculiar. There is an awful lot in train that seems incompatible with other things that also are in train. This is why I think Europe is still in a sorting out period and Brexit is probably one of the big reasons as firms begin to act and plan for the future.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief